Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

