Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

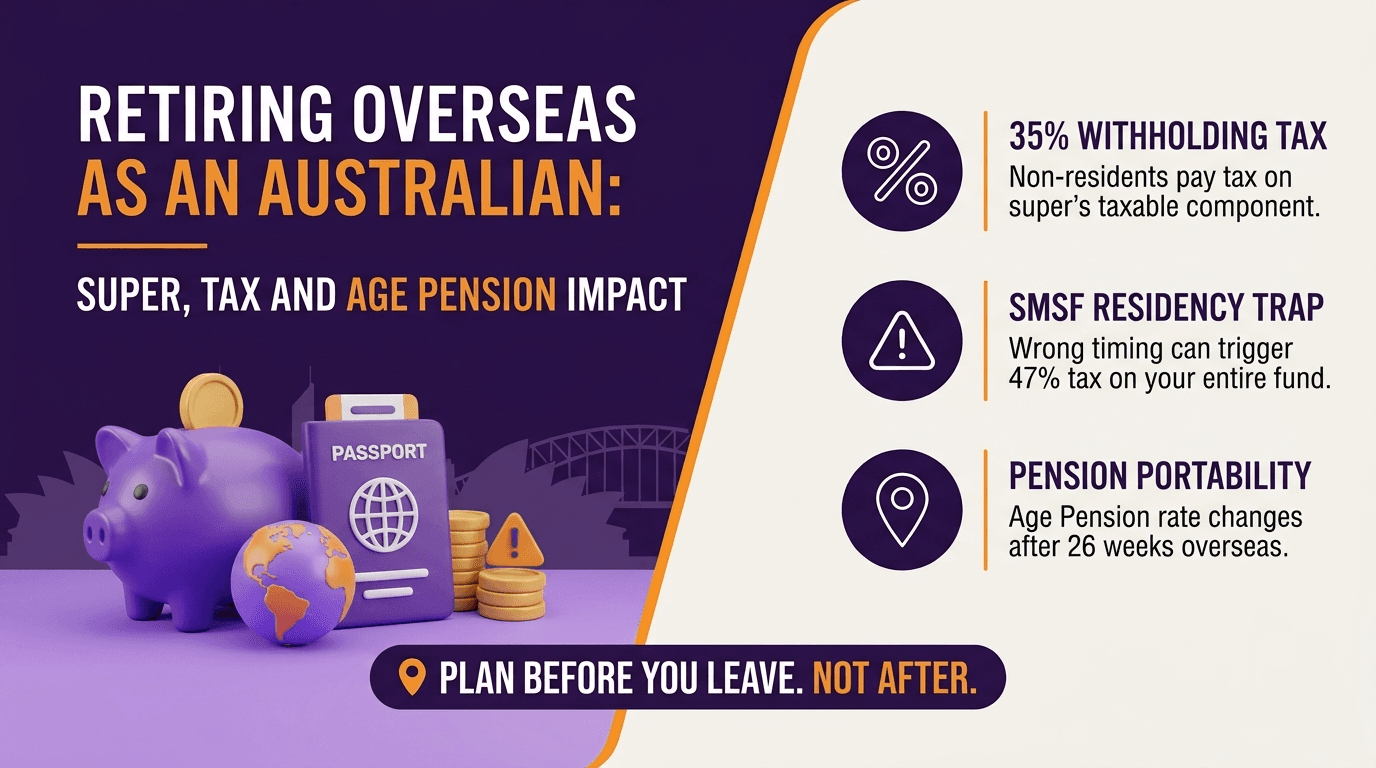

Retiring Overseas as an Australian: Super, Tax and Age Pension Impact

Retiring overseas is a serious financial decision that sits behind a web of tax rules most Australians have never needed to think about before. Your superannuation, your tax residency, your Age Pension, and your SMSF, if you have one, are all affected the moment you stop being a permanent Australian resident.

Some of these changes work in your favour. Others create tax consequences that significantly exceed what most people planning an overseas retirement expect. The SMSF residency trap alone has cost Australian retirees tens of thousands of dollars because the timing was wrong.

