Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

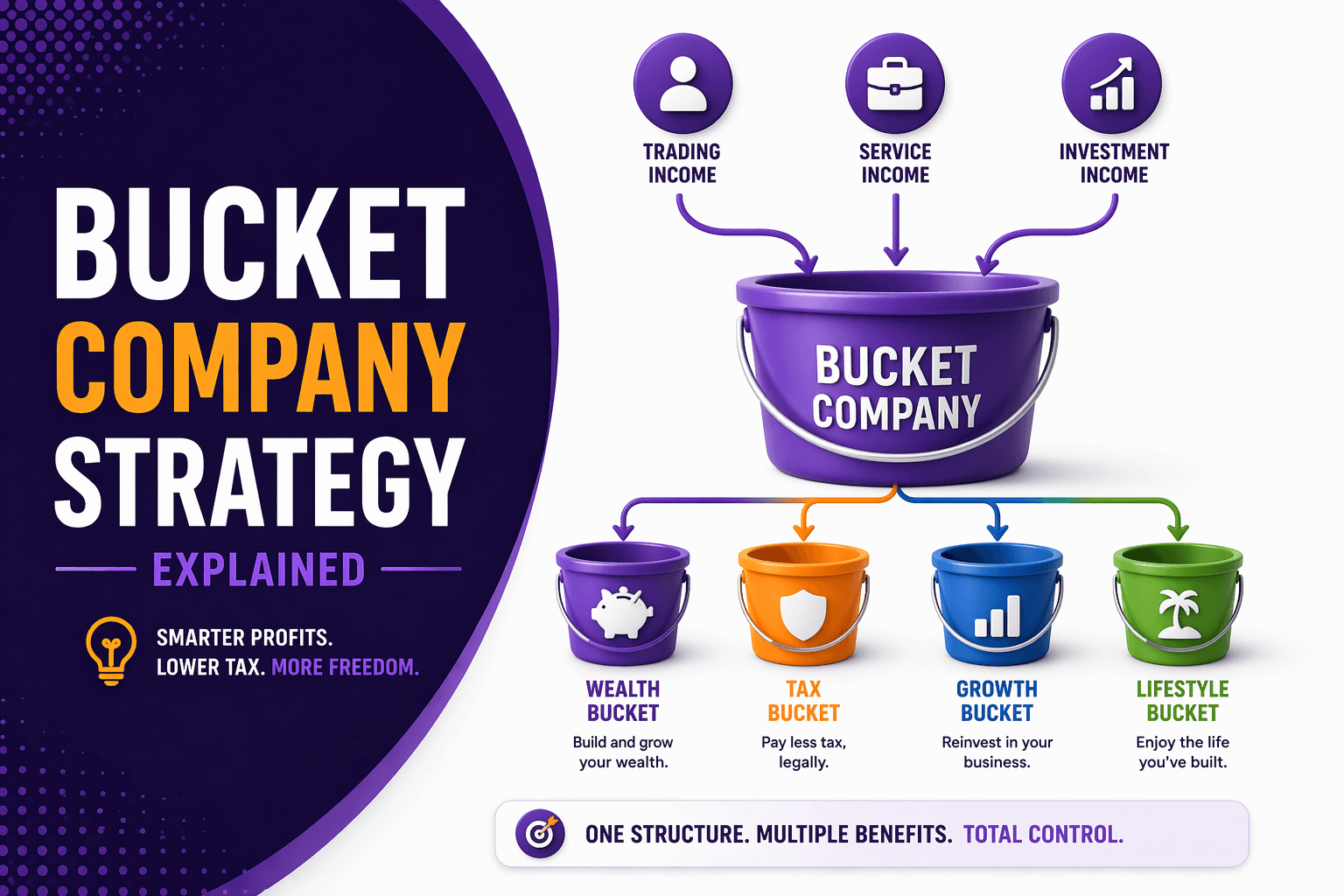

Bucket Company Strategy Explained for Australian Business Owners

A bucket company is one of the most common tax strategies used with discretionary trusts in Australia.

Used correctly, it can:

Cap tax at the company rate (typically 25%)

Retain profits for future use

Provide flexibility in distribution timing

Used incorrectly, it can:

Trigger Division 7A issues

Create compliance problems

Lead to unexpected tax outcomes

Here’s how it actually works.

What Is a Bucket Company?

A bucket company is:

A company used as a beneficiary of a discretionary trust to receive income distributions.

