Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

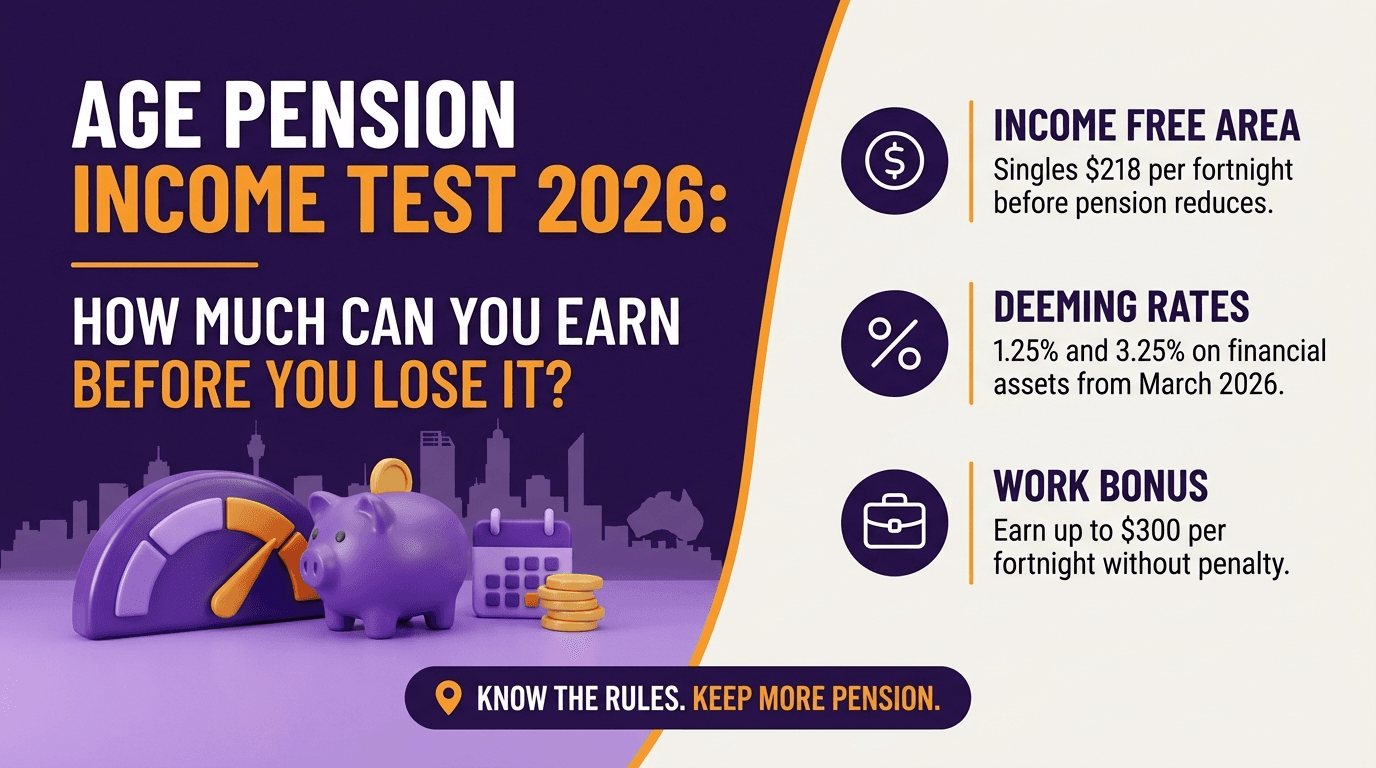

Age Pension Income Test 2026: How Much Can You Earn Before You Lose It?

What if you're receiving less Age Pension than you're entitled to, not because of your income or assets, but because no one's ever explained how the income test actually works? On average, retirees who apply late miss approximately $18,000 in Age Pension payments. The income test is one of two means tests Services Australia applies to assess Age Pension entitlement. Most retirees think it's straightforward. Deeming, the Work Bonus, and the interaction between the income and assets tests mean it's often not, and the gap between what retirees receive and what they're entitled to can be thousands of dollars per year. This guide explains the 2026 income test figures, how deeming works, the Work Bonus, and the practical strategies that help retirees structure income and assets to maximise their Age Pension entitlement.

The income test is one of two means tests Services Australia applies to assess Age Pension entitlement. The other is the assets test. Centrelink calculates your pension under both and pays whichever produces the lower result. For many retirees, the income test, and specifically the deeming rules within it, is the binding constraint on their pension payment.

