Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

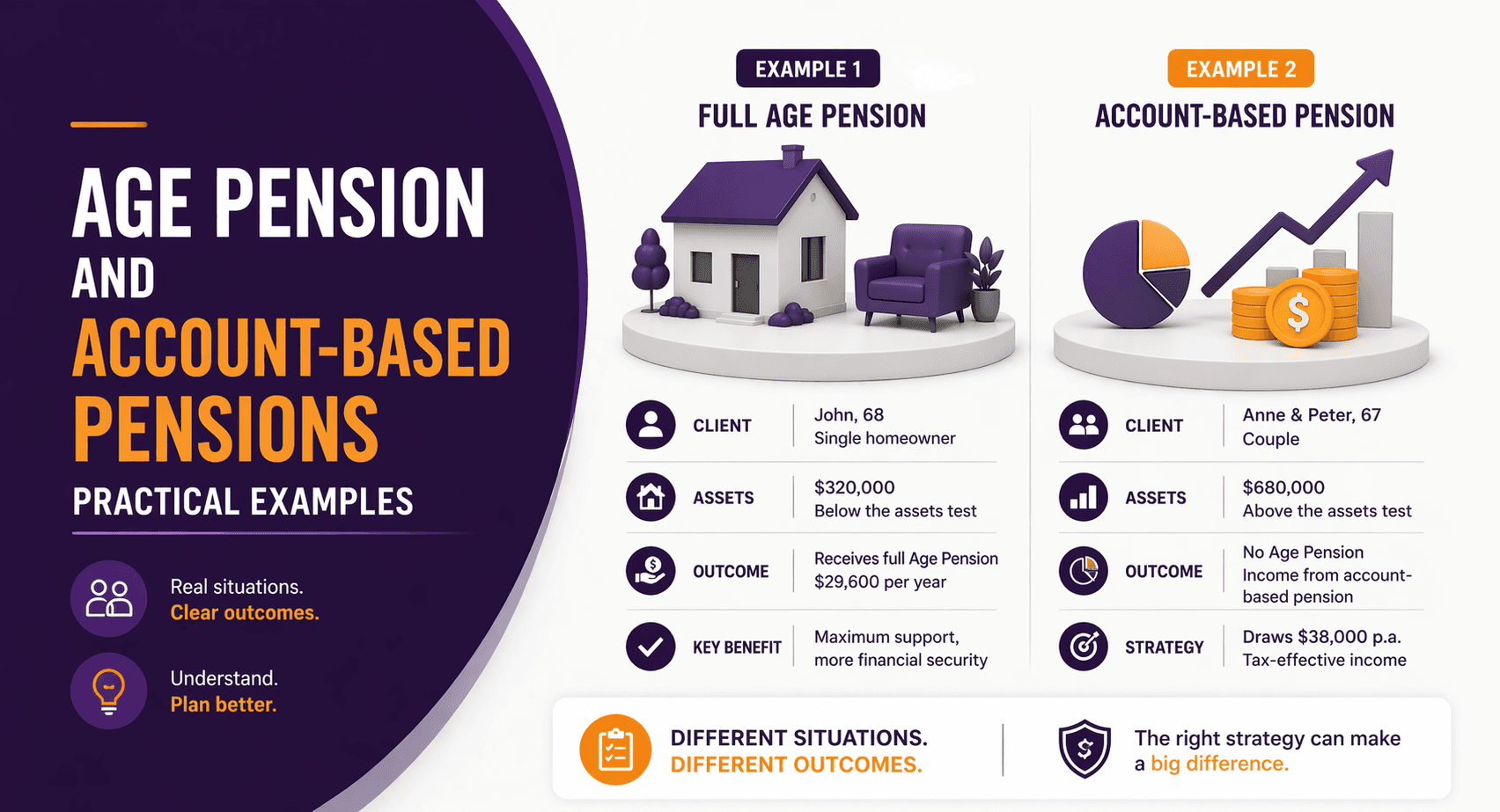

Age Pension and Account-Based Pensions: Practical Examples for Australians

If you’re drawing income from an account-based pension, it will affect your Age Pension, but not always in the way you expect.

Some retirees assume:

“More income = less pension”

That’s not always true.

Centrelink uses deeming rules, not your actual withdrawals, which means your pension outcome depends on how your super is structured and assessed.

Let’s break it down with real-world examples.