As financial advisers (AFSL 528250) and registered tax agents, this is genuinely hybrid territory, super and Age Pension planning on one side, tax residency and CGT on the other, and both disciplines matter here. This guide covers what actually happens to each part of your financial position when you retire overseas, what changes immediately, what changes after you have been away for a period of time, and what you need to address before you leave.

TL;DR: The Key Points

Here is the short version before the detail:

Leaving Australia permanently changes your tax residency, which affects how your income, capital gains, and super withdrawals are taxed

Non-residents do not get the $18,200 tax-free threshold and are taxed from the first dollar of Australian-sourced income at non-resident rates

Super withdrawals as a non-resident attract a withholding tax of up to 35% on the taxable component, compared with the zero or 15% that applies to many resident withdrawals

The Age Pension can be paid overseas in many cases but the rate changes after 26 weeks based on your Australian working life residence

SMSF trustees living overseas can cause the fund to fail its residency test and face tax at 47% on the entire fund value if not managed correctly before departure

Capital gains on Australian assets still apply to non-residents on taxable Australian property, and the 50% CGT discount may not be available on gains accrued after becoming non-resident

International social security agreements between Australia and some countries can affect your pension entitlement and eligibility

Planning before you leave, not after arrival overseas, is critical to avoiding avoidable tax and compliance consequences

Jump to a Section

How Leaving Australia Affects Your Tax Residency

What Tax Non-Residents Pay on Australian Income

Super Access Overseas: What Changes

Withholding Tax on Super Withdrawals as a Non-Resident

The SMSF Residency Trap

Age Pension Portability: What You Actually Get Overseas

How the 26-Week Rule Changes Your Pension Rate

International Social Security Agreements

Capital Gains Tax for Non-Residents

Key Steps to Take Before You Leave

FAQ

How Leaving Australia Affects Your Tax Residency

Australian tax law distinguishes between Australian tax residents and non-residents. These are not the same as immigration status, citizenship, or permanent residency. You can be an Australian citizen living in Europe and be a tax non-resident. You can hold a foreign passport but still be taxed as an Australian resident.

Tax residency is determined by the ATO based on a combination of tests, including whether you have an intention to reside permanently outside Australia, where your domicile is, and whether you satisfy the resides test based on your ongoing presence and connections.

For most Australians retiring overseas permanently, the key change occurs when they leave with the genuine intention of living abroad indefinitely. At that point, they generally cease to be Australian tax residents. The ATO assesses the circumstances of departure and can challenge a claimed change of residency where the facts do not support it.

The practical implications of becoming a non-resident:

You are taxed only on Australian-sourced income, not worldwide income

Income from Australian investments, super, rental properties, and business activity in Australia remains taxable in Australia

Your home country will generally tax your worldwide income, including income from Australia, subject to any double tax agreement between the two countries

The Medicare levy no longer applies to non-residents

You are generally no longer eligible to bulk-bill or claim Medicare benefits while overseas

Timing of residency change matters enormously. The ATO assesses the year in which you became a non-resident and can apportion income accordingly. Capital gains on assets sold in the year you changed residency can be split between the resident and non-resident periods, with different rules applying to each. Getting the date of residency change right, and ensuring it is documented and supportable, is the first step in any overseas retirement plan.

Bottom line: changing your tax residency by moving overseas is not automatic or administrative. It is a legal determination with significant tax consequences across super, investment income, and capital gains that needs to be understood and planned for before you leave.

What Tax Non-Residents Pay on Australian Income

Australian non-residents are taxed on Australian-sourced income at non-resident tax rates. These rates are substantially different from resident rates in one critical way: there is no tax-free threshold.

Non-resident tax rates for the 2026-27 income year:

Taxable Income | Tax Rate |

$0 to $135,000 | 30% |

$135,001 to $190,000 | 37% |

$190,001 and above | 45% |

A resident retiree with $50,000 of Australian taxable income pays approximately $6,450 in income tax (including the Medicare levy) after the low-income tax offset and tax-free threshold. A non-resident with the same $50,000 of Australian income pays $15,000, taxed flat at 30% from the first dollar with no offsets or Medicare levy applying. The gap is not marginal, it is a structural difference of roughly $8,500 that changes the economics of drawing Australian income in retirement.