TL;DR: The 2026 Figures at a Glance

Singles can earn up to $218 per fortnight before the pension starts to reduce

Couples combined can earn up to $380 per fortnight before reduction begins

Above these amounts, the pension reduces by 50 cents per dollar of excess income

The pension cuts off entirely at approximately $2,619.80 per fortnight for singles and $4,000.80 per fortnight for couples combined

Deeming rates of 1.25% and 3.25% apply to financial assets, with thresholds of $64,200 (single) and $106,200 (couple) at the lower rate

The Work Bonus allows Age Pension recipients to earn up to $300 per fortnight from employment without affecting the pension

Many retirees with $300,000 to $800,000 in super incorrectly assume they don't qualify. Partial Age Pension is common across this range and often worth $15,000 to $40,000 per year.

Bottom line: The income test is more nuanced than most retirees realise. Deeming, the Work Bonus, and asset structuring decisions can meaningfully shift pension entitlements, sometimes by thousands of dollars per year.

Jump to a Section

What the Income Test Measures

The 2026 Income Free Area and Taper Rate

Deeming: The Most Misunderstood Part of the Income Test

The Work Bonus: Earning from Employment Without Penalty

How the Income and Assets Tests Interact

Strategies to Maximise Age Pension Under the Income Test — the high-value section

Two Age Pension Calculation Examples: Single and Couple

Common Mistakes Retirees Make With the Income Test

FAQ

Ready to Work Out Your Age Pension Entitlement?

What the Income Test Measures

The income test assesses all assessable income from every source. This includes:

Employment income (wages, salaries, self-employment income)

Investment income assessed through deeming rules on financial assets

Rental income from investment properties (assessed at actual amount, not deemed)

Income streams from account-based pensions and annuities

Foreign pensions and overseas income

Business and trust income

Deemed income from financial assets including bank accounts, shares, managed funds, and superannuation in pension phase

What the income test does not include:

Income from the principal home (it is exempt from both tests)

Most government payments including the Age Pension itself

Certain exempt payments and allowances

The income test looks at assessable income on a fortnightly basis. The key thresholds are reviewed twice yearly (typically in September and March) and change with indexation.

Bottom line: The income test covers almost every income source a retiree has. Understanding what is and is not included determines the accuracy of any entitlement calculation.

The 2026 Income Free Area and Taper Rate

The income free area is the amount of income a retiree can receive before the pension begins to reduce. All figures effective from 20 March 2026.

Status | Fortnightly Income Free Area | Annual Equivalent |

Single | $218 per fortnight | ~$5,668 per year |

Couple (combined) | $380 per fortnight | ~$9,880 per year |

Above the free area, the pension reduces at the taper rate:

Singles: pension reduces by 50 cents for every dollar of income above $218 per fortnight

Couples: each partner's pension reduces by 25 cents for every dollar of combined income above $380 per fortnight

The income cut-off points from 20 March 2026 (approximately):

Status | Income Cut-Off (Fortnightly) | Annual Equivalent |

Single | ~$2,619.80 | ~$68,115 |

Couple (combined) | ~$4,000.80 | ~$104,021 |

Above these amounts, the Age Pension entitlement is nil under the income test.

What if your $450,000 account-based pension is generating $27,000 in actual earnings but Centrelink is only deeming it to earn $13,000? The excess earnings don't count. That's a situation where growth investing inside super actually improves your Age Pension entitlement, not reduces it.

Bottom line: The income free area is modest, but the cut-off is generous. Many retirees with significant account-based pension drawdowns, rental income, and investment returns are surprised to find they still qualify for a partial Age Pension.

Want to calculate your specific Age Pension entitlement with your actual income and assets? Book a free 15-min chat with WIAA's financial advisers. Call 1800 942 843 or email clientservices@whatifadvice.com.au.

Deeming: The Most Misunderstood Part of the Income Test

Deeming is the mechanism Services Australia uses to estimate the income your financial assets generate, regardless of what they actually earn. Rather than tracking actual returns on bank accounts, shares, and managed funds, Centrelink applies a standard deemed rate to the total value of your financial assets and counts that as income.

What Is Deemed?

Deeming applies to a broader range of assets than most retirees realise. These are the financial assets that attract deeming under the 2026 rules:

Bank accounts, term deposits, and cash management accounts

Shares, ETFs, and listed securities

Managed funds and unlisted investments

Account-based pensions and superannuation in the pension phase (once you reach Age Pension age)

Loans made to other parties

Equally important is what Centrelink does not deem. These exemptions create planning opportunities:

The principal home

Investment properties (rental income is assessed directly at actual amounts)

Personal use assets such as vehicles and household contents

Superannuation in the accumulation phase for a partner who has not yet reached Age Pension age

The 2026 Deeming Rates

Deeming rates changed significantly on 20 March 2026, ending a freeze that had been in place since May 2020. The rates increased by 0.5 percentage points on both tiers.