Instead of distributing all trust income to individuals:

Some income is distributed to a company

Tax is paid at the company rate

Why Use a Bucket Company?

1. Cap Tax at a Lower Rate

Individuals:

Taxed up to 45% + Medicare levy

Companies:

Typically taxed at 25% (for base rate entities, subject to ATO rules)

This creates a tax deferral opportunity

2. Retain Profits for Future Use

Income distributed to a bucket company:

Can be retained

Used later for:

Investment

Business expansion

Future dividends

3. Flexibility in Income Distribution

A discretionary trust allows:

Distribution to individuals or companies

You can choose:

Who receives income each year

Based on tax position

How a Bucket Company Structure Works

Basic Setup

Business operates through a trust

Trust generates profit

Income is distributed:

To individuals (up to tax thresholds)

Excess to bucket company

Example

Trust profit: $200,000

Distribution:

$80,000 to individual (lower tax bracket)

$120,000 to bucket company

Outcome:

Reduced overall tax burden

Remaining funds taxed at company rate

Where Things Get Risky: Division 7A

Here’s where people get into trouble.

If profits are:

Distributed to a company

But not actually paid (left as unpaid entitlement)

This creates:

Unpaid Present Entitlement (UPE)

ATO may treat this as:

A loan to the trust

Which can trigger:

Division 7A

What This Means

If not structured correctly:

The amount can be treated as a deemed dividend

Taxed in the hands of shareholders

How to Stay Compliant

1. Manage UPEs Properly

Options include:

Paying the amount to the company

Placing funds on complying loan terms

2. Use Division 7A Loan Agreements

If funds remain in the trust:

Must follow:

ATO benchmark interest rate

Minimum yearly repayments

Formal agreement

3. Keep Clean Documentation

You need:

Distribution resolutions

Loan agreements

Accurate accounting records

4. Review Annually

Bucket company strategies are:

Not “set and forget”

Must be reviewed each financial year

When a Bucket Company Makes Sense

It may be suitable if:

You operate through a discretionary trust

You’re generating significant profit

You want to defer personal tax

You’re reinvesting profits

When It May Not Be Suitable

Avoid or reconsider if:

Profits are low

You need all income personally

You don’t want additional compliance

You don’t understand Division 7A risks

Example Scenario

Without Bucket Company

Profit: $180,000

Distributed to individual

Taxed at marginal rates

With Bucket Company

$90,000 to individual

$90,000 to company

Outcome:

Lower immediate tax

Funds retained in company

Common Mistakes

1. Treating Company Money as Personal Money

This triggers Division 7A issues.

2. Ignoring UPE Rules

This is the most common compliance failure.

3. No Strategy for Retained Funds

Money sits idle with no purpose.

4. Overcomplicating Structures

More entities ≠ better outcomes.

Strategic Insight: Bucket Companies Are About Timing, Not Avoidance

This is not:

“Avoid tax forever”

It’s:

“Control when and how tax is paid”

Used correctly:

You defer tax

You manage cash flow

You build long-term wealth

Used poorly:

You create compliance risks

When Should You Get Advice?

You should seek advice if:

You operate a trust

Your profits are growing

You’re considering a company beneficiary

You’re unsure about Division 7A

Because:

The structure only works if it’s implemented properly.

FAQs

1. What is a bucket company?

A company used as a beneficiary of a trust to receive income distributions and cap tax at company rates.

2. How does a bucket company reduce tax?

By distributing income to a company taxed at a lower rate than individual marginal rates.

3. What is a UPE?

An unpaid present entitlement, income allocated but not paid to the beneficiary.

4. Does Division 7A apply to bucket companies?

Yes, particularly where UPEs are involved.

5. Can I access money in a bucket company?

Yes, but it must be done properly (e.g. dividends or loans).

6. Is a bucket company always beneficial?

No. It depends on profit levels, structure, and strategy.

7. What is the biggest risk?

Incorrect handling of UPEs and Division 7A compliance.

Using a Bucket Company or Thinking About It?

This strategy can be powerful, but only when structured correctly.

At What If Advice, we help business owners:

Implement bucket company strategies properly

Manage Division 7A compliance

Align tax strategy with long-term goals

Book a strategy session to ensure your structure works efficiently and compliantly.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional advice. Taxation laws, including Division 7A and trust distribution rules, are subject to change and ATO interpretation.