Types of Australian income that remain taxable to non-residents:

Rental income from Australian property (net of allowable deductions)

Australian dividends (withholding tax rules apply to unfranked dividends)

Interest income from Australian bank accounts and bonds

Business income from Australian sources

Capital gains on taxable Australian property

Franking credits: non-residents can generally still receive franked dividends from Australian companies, but the treatment of franking credits depends on the relevant double tax agreement and Australian tax rules. Unfranked dividends paid to non-residents attract a dividend withholding tax of generally 30%, or a reduced rate under a double tax agreement (commonly 15%).

What if the income stream you planned to draw from in retirement becomes significantly less efficient the moment you change your tax residency? Understanding the non-resident rate differential before you decide where to draw income from is essential planning, not optional.

Super Access Overseas: What Changes

Access to superannuation does not change simply because you move overseas. The conditions of release still apply. You can access your super when you:

Reach your preservation age (60 for those born from 1 July 1964 onward) and retire from the workforce

Reach age 65, regardless of employment status

Meet another condition of release such as permanent incapacity or terminal medical condition

If you leave Australia before satisfying a condition of release, your super remains preserved inside the fund until a condition is met. You cannot access it simply because you are leaving Australia permanently. This is a common misconception.

Important distinction for temporary residents: former temporary visa holders who have left Australia permanently may be eligible for a Departing Australia Superannuation Payment. This provision is not available to Australian citizens or permanent residents. Australian citizens and former permanent residents must satisfy a standard condition of release to access their super, regardless of where they live.

Once you have satisfied a condition of release, you can generally access your super from overseas. Lump sums and income streams can be paid to overseas bank accounts, subject to the fund's operational rules and any relevant fees for international transfers. The key question is not whether you can access it, but how it is taxed when you do.

Bottom line: your super remains subject to its standard conditions of release when you move overseas. The change is not in access but in the tax treatment of withdrawals once you are a non-resident.

Withholding Tax on Super Withdrawals as a Non-Resident

This is the area that surprises most Australians planning an overseas retirement. The tax treatment of super withdrawals for non-residents is substantially worse than the treatment that applies to Australian residents.

Australian super withdrawals consist of two components:

Tax-free component: contributions made from after-tax money (non-concessional contributions) and certain other amounts. This component is tax-free for both residents and non-residents.

Taxable component: contributions made from pre-tax money (concessional contributions), earnings inside the fund, and employer contributions. The treatment of this component changes significantly for non-residents.

For Australian residents aged 60 and over, lump sum withdrawals from a taxed super fund are generally entirely tax-free, subject to total super balance rules and current ATO conditions. This is one of the most valuable tax benefits in the Australian system and a major reason super is such an effective retirement vehicle.

For non-residents, the taxable component of super withdrawals is subject to withholding tax at 35% for amounts paid from a taxed fund. The tax-free component remains tax-free.

Withdrawal Type | Australian Resident (60+) | Non-Resident |

Tax-free component | Tax-free | Tax-free |

Taxable component (taxed fund) | Generally tax-free | 35% withholding tax |

Taxable component (untaxed fund) | Up to 15% tax | 45% withholding tax |

A practical example:

An Australian retiree has $600,000 in super, comprising $150,000 tax-free component and $450,000 taxable component. They withdraw the entire balance as a lump sum.

As an Australian resident: the lump sum is generally entirely tax-free. Total tax: $0.

As a non-resident: the $150,000 tax-free component is tax-free. The $450,000 taxable component is subject to 35% withholding. Tax withheld: $157,500.

The difference in tax treatment on the same withdrawal from the same fund is $157,500. This number illustrates why the timing of super withdrawals relative to the change in tax residency matters so significantly.

Practical implication: where circumstances allow, withdrawing super or converting to an income stream before changing tax residency can significantly reduce the tax payable on those funds. This is one of the most important planning decisions in an overseas retirement strategy and should be modelled with specific professional advice before any departure date is set.

Not sure how your super component split affects the tax cost of retiring overseas? The financial advisers and registered tax agents at What If Advice can model the resident versus non-resident withdrawal difference for your specific fund balance. Call 1800 942 843 or email tax@whatifadvice.com.au.

