Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

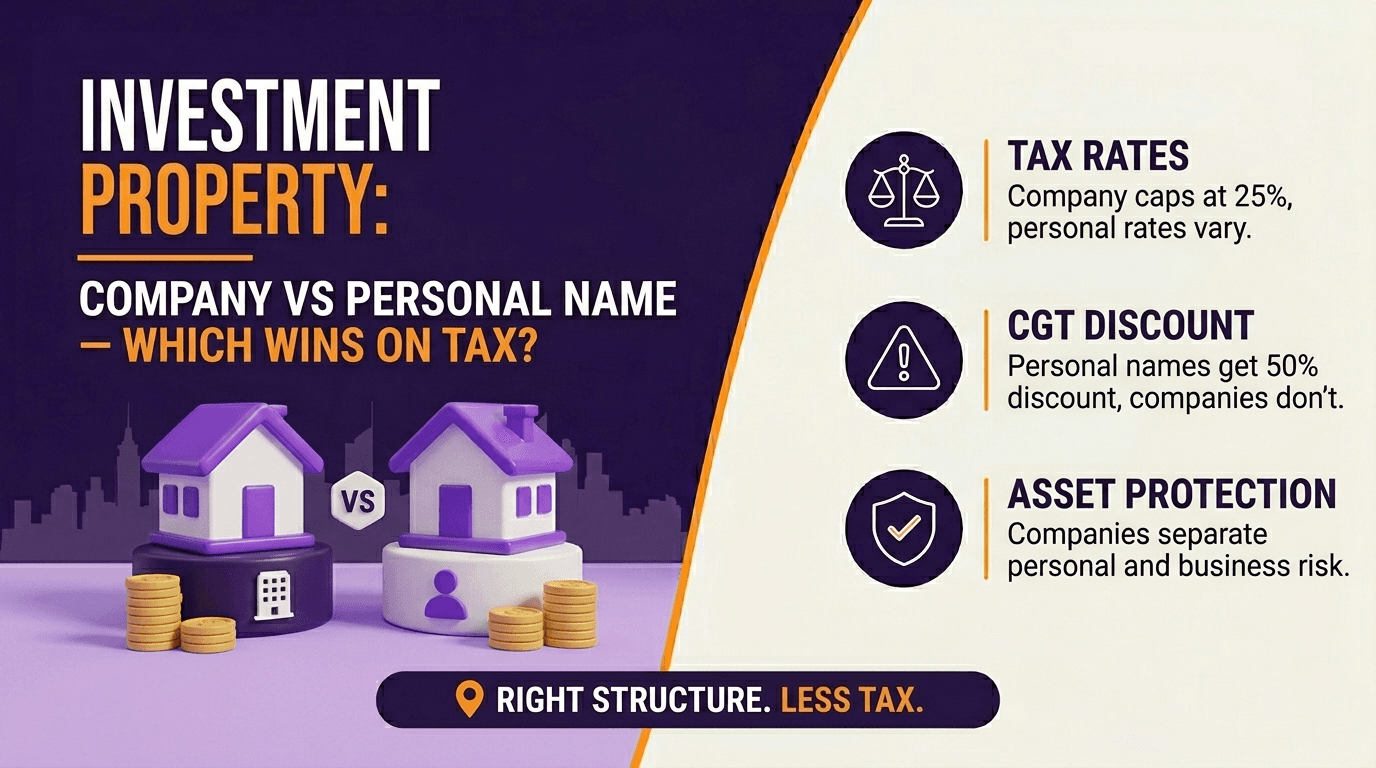

Investment Property in a Company vs Personal Name: Which Wins on Tax?