Financial Asset Value | Single | Couple (combined) | Deemed Rate |

First threshold | First $64,200 | First $106,200 | 1.25% per year |

Above threshold | Above $64,200 | Above $106,200 | 3.25% per year |

How Deeming Works in Practice

For a single retiree with $300,000 in financial assets:

First $64,200 deemed at 1.25%: $802.50 per year ($30.87 per fortnight)

Remaining $235,800 deemed at 3.25%: $7,663.50 per year ($294.75 per fortnight)

Total deemed income: $8,466 per year ($325.62 per fortnight)

This $325.62 per fortnight exceeds the $218 free area by $107.62. At 50 cents per dollar, the pension reduces by $53.81 per fortnight from the maximum rate of $1,200.90. The retiree receives approximately $1,147.09 per fortnight in Age Pension, regardless of what their $300,000 actually earns. If their assets earn 6%, the excess earnings are not counted. If their assets earn 1%, they are still deemed to earn 3.25% on the portion above the threshold.

Bottom line: Deeming is a simplification that benefits retirees with high-yielding investments and disadvantages those with low-yielding ones. The 2026 rate increase means retirees with significant financial assets may see a modest reduction in pension payments compared to prior years.

Deeming confusing? The free Retire Ready Roundtable workshop covers Age Pension assessment, deeming rules, and retirement income structuring in 90 minutes — in Brisbane, Melbourne, and online. Reserve your seat.

The Work Bonus: Earning from Employment Without Penalty

The Work Bonus is one of the most underutilised features of the Age Pension system. It allows pension recipients to earn income from employment or self-employment without it immediately affecting their pension.

The Work Bonus has several features that work together. Understanding them fully shows why part-time work is more financially attractive than most pensioners assume:

The first $300 per fortnight of employment or self-employment income is exempt from the income test

Unused Work Bonus accrues in a Work Bonus bank up to a maximum of $11,800

New Age Pension recipients receive a $4,000 opening balance in their Work Bonus bank

The Work Bonus bank can be drawn on in fortnights where employment income exceeds $300

Work Bonus applies only to employment income, not to investment income, rental income, or deemed income from superannuation

What if you've been avoiding casual work because you thought every dollar would come off your pension? With a full Work Bonus bank of $11,800 and the $300 fortnightly exemption, a pensioner could earn over $9,000 in a single fortnight before the pension is affected.

Bottom line: The Work Bonus makes paid employment significantly more financially attractive for Age Pension recipients. Retirees considering part-time or casual work should understand their Work Bonus bank balance before assuming all earnings will reduce their pension.

How the Income and Assets Tests Interact

Services Australia assesses retirees under both the income test and the assets test and pays the lower result. Understanding which test is binding for your specific situation determines where planning efforts are most valuable.

Situation | Likely Binding Test |

High financial assets, moderate actual income | Assets test more likely to bind |

Significant account-based pension drawdowns | Income test may bind via deeming |

Large investment property portfolio | Income test (rental income assessed directly) |

Home-owning couple with modest super | May qualify under both tests |

Non-homeowner with lower assets | Income test |

For the approximately two-thirds of part-rate pensioners who are income-tested rather than assets-tested, the deeming calculation on financial assets is the primary lever. Small changes in financial asset levels can produce meaningful changes in pension payments.

Bottom line: Knowing which test is binding for your situation focuses planning efforts on the most valuable lever. An adviser or Services Australia financial information officer can help identify this.

Strategies to Maximise Age Pension Under the Income Test

This is the section where planning actually makes a difference. For a couple receiving $5,000 to $10,000 less per year than they're entitled to, the strategies below are the reason why, and the fix. None of these are aggressive or unusual. They are well-established approaches that experienced financial advisers apply regularly for clients approaching or in retirement.

1. Super in Accumulation Phase for the Younger Partner

Superannuation held in the accumulation phase by a partner who has not yet reached Age Pension age is not counted under either the income or assets test for the older partner. For couples with an age gap, contributing to the younger partner's accumulation super can meaningfully reduce deemed income for the pension-age partner while the assets remain accessible for the household.

This strategy requires attention to contribution caps and the Division 296 rules for balances above $3 million (subject to current ATO rules).

2. Review Investment Allocation Relative to Deeming Rates

The upper deeming rate of 3.25% is lower than returns many retirees are earning on shares and growth assets. Where actual returns significantly exceed deeming rates, the excess is not counted. This creates a situation where higher-yielding growth investments produce better after-pension outcomes than low-yielding deposits that attract deeming at the full rate.