The SMSF Residency Trap

For Australians with a Self-Managed Super Fund, retiring overseas introduces a compliance risk that can be catastrophic if not addressed before departure: the SMSF residency test.

For an SMSF to be a complying Australian superannuation fund, it must satisfy three conditions at all times:

The fund was established in Australia or holds Australian assets

The central management and control of the fund is ordinarily in Australia

The fund either has no active members, or all active members who are Australian residents hold at least 50% of the fund's total assets or total amounts that would be payable if the fund were wound up

The central management and control test is the primary issue for trustees moving overseas. Central management and control refers to the high-level decision-making of the fund: setting investment strategy, deciding on member benefits, and exercising trustee discretion. Where the trustees are living overseas, the ATO will scrutinise whether the fund's central management and control has moved offshore.

The ATO allows a temporary absence of up to two years before the central management and control is treated as having moved overseas, provided the absence is genuinely temporary. A permanent overseas relocation does not qualify for this concession.

If an SMSF fails the residency test, the consequences are severe:

The fund's entire assets (not just future income, but the total current balance) are assessed at the top marginal rate of 47% in the year the fund becomes non-complying

All future income of the non-complying fund is also taxed at 47%

The loss of concessional tax treatment on even a $400,000 fund can produce a tax bill of over $150,000

Options for SMSF trustees planning to retire overseas:

Roll the SMSF into an APRA-regulated fund (such as a retail or industry super fund) before departure. This is the simplest and most commonly recommended solution where the trustee is moving overseas permanently.

Appoint additional trustees who will remain in Australia and genuinely exercise central management and control. This requires real, active trustee participation by the Australian-based trustees, not a nominal appointment.

Convert from individual to corporate trustee and ensure the board of directors includes Australian-resident directors who hold genuine control over fund decisions.

All of these options must be implemented before the trustee's permanent departure from Australia. Attempting to address the residency issue after the fund has already failed the test does not retroactively restore its complying status.

What if your SMSF has been a complying fund for twenty years and becomes non-complying because the departure timing was wrong by a matter of weeks? The SMSF residency trap is one of the most preventable and most expensive mistakes in Australian retirement planning.

Age Pension Portability: What You Actually Get Overseas

The Age Pension is portable. That is the good news. Eligible Australians living overseas can continue to receive Age Pension payments from Services Australia. The more nuanced reality is that the amount you receive, and the rules that govern it, change significantly once you have been outside Australia for more than 26 weeks.

Eligibility conditions before leaving:

Have already been granted the Age Pension while living in Australia

Meet the Age Pension's standard eligibility conditions including age (currently 67), residency, and income and assets tests

Notify Services Australia of your intention to leave Australia

You cannot apply for the Age Pension for the first time from overseas in most circumstances. Applying before you leave and establishing your entitlement as an Australian resident is the correct sequence.

The first 26 weeks overseas: for the first 26 weeks outside Australia, most eligible recipients continue to receive the Age Pension at the same rate that applied in Australia, subject to the ongoing income and assets tests.

How the 26-Week Rule Changes Your Pension Rate

After 26 continuous weeks outside Australia, the way your pension rate is calculated changes. The rate is no longer based simply on your income and assets. It is also subject to a proportional calculation based on your Australian Working Life Residence (AWLR).

AWLR is the number of years you were an Australian resident between the ages of 16 and Age Pension age (currently 67). The maximum AWLR is the number of years in that window, capped at 35 for the purposes of the portability calculation.

The proportional rate formula:

Pension rate = (AWLR in whole years / 35) x maximum pension rate

Where your AWLR is 35 years or more, you receive the full pension rate (still subject to income and assets tests).

Where your AWLR is less than 35 years, your pension is reduced proportionally. An Australian who spent significant years overseas during their working life and has an AWLR of, say, 20 years, would receive 20/35 (approximately 57%) of the maximum pension rate.

Other changes after 26 weeks:

The pension supplement reduces to the basic pension supplement rate. The full pension supplement, which includes amounts for utilities, pharmaceutical costs and other living expenses, is not paid overseas beyond the 26-week mark.