What if the structure you choose for your next investment property locks in a tax outcome that plays out over the next 20 years, and the rules that govern it just changed on 12 May 2026? The Budget night announcements on negative gearing and CGT mean the personal name vs company decision looks materially different for established residential properties purchased after that date. This post serves two reader types: investors already holding property acquired before Budget night (grandfathered, no panic needed) and investors making purchase decisions now (the 2026 rules apply to you). WIAA's registered tax agents have been reviewing client structures since Budget night; the analysis below reflects the announced rules and the grandfathering provisions as currently understood. This guide explains how each structure works, where each wins under current and proposed rules, and what the 2026 changes mean for investors making decisions now.

TL;DR: The 2026 Comparison at a Glance

Personal name has historically won on CGT (50% discount) and negative gearing (losses deductible against salary)

Companies win on income retention (flat 25% rate) and offer no CGT discount on sale

The 2026 Budget has announced that for established residential properties acquired after 7:30pm AEST 12 May 2026, negative gearing losses will only be deductible against rental income, not salary, from 1 July 2027

The 50% CGT discount is being replaced by indexation and 30% minimum tax from 1 July 2027 for both individuals and companies

Properties acquired before Budget night are fully grandfathered under the existing rules

New builds remain exempt from both changes, with investors retaining full negative gearing and choice of CGT treatment

If you purchased an established property after 7:30pm AEST 12 May 2026 and are already under contract, seek specific professional advice on your structure before the 2027 changes take effect

Bottom line: The 2026 Budget changes narrow the personal name advantage significantly for new purchases of established properties. For grandfathered properties and new builds, the existing comparison largely holds. Professional advice specific to your situation is essential before making any structural decision.

Where do you sit? Two situations, two different conversations.

You own an investment property acquired before 7:30pm AEST 12 May 2026: your property is fully grandfathered. The existing negative gearing and CGT rules apply for the life of that investment. No structural change required.

You're considering buying an established residential property now, or you purchased after Budget night: the announced 2027 negative gearing restriction applies to you. Read the negative gearing section carefully and seek specific advice before finalising your structure.

Jump to a Section

How Personal Name Ownership Works

How Company Ownership Works

The Head-to-Head Tax Comparison: Current Law vs Announced Changes

The Negative Gearing Change: What It Means If You're Buying Now

The CGT Comparison: Where the Real Difference Lives

Land Tax: The Often-Overlooked Cost

Asset Protection: The Non-Tax Consideration

Two Property Investor Examples

Common Mistakes Property Investors Make

FAQ

Ready to Work Out the Right Structure for Your Situation?

How Personal Name Ownership Works

Personal name is the default structure for most Australian property investors. Understanding exactly what that means for tax is the starting point for any comparison.

Key features of personal name ownership:

Rental income is added to your taxable income and taxed at your marginal rate

Rental expenses (interest, rates, insurance, management fees, depreciation) are deducted against all income

Net rental losses (negative gearing) are currently deductible against salary and other income for properties acquired before 12 May 2026

Capital gains on sale are taxed at marginal rates with the 50% CGT discount available for assets held over 12 months (under current law until 30 June 2027)

Land tax applies at individual thresholds, which vary by state

Asset protection is limited: the property sits in your personal name and is accessible to creditors

The primary advantage of personal name ownership has always been the interaction between negative gearing and the 50% CGT discount. At a 37% marginal rate, a $15,000 annual rental loss saves $5,550 in tax. On sale after 10 years with a $400,000 capital gain, the 50% discount reduces the taxable gain to $200,000, saving approximately $74,000 in tax compared to a company sale.

What if you've been holding your investment property in personal name assuming the 50% CGT discount would always be available on sale? Under the announced 2027 rules, that assumption needs revisiting for gains accruing after 1 July 2027.

Bottom line: Personal name ownership has historically been most advantageous for negatively geared properties held long term by higher-income earners. The 2026 Budget changes narrow this advantage for new purchases of established properties.

How Company Ownership Works

Company ownership changes the tax treatment in ways that benefit some investors significantly and disadvantage others. The profile matters.