What Is an Account-Based Pension?

An account-based pension is a retirement income stream created from your super.

Once you retire (or reach preservation age), you can:

Convert your super into a pension account

Withdraw regular income

You must withdraw a minimum amount each year, based on your age (ATO rules).

How Centrelink Treats Account-Based Pensions

After you reach Age Pension age:

1. It Counts as an Asset

Your pension balance is included in the assets test.

2. It Is Deemed for Income

Centrelink does not use your actual withdrawals.

Instead, it applies deeming rates to estimate income.

This is critical.

Even if you withdraw $40,000

Centrelink might only assess $8,000–$12,000 as income

Subject to current Services Australia rules.

Why This Matters

Because:

You can withdraw more income

Without proportionally reducing your Age Pension

This creates planning opportunities most people completely miss.

Practical Examples

Example 1: Moderate Super Balance (Part Pension)

Scenario:

Single homeowner

$400,000 in account-based pension

Withdraws $30,000/year

Centrelink treatment:

Assets: $400,000 = reduces pension

Deemed income: approx. $8,000–$10,000

Outcome:

Eligible for part Age Pension

Total income = pension + super withdrawals

Key insight:

Actual withdrawals don’t directly reduce the pension.

Example 2: Higher Balance (No Pension → Partial Later)

Scenario:

Couple with $800,000 combined

Initially above threshold

Outcome at start:

No Age Pension

After 3–5 years:

Balance reduces to $600,000

New outcome:

Eligible for part pension

Strategy:

Drawdown gradually to move into eligibility range.

Example 3: Low Balance (Near Full Pension)

Scenario:

Single retiree

$250,000 in pension account

Withdraws minimum only

Outcome:

Close to full Age Pension

Super acts as a supplement

This is where:

Pension provides stability

Super provides flexibility

Assets Test vs Income Test: Which One Applies?

Centrelink applies both:

Test | What It Looks At |

Assets test | Total value of your pension account |

Income test | Deemed income from that balance |

You receive the lower pension result from the two tests.

Minimum Drawdown Rules (Important)

You must withdraw a minimum percentage each year:

Age | Minimum Drawdown |

Under 65 | 4% |

65–74 | 5% |

75–79 | 6% |

(Subject to current ATO rules)

This ensures:

Your super is gradually used

It’s not just sitting untouched

Strategic Insights Most People Miss

1. Withdrawals Don’t Equal Assessable Income

Centrelink ignores your actual drawdowns.

2. Lowering Your Balance Can Increase Pension

Over time:

Less assets = higher pension

3. Structure Matters More Than Amount

Where your money sits:

Super

Cash

Investments

Can change outcomes significantly.

4. Timing Is Everything

The interaction evolves over:

Years, not months

Common Mistakes

1. Taking too little or too much

No strategy = inefficient income.

2. Misunderstanding deeming

People assume real income is assessed.

3. Ignoring thresholds

Small changes can shift eligibility.

4. Not reviewing annually

Your pension should be reviewed every year.

When Should You Get Advice?

You should consider professional advice if:

You’re starting an account-based pension

You’re close to Age Pension thresholds

You want to optimise total retirement income

Because small structural changes can mean:

Thousands per year difference

FAQs

1. Does an account-based pension reduce my Age Pension?

Yes, but indirectly. It is counted as an asset and deemed for income, which can reduce your entitlement.

2. Does Centrelink use my actual pension withdrawals?

No. Centrelink applies deeming rates to estimate income.

3. Can I still get a full Age Pension with super?

Yes, if your total assets are below the lower threshold.

4. Should I withdraw more to reduce my assets?

It depends. The goal is to maximise total income, not just pension eligibility.

5. What happens as my pension balance decreases?

You may become eligible for a higher Age Pension over time.

6. Is my home counted in the assets test?

Your principal residence is generally exempt (subject to current Services Australia rules).

7. What is the biggest advantage of an account-based pension?

Flexibility. You control how much income you withdraw.

Not Sure How Your Super Impacts Your Age Pension?

The way your account-based pension is structured can significantly affect your retirement income.

At What If Advice, we help Australians:

Understand Centrelink rules clearly

Structure pension drawdowns effectively

Maximise total retirement income

Book a strategy session to get clarity on your position and next steps.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional advice. Rules relating to Centrelink, the ATO, and Services Australia are subject to change.