The energy supplement may also be affected depending on the destination country and your circumstances.

Deeming continues to apply to your financial assets for the income test, using Australian deeming rates regardless of where the assets are held or what returns they generate overseas.

You remain subject to the income and assets tests while overseas. You are required to notify Services Australia of changes to your income, assets, and circumstances. Failing to notify can result in overpayments that Services Australia will recover.

International Social Security Agreements

Australia has international social security agreements with a number of countries. These agreements can affect both the portability of your Australian Age Pension and your eligibility for the equivalent pension in your destination country.

Countries with which Australia has active social security agreements include Austria, Belgium, Canada, Chile, Croatia, Cyprus, Czech Republic, Denmark, Finland, Germany, Greece, Hungary, India, Ireland, Italy, Japan, South Korea, Latvia, Malta, the Netherlands, New Zealand, Norway, Poland, Portugal, Slovakia, Slovenia, Spain, Switzerland, and the United States, among others.

How these agreements work:

They can allow periods of residency in one country to count toward pension eligibility in another

They can reduce or eliminate the AWLR proportionality calculation, meaning you may receive a higher pension rate in your destination country than the strict Australian formula would produce

They can provide access to the destination country's pension system in ways that supplement the Australian Age Pension

The specific terms of each agreement differ. The agreement with New Zealand operates quite differently from the agreements with European countries. If you are planning to retire to a country with which Australia has a social security agreement, understanding the specific terms of that agreement is an important part of the financial planning.

For countries without a social security agreement with Australia, the standard portability rules apply and there is no mechanism for combining residency periods between the two countries. You rely entirely on the Australian Age Pension, subject to the AWLR proportionality calculation.

Bottom line: international social security agreements can work significantly in your favour if you are retiring to an agreement country. Understanding whether your destination country has an agreement with Australia, and what the specific terms provide, can change the retirement income picture materially.

Planning to retire to a specific overseas destination and want to understand the Age Pension and tax implications? The financial advisers and registered tax agents at What If Advice can work through the pension portability and tax residency picture for your specific destination. Call 1800 942 843 or email tax@whatifadvice.com.au.

Capital Gains Tax for Non-Residents

Changing tax residency does not eliminate your exposure to Australian CGT. Non-residents remain subject to Australian CGT on taxable Australian property, which includes:

Australian real property (residential and commercial)

Interests in entities whose value is principally derived from Australian real property

Assets used in carrying on a business through a permanent establishment in Australia

Non-residents are not subject to Australian CGT on assets that do not fall into these categories, such as shares in widely held Australian listed companies where the non-resident holds less than 10% of the shares.

The 50% CGT discount and non-residents. Australian residents who hold assets for more than 12 months are entitled to a 50% CGT discount on capital gains. For non-residents, this discount is not available on gains that accrue after the date of becoming a non-resident. Gains that accrued while you were an Australian resident may still attract the discount for the resident portion, subject to the rules that apply to the apportionment of gains between resident and non-resident periods.

The deemed disposal rule. When an Australian resident becomes a non-resident, certain assets that are not taxable Australian property are treated as having been disposed of at market value on the date of departure. This deemed disposal can trigger a CGT event on unrealised gains in assets that will no longer be subject to Australian CGT once you are a non-resident. Managing this deemed disposal, including decisions about which assets to sell before departure, is an important pre-departure planning exercise.

Australian real property owned overseas. Conversely, your Australian property remains subject to Australian CGT even as a non-resident, and the main residence exemption has specific rules for non-residents. From 2020 onwards, the main residence exemption is generally not available to non-residents at the time of sale of the Australian property, subject to limited life events exceptions. This means an Australian who retires overseas and later sells their former Australian home may not be able to claim the full main residence exemption on the gain, even if they lived in the property for many years before departure.

Key Steps to Take Before You Leave

The consequences of an unplanned overseas retirement departure are far more expensive than the cost of addressing these issues in advance. The following steps are the minimum planning exercise for any Australian considering retiring overseas.