Key features of company ownership:

Rental income is taxed at the flat 25% company tax rate (for base rate entities) or 30% for larger companies

Rental expenses are fully deductible against company income

Net rental losses within the company cannot be passed to shareholders; they are retained in the company and carried forward

Capital gains on sale are taxed at the company rate with no access to the 50% CGT discount

Profits distributed to shareholders as dividends come with franking credits at the company tax rate

Land tax is generally assessed at higher rates for companies and without individual thresholds in most states

Asset protection is stronger: shareholders have limited liability and the property is held by a separate legal entity

The company's key advantage is income retention. If the property is positively geared and the investor does not need the income immediately, retaining profits inside the company at 25% is significantly cheaper than taking them personally at 37% to 47%.

The company's key disadvantage is the loss of the 50% CGT discount on sale. This is typically the decisive factor for most long-term property investors.

Bottom line: Company ownership suits positively geared investors who plan to retain income inside the structure. It is rarely optimal for negatively geared investors relying on the salary offset, or for those planning to realise a large capital gain.

The Head-to-Head Tax Comparison: Current Law vs Announced Changes

This table is the most useful starting point in the post. Read across each row for the dimension you care most about, or read down each column for the full picture of each structure. The post-2027 columns reflect announced but not yet legislated changes. Treat them as the probable direction, not confirmed law.

Tax Dimension | Personal Name (Current Law) | Personal Name (Post-2027 Announced) | Company (Current and Post-2027) |

Rental income tax rate | Marginal rate (up to 47%) | Marginal rate (up to 47%) | 25% flat (base rate entity) |

Negative gearing (pre-12 May 2026 property) | Deductible against all income | Grandfathered, fully deductible | Loss stays in company, carries forward |

Negative gearing (post-12 May 2026 established property) | Currently deductible against all income | Only against rental income from 1 July 2027 | Loss stays in company, carries forward |

Negative gearing (new build) | Deductible against all income | Deductible against all income | Loss stays in company, carries forward |

CGT on sale (pre-1 July 2027 gains) | 50% discount, then marginal rate | Grandfathered 50% discount on pre-2027 gains | 25% flat, no discount |

CGT on sale (post-1 July 2027 gains) | Indexation, 30% minimum tax | Indexation, 30% minimum tax | 25% flat, no indexation |

Land tax treatment | Individual thresholds apply | No change | Higher rates, fewer thresholds |

Asset protection | Limited | No change | Strong (limited liability) |

Loan accessibility | Easier personal lending | No change | Harder, higher rates typical |

Bottom line: The comparison depends heavily on whether the property is positively or negatively geared, when it was or will be acquired, and what the investor's income and exit strategy looks like.

The Negative Gearing Change: What It Means If You're Buying Now

The most significant 2026 Budget change for this comparison is the limitation on negative gearing for established residential properties acquired after 7:30pm AEST 12 May 2026.

Under the announced rules from 1 July 2027:

Losses from established residential properties acquired after Budget night can only be offset against residential rental income or capital gains from residential properties

They cannot be offset against salary, business income, or other income

Unused losses can be carried forward to future years against rental income

This change affects individuals, partnerships, companies, and most trusts equally for established residential properties acquired after the cutoff. Companies holding established residential property acquired after Budget night face the same loss restriction as individuals.

The practical implication for the personal name vs company comparison is significant. One of the primary reasons to own in personal name (the ability to offset negative gearing against a salary at 37% to 47%) is removed for new purchases of established properties. This makes the personal name vs company distinction less about the salary offset and more about:

CGT treatment on eventual sale

Tax rate on positive rental income as the property becomes positively geared

Asset protection requirements

Land tax position

For properties acquired before Budget night, the grandfathering provisions fully preserve the existing rules for the life of that investment.

Bottom line: For established residential properties purchased after 12 May 2026, the negative gearing salary offset will not be available from 1 July 2027. This removes a key reason to prefer personal name over company for new purchases.