This is not a reason to take inappropriate investment risk. It is a reason to understand that deeming does not penalise genuine investment outperformance above the deeming rate.

3. Prepaid Funeral Expenses

Prepaid funeral plans and funeral bonds up to a specified limit are exempt from both the income and assets tests. Moving assessable financial assets into a prepaid funeral arrangement reduces the deemed income calculation.

4. Gifting Within the Gifting Rules

Retirees can gift up to $10,000 per financial year or up to $30,000 over five financial years without it being counted as a deprived asset under the gifting rules. Gifts above these amounts are counted as a deprived asset for five years.

Gifting within the rules reduces assessable assets and therefore reduces deemed income under the income test.

5. Consider an Annuity

Certain complying income stream products (annuities) receive concessional treatment under the income test. A portion of the income is treated as a return of capital rather than assessable income. For some retirees, structuring part of their retirement income through a complying annuity reduces income test exposure.

Bottom line: Age Pension maximisation is a legitimate and often high-value planning exercise. For a couple receiving $5,000 to $10,000 less per year than they could with better structuring, the value of professional advice is tangible and immediate.

Age Pension maximisation strategies work best when implemented before eligibility age. On average, retirees who apply late miss approximately $18,000 in payments. Book a free 15-min chat to start planning your Age Pension position: call 1800 942 843 or book online.

Two Age Pension Calculation Examples: Single and Couple

Example 1: Margaret, Single Homeowner, $450,000 in Financial Assets

Margaret is 70 and single. She owns her home and has $450,000 in an account-based pension. She draws the minimum 5% per year ($22,500 annually, approximately $865 per fortnight).

Her income test calculation:

Deemed income on $450,000: first $64,200 at 1.25% ($802.50) plus remaining $385,800 at 3.25% ($12,538.50) = $13,341 per year ($513.12 per fortnight)

Deeming applies regardless of her actual drawdown

Income free area: $218 per fortnight

Excess income: $513.12 minus $218 = $295.12 per fortnight

Pension reduction: $295.12 multiplied by 0.50 = $147.56 per fortnight

Age Pension received: $1,200.90 minus $147.56 = $1,053.34 per fortnight ($27,387 per year)

Margaret also has assessable assets of $450,000. Both tests are calculated and the lower result applies.

Margaret's total retirement income: $22,500 from account-based pension drawdown plus $27,387 from Age Pension = approximately $49,887 per year, before the account-based pension earnings are considered.

Example 2: Robert and Helen, Couple Homeowners, $800,000 Combined Financial Assets

Robert is 68 and Helen is 67. Both have reached Age Pension age. They own their home and have $800,000 combined in account-based pensions. They draw $48,000 per year combined ($1,846 per fortnight).

Their income test calculation:

Deemed income on $800,000: first $106,200 at 1.25% ($1,327.50) plus remaining $693,800 at 3.25% ($22,548.50) = $23,876 per year ($918.31 per fortnight combined)

Income free area for couple: $380 per fortnight combined

Excess income: $918.31 minus $380 = $538.31 per fortnight

Pension reduction: $538.31 multiplied by 0.50 = $269.16 per fortnight combined ($134.58 each)

Combined Age Pension received: $1,810.40 minus $269.16 = $1,541.24 per fortnight ($40,072 per year combined)

Their total retirement income: $48,000 from drawdowns plus $40,072 from Age Pension = approximately $88,072 per year before investment earnings are considered.

Common Mistakes Retirees Make With the Income Test

Assuming they do not qualify because they have super. Many retirees with balances between $300,000 and $800,000 incorrectly assume their super disqualifies them. The income and assets tests have generous thresholds, and partial Age Pension entitlements are common across this balance range.

Not understanding that deeming applies to account-based pensions. Account-based pensions in the pension phase are deemed financial assets once the holder reaches Age Pension age. Many retirees believe only the drawdown amount counts, not realising the full balance is subject to deeming.

Not using the Work Bonus. Retirees who work casually without understanding the Work Bonus often assume all employment income reduces their pension. The $300 per fortnight exemption and accumulated bank make part-time work significantly more financially attractive.

Gifting above the gifting rules. Large gifts to children or grandchildren above the $10,000 per year or $30,000 over five years limits are counted as deprived assets for five years, as if the retiree still held them.

Ignoring the Commonwealth Seniors Health Card. Retirees who miss the Age Pension on income grounds may still qualify for the CSHC, which provides access to concessional prescriptions and bulk-billed GP incentives. The 2026 income threshold is approximately $101,105 for singles and $161,768 for couples combined. There is no assets test.