Determine your planned date of residency change and document it. The date you cease to be an Australian tax resident is the reference point for super withdrawal tax treatment, CGT deemed disposal, and Age Pension portability calculations. It should be a deliberate decision, not an incidental one.

Model the super withdrawal tax position before and after residency change. Understand the composition of your super balance (tax-free and taxable components) and the withholding tax that will apply to taxable component withdrawals as a non-resident. Where the difference is material, consider whether withdrawing a lump sum or converting to an income stream before departure reduces the overall tax cost. This calculation should be done with specific advice from a financial adviser.

Address your SMSF before you leave if you have one. Do not rely on the two-year temporary absence concession if you are leaving permanently. Rolling your SMSF into an APRA-regulated fund before departure, or restructuring the trustee arrangements to maintain genuine Australian control, must happen before the departure date.

Apply for the Age Pension before you leave if you are eligible. You cannot apply from overseas in most circumstances. If you are at Age Pension age and meet the eligibility conditions, establishing your entitlement before departure and notifying Services Australia of your overseas move is the correct sequence.

Review your investment asset ownership before departure. Assets that will trigger a deemed CGT disposal on the date of departure, and assets that will become subject to different tax treatment as a non-resident, should be reviewed with a registered tax agent. The decision about which assets to hold and which to sell before becoming a non-resident can affect the total tax position materially.

Research the social security agreement between Australia and your destination country. If an agreement exists, understand how it affects your Age Pension portability rate and whether it provides access to any pension entitlement in the destination country.

Understand the tax treatment of your Australian income in your destination country. Double tax agreements between Australia and many countries reduce or eliminate double taxation of Australian income. Understanding how your rental income, dividends, and pension will be treated in the destination country is part of the total financial picture.

Notify Services Australia and the ATO. Services Australia requires notification of your departure before you leave if you are receiving Age Pension or other payments. The ATO should be notified of your change of residency through your tax return and, where relevant, through other formal notifications.

What if you have spent decades building a super balance that the Australian tax system will treat very generously for a resident retiree, but the timing of your overseas move costs you six figures in avoidable withholding tax? That is not an unlikely scenario. It is the situation that catches Australians who plan the move but not the financial consequences of it.

FAQ

Can I access my super if I move overseas permanently?

Yes, but only once you satisfy a standard condition of release. Preservation age plus retirement, or reaching age 65, are the most common conditions. Moving overseas permanently does not itself trigger access to your super. Australian citizens and permanent residents cannot access their super simply by leaving Australia. The change when you become a non-resident is not in whether you can access your super, but in how withdrawals are taxed.

How much tax will I pay on super withdrawals if I am living overseas?

The taxable component of super withdrawals paid to a non-resident from a taxed fund is subject to a 35% withholding tax. The tax-free component (from non-concessional contributions and other tax-free amounts) remains tax-free. For a resident aged 60 and over, lump sum withdrawals are generally entirely tax-free. The withholding tax difference between resident and non-resident withdrawals can be very significant depending on your fund's component mix.

Can I take my Age Pension overseas?

In most cases, yes. The Age Pension is portable and can be paid to Australians living overseas. However, after 26 weeks outside Australia, the rate is recalculated based on your Australian Working Life Residence. Where your AWLR is less than 35 years, the pension rate is reduced proportionally. The pension supplement also reduces after 26 weeks to the basic rate.

What happens to my SMSF if I retire overseas?

This is the most critical pre-departure issue for SMSF trustees. If you move overseas permanently and remain an SMSF trustee, the fund may fail the central management and control test and become a non-complying fund. A non-complying fund is taxed at 47% on its entire asset value in the year it becomes non-complying. The recommended approach for those retiring overseas permanently is to roll the SMSF into an APRA-regulated fund before departure, or to restructure the trustee arrangements to maintain genuine Australian control.

Do I still pay CGT if I sell my Australian property after moving overseas?

Yes. Australian real property remains subject to Australian CGT for non-residents. Additionally, the main residence exemption is generally not available to non-residents at the time of sale under rules that have applied since 2020, subject to limited exceptions for certain life events. This means selling a former Australian home after moving overseas can produce a CGT liability on the full gain, without the main residence exemption that would have applied to a resident.