Purchased an established investment property after 12 May 2026? The negative gearing salary offset is available until 30 June 2027 under current law. After that, if the announced changes proceed, the offset is restricted to rental income only. That gives you a known planning window to review your structure, depreciation strategy, and loan setup before the rules change. Book a 15-min chat with WIAA's registered tax agents to scope your position. Phone 1800 942 843 or email tax@whatifadvice.com.au.

The CGT Comparison: Where the Real Difference Lives

The CGT comparison is where the personal name vs company decision has always been most stark. This remains true under the announced changes, though the gap narrows from 1 July 2027.

Under Current Law (Gains Accruing Before 1 July 2027)

For a property sold with a $400,000 capital gain:

Personal name (37% marginal rate): After 50% discount, taxable gain of $200,000, tax of approximately $74,000

Company: Full $400,000 taxable at 25%, tax of $100,000, plus personal tax on dividends received

Personal name wins by approximately $26,000 on CGT alone before considering the franking credit impact.

Under Announced Rules (Gains Accruing After 1 July 2027)

For a property sold with a $400,000 capital gain (all accruing post-2027, in a high-inflation scenario where indexation adjusts the cost base by $60,000):

Personal name (37% marginal rate): Net gain after indexation of $340,000, 30% minimum tax applies, tax of approximately $102,000

Company: Full gain (no indexation benefit for companies under announced rules) of $400,000 at 25%, tax of $100,000

The gap between personal name and company on CGT narrows significantly under the announced rules, particularly in lower-inflation environments where indexation provides limited benefit. In some scenarios the company rate may actually produce a comparable or better outcome.

This analysis is based on announced but not yet legislated changes. The detailed mechanics of how indexation interacts with the 30% minimum tax for individuals, and whether companies receive any indexation benefit, remain subject to consultation.

Bottom line: Under current law, personal name consistently wins on CGT for long-term held properties. Under the announced 2027 rules, the gap narrows considerably and in some scenarios company ownership produces a comparable outcome.

The CGT outcome on eventual sale is where the structure decision matters most. WIAA's registered tax agents can model your specific holding period and inflation assumptions against both personal name and company scenarios. Single-issue structure modelling typically starts at $1,500. Book a free 15-min scoping chat or email tax@whatifadvice.com.au.

Land Tax: The Often-Overlooked Cost

Land tax is assessed annually on the unimproved value of land above a threshold. The treatment differs significantly between individual and company ownership, and is often the deciding factor for investors with multiple properties.

General principles across most Australian states:

Individuals receive a tax-free threshold (typically $300,000 to $600,000 depending on state) before land tax applies

Companies and trusts generally receive no threshold or a lower threshold, and may face surcharge rates

Multiple properties in personal name aggregate for threshold purposes, but remain within individual rates

Foreign investors face surcharge rates in most states regardless of structure

For a single investment property below the individual threshold, land tax may not apply in personal name but does apply in a company. For investors with significant property portfolios, the land tax treatment can cost tens of thousands per year depending on the structure and state.

Always obtain state-specific land tax advice before choosing a structure, as rules vary significantly between jurisdictions.

What if the structure that wins on income tax and CGT loses significantly on land tax over a 15-year holding period? The annual land tax cost of company ownership is the most consistently undermodelled variable in the personal name vs company comparison.

Bottom line: Land tax treatment significantly favours individuals over companies in most Australian states for investors with modest property portfolios. Multiple property investors should model the aggregate land tax position carefully.

Asset Protection: The Non-Tax Consideration

The tax comparison is important, but it is not the only consideration. Asset protection is a genuine reason some investors prefer company ownership despite the tax trade-offs.

In personal name:

The property is directly owned and directly accessible to personal creditors

A judgment against you personally can be enforced against the property

No separation between your personal and investment assets

In a company:

The property is owned by a separate legal entity

Personal creditors cannot directly access company assets (subject to corporate law principles)

Directors can have personal liability in specific circumstances

The separation reduces but does not eliminate risk

For investors who operate businesses or professions with personal liability exposure (medical practitioners, lawyers, builders, and financial advisers among others), asset protection through a company or appropriately structured trust is often worth the tax trade-offs.