Not reassessing after a major asset or income change. Deeming is calculated on current financial asset values. A significant market decline, property sale, or inheritance changes the calculation. Services Australia should be notified of material changes.

Not seeking advice before the claim date. On average, retirees who apply late miss out on approximately $18,000 in payments. The income test calculation is worth understanding before eligibility age, not after.

FAQ

How much can a single person earn before losing the Age Pension in 2026?

The income free area for a single pensioner is $218 per fortnight. Above this, the pension reduces by 50 cents for every dollar of excess income. The pension cuts off entirely at approximately $2,619.80 per fortnight. These figures are effective from 20 March 2026 and will be reviewed again at the next indexation.

What are the deeming rates in 2026?

From 20 March 2026, the lower deeming rate is 1.25% on the first $64,200 of financial assets for singles ($106,200 for couples combined). The upper deeming rate is 3.25% on amounts above those thresholds. Rates changed on 20 March 2026 after being frozen since May 2020.

Does superannuation count as income for the Age Pension income test?

Superannuation in the pension phase (account-based pension) is subject to deeming once the holder reaches Age Pension age. The full balance is deemed to earn income at the deeming rates, regardless of actual drawdowns. Superannuation in the accumulation phase for a partner who has not yet reached Age Pension age is not counted.

What is the Work Bonus and how does it work?

The Work Bonus allows Age Pension recipients to earn up to $300 per fortnight from employment or self-employment without it being assessed under the income test. Unused Work Bonus accumulates in a bank up to $11,800. New pensioners receive a $4,000 opening balance. The Work Bonus applies only to employment income, not investment or rental income.

Can I receive the Age Pension if I still work?

Yes. Employment income receives the Work Bonus exemption of $300 per fortnight, and the pension tapers rather than cuts off immediately as income rises. Many Australians receive a partial Age Pension while working part-time, particularly if their employment income remains below the income cut-off threshold.

What is the Commonwealth Seniors Health Card and do I qualify?

The CSHC is available to Australians who have reached Age Pension age but do not receive the Age Pension, often because their income or assets exceed the pension thresholds. The 2026 income thresholds are approximately $101,105 for singles and $161,768 for couples combined. There is no assets test. It provides access to concessional prescriptions and other concessions.

How often are the income test thresholds updated?

Income test thresholds and Age Pension rates are indexed twice yearly, typically in March and September. The figures in this article are current from 20 March 2026 and will be reviewed at the next indexation. Always verify current figures with Services Australia before making financial decisions.

What is the difference between the income test and the assets test for the Age Pension?

The income test assesses what you earn or are deemed to earn from financial assets. The assets test assesses the total value of what you own. Centrelink calculates your entitlement under both tests and pays whichever produces the lower pension amount. For many retirees with significant financial assets, the income test is the binding constraint because of the way deeming works.

Can I reduce my assessable income to get more Age Pension?

Yes, through a range of legitimate strategies including moving super into the accumulation phase for a younger partner, gifting within the gifting rules, prepaid funeral expenses, and structuring part of retirement income through a complying annuity. These strategies work best when planned before Age Pension eligibility age. A financial adviser can model the impact of each strategy on your specific entitlement.

Ready to Work Out Your Age Pension Entitlement?

The Age Pension income test calculation is more complex than most retirees realise, and the gap between what you're receiving and what you're entitled to can be thousands of dollars per year. The right advice can close that gap.

Still asking what if about your Age Pension entitlement? The calculation is specific to your income and assets. Let's run the numbers.

Three ways to start:

Free 15-minute phone chat at 1800 942 843 to run the income test calculation with your specific figures and find out if you're getting everything you're entitled to.

Free Retire Ready Roundtable workshop in Brisbane, Melbourne, or online. 90 minutes covering retirement income, Age Pension assessment, and super strategies. Reserve your seat.

Email clientservices@whatifadvice.com.au with your approximate super balance and income sources and we'll give you an initial read on your likely Age Pension entitlement.

WIAA has advised 1,000+ Australians through retirement planning, with 6 financial advisers operating from offices in Toowong, Grange, and Melbourne. AFSL 528250.

General Advice Disclaimer: This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions. Age Pension rates, income test thresholds, and deeming rates are reviewed twice yearly by Services Australia and are subject to change. All figures in this article are effective from 20 March 2026. Always verify current figures with Services Australia before making decisions. What If Advice is an Authorised Representative under Beryllium Advisers Pty Ltd, AFSL 528250.