Do I pay income tax in both Australia and my new country?

Potentially, but double tax agreements between Australia and many countries reduce or eliminate double taxation. Australia has double tax agreements with most major retirement destinations including New Zealand, the United Kingdom, the United States, Canada, Germany, France, and many others. These agreements typically determine which country has primary taxing rights over different income types and provide credits or exemptions to prevent the same income being fully taxed twice.

Should I withdraw my super before I move overseas?

This depends entirely on your age, your super balance composition, the gap between resident and non-resident withholding tax on your taxable component, and your planned timing. For some Australians, withdrawing a lump sum or converting to an income stream before changing residency produces a significantly better tax outcome. For others, the amounts involved or the timing make this impractical. This calculation should be modelled with specific financial and tax advice before any decision is made.

What is the Australian Working Life Residence calculation?

AWLR is the number of years you were an Australian resident between ages 16 and 67 (current Age Pension age), measured in whole years, with a maximum of 35 years for the portability calculation. Where your AWLR is 35 or more, you receive the full Age Pension rate (subject to income and assets tests) after 26 weeks overseas. Where it is less, your pension is proportionally reduced. Australians who spent significant time living outside Australia during their working years may have a lower AWLR than they expect.

How do I notify the ATO and Services Australia when I move overseas?

Services Australia requires notification of your departure if you are receiving Age Pension or other payments. This should be done before you leave or as close to departure as possible. The ATO is notified of your change of tax residency through your income tax return for the year of departure, where you indicate the date your residency changed. A registered tax agent can ensure the return is completed correctly for the year that spans both resident and non-resident periods, which requires apportionment of income and any CGT events.

Will I still have access to Medicare while living overseas?

Generally, no. Medicare eligibility is tied to being an Australian resident, and once you become a non-resident for immigration and health system purposes, you are no longer able to bulk-bill or claim Medicare benefits, either in Australia during visits or for treatment overseas, since Medicare does not cover care received outside Australia in any circumstance. Some countries have reciprocal health care agreements with Australia that provide limited access to public healthcare for visiting Australians, but these are separate from Medicare and vary significantly by country. Private international health insurance is worth investigating well before departure, particularly for retirees managing ongoing health conditions.

If I move overseas partway through the financial year, do I file one tax return or two?

One return, not two. The Australian tax return for the year you leave covers the full financial year but is apportioned into a resident period and a non-resident period based on your actual date of residency change. Income and deductions are allocated to whichever period they relate to, and different rules apply to each period, particularly for the tax-free threshold, Medicare levy, and CGT discount eligibility. This apportionment is one of the more technical aspects of a departure-year return and is worth having a registered tax agent prepare rather than attempting it through standard tax software, which is generally built around a full resident or full non-resident year rather than a split one.

Planning to retire overseas and not sure where your super, tax, and pension position actually stands?

The gap between what most Australians assume will happen to their finances when they retire overseas and what actually happens under the rules can be significant. The super withholding tax position alone is worth understanding before you set a departure date.

The financial advisers and registered tax agents at What If Advice work with Australians across Brisbane, Melbourne, and virtually across Australia to model the full financial picture of an overseas retirement, including super withdrawal timing, SMSF residency issues, Age Pension portability, and the tax residency transition.

Call 1800 942 843 or email tax@whatifadvice.com.au to book a consultation before your plans are finalised.

Still asking what if about retiring overseas? That is exactly the right time to be asking it. The answers depend on your specific super balance, your fund's component split, your AWLR, and your destination. Let the team at What If Advice work through it with you. AFSL 528250.

General Advice Disclaimer: This information is general in nature and does not take into account your personal financial situation, needs, or objectives. Tax residency, super withdrawal tax treatment, Age Pension portability, and SMSF residency rules are complex and subject to change. The information in this article reflects rules as understood at the time of publication and may not reflect subsequent legislative or regulatory changes. You should seek advice from a licensed financial adviser and registered tax agent before making any decisions about retiring overseas. What If Advice is an Authorised Representative under Beryllium Advisers Pty Ltd, AFSL 528250. What If Advice Accounting Pty Ltd is a registered tax agent.