Bottom line: Asset protection is a genuine consideration for some investors. It should be weighed alongside the tax comparison, not treated as separate from it.

Two Property Investor Examples

Example 1: Michael, 42, Purchasing an Established Investment Property Post-Budget Night

Michael earns $185,000 as a senior corporate manager. He is considering purchasing an established residential investment property in Brisbane for $900,000 in June 2026. The property will be negatively geared by approximately $18,000 per year initially.

Michael's analysis breaks down into two time periods: the window under current law, and the position after the announced 2027 changes take effect.

Personal name:

Under current law and for 2025-26 and 2026-27, the $18,000 rental loss offsets his salary at 47%, saving approximately $8,460 per year

From 1 July 2027 (if the announced changes proceed), the loss can only be offset against rental income, not salary

On sale after 15 years with a $500,000 gain, CGT under the post-2027 rules applies to the indexed gain with a 30% minimum tax

Company:

Rental losses remain within the company, carried forward against future rental income

No salary offset at any point

Rental income as the property becomes positively geared taxed at 25%

On sale, CGT at 25% with no indexation benefit under announced rules

Michael's analysis: In the first 1 to 3 years before the announced negative gearing changes take effect, personal name produces tax savings through the salary offset. From 1 July 2027, the position becomes more comparable. The CGT outcome on eventual sale requires specific modelling based on the holding period and inflation environment. Michael engages a financial planner and accountant to model both scenarios before proceeding.

Example 2: Helen and Robert, Established Investors with Grandfathered Property

Helen and Robert purchased an investment property in 2020 and another in February 2026, both before Budget night. Both properties are negatively geared and have accumulated significant unrealised gains.

Helen and Robert's situation is the most common one for established investors: fully grandfathered, no structural action required, but still benefiting from active optimisation of their existing position. Their position:

Both properties are fully grandfathered under existing rules

Negative gearing losses continue to offset salary for the life of both investments

Gains accrued before 1 July 2027 retain the 50% CGT discount

Gains accruing after 1 July 2027 will be subject to the announced indexation and minimum tax rules if the legislation proceeds

No structural change is required for their existing properties. The grandfathering protection is clear and unconditional. Helen and Robert focus on maximising their depreciation claims, reviewing loan structures, and planning the timing of eventual sale to optimise the transitional CGT position.

Common Mistakes Property Investors Make

Choosing a structure at purchase without modelling the long-term tax outcome. The structure decision affects every year of ownership and the eventual sale. Modelling the full lifecycle tax position before purchase produces materially better outcomes than choosing by default.

Assuming a company always provides better asset protection. A poorly structured company (particularly one with inadequate separation between business and investment activities) provides less protection than expected.

Ignoring land tax in the structural decision. Many investors focus on income tax and CGT but overlook the annual land tax cost of company ownership, which can be significant over a long holding period.

Making irreversible structural decisions based on announced but unlegislated changes. The 2026 Budget negative gearing and CGT changes are announced, not law. Acting on announcements alone before legislation passes and detail is settled is premature.

Transferring property from personal name to a company after purchase. This transfer is a CGT event at market value. It can trigger substantial CGT and stamp duty on the existing gain. Structural decisions are most cost-effective at the point of acquisition.

Not considering borrowing capacity differences. Lenders typically offer less favourable terms for company loans than personal loans. The tax advantage of a company structure can be partially or fully offset by higher interest rates on the loan.

Treating the personal name vs company decision in isolation. The right structure depends on your full financial position, including other income, other assets, family situation, and long-term investment strategy. Siloed advice produces worse outcomes than integrated planning.

FAQ

Should I buy an investment property in a company or personal name? There is no universal answer. Personal name has historically won on CGT and negative gearing for higher-income earners. Company wins on income retention and asset protection. The 2026 Budget changes have narrowed the personal name advantage for new purchases of established properties. Always seek specific professional advice before making this decision.

I bought an investment property after 12 May 2026 — does the new negative gearing rule apply to me? Yes, if you purchased an established residential property after 7:30pm AEST 12 May 2026. The announced negative gearing changes from 1 July 2027 will restrict the salary offset for those properties. The restriction is the same whether you own in personal name or through a company. New builds and properties acquired before the cutoff are not affected.

Is my existing investment property protected from the 2026 Budget changes? Yes, if you acquired it before 7:30pm AEST 12 May 2026. Those properties are fully grandfathered under the existing rules for negative gearing and CGT (for gains accruing before 1 July 2027). Gains accruing after 1 July 2027 on grandfathered properties will still be subject to the announced CGT changes if those measures are legislated.

Do companies get the CGT discount on investment property in Australia? No. Companies do not access the 50% CGT discount. Capital gains are taxed at the flat company rate of 25% to 30%. This is typically the decisive reason most investors prefer personal name for long-term capital growth investments under current law.

Can a company negatively gear a property? Yes, but the loss stays within the company. It cannot be distributed to shareholders to offset their personal income. The loss carries forward inside the company and can offset future rental income or other company income. This is why company ownership is generally unsuitable for negatively geared properties where the salary offset is the primary tax benefit.

How do the 2026 Budget changes affect the company vs personal name decision? The announced negative gearing changes from 1 July 2027 restrict salary offsets for established properties acquired after 12 May 2026, applying equally to individuals and companies. The CGT changes from 1 July 2027 replace the 50% discount with indexation and a 30% minimum tax for individuals, narrowing the gap with the 25% company rate. Both changes are announced but not yet legislated.

Do companies pay more land tax than individuals on investment property? Generally yes. Most Australian states provide a tax-free threshold for individuals that does not apply to companies. This makes company ownership more expensive on an annual basis from a land tax perspective. Always obtain state-specific land tax advice.

Can I move my investment property from personal name into a company? Yes, but it is typically costly. The transfer triggers a CGT event at market value, potentially generating a large tax bill. Stamp duty also applies in most states on the transfer. Structural decisions are best made at the point of acquisition rather than retrospectively.

What about using a trust instead of a company or personal name? A discretionary trust is a common alternative that has historically offered income splitting and access to the 50% CGT discount, combining some advantages of both personal name and company. The 2026 Budget changes (30% minimum trust tax from 1 July 2028 and CGT discount replacement) also affect trusts. The trust comparison requires its own separate analysis.

Ready to Work Out the Right Structure for Your Situation?

Investment property structure decisions affect every year of ownership and the sale. With the 2026 Budget announcements reshaping the comparison for new purchases, the time to review is now, not when the legislation passes.

Still asking what if about your investment property structure? The 2026 Budget has made that question more urgent than at any point in the past decade.

Three ways to start, based on your situation:

You have existing grandfathered properties and want to optimise their position: email tax@whatifadvice.com.au to scope a depreciation and loan structure review.

You're considering purchasing now and want to understand which structure suits your situation: book a free 15-min chat at 1800 942 843 or online.

You purchased after Budget night and need to understand your options before 2027: call 1800 942 843 today. This has a known planning window and it is worth using.

WIAA combines registered tax agents and AFSL-licensed financial advisers under one roof. Offices in Brisbane and Melbourne, virtual advice Australia-wide. AFSL 528250.

General Advice Disclaimer: This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions. The 2026-27 Budget measures discussed in this article, including the negative gearing changes and CGT discount replacement, are announced but not yet legislated. Rules change and you should verify current measures and seek specific professional advice before making any structural decisions about investment property ownership. What If Advice is an Authorised Representative under Beryllium Advisers Pty Ltd, AFSL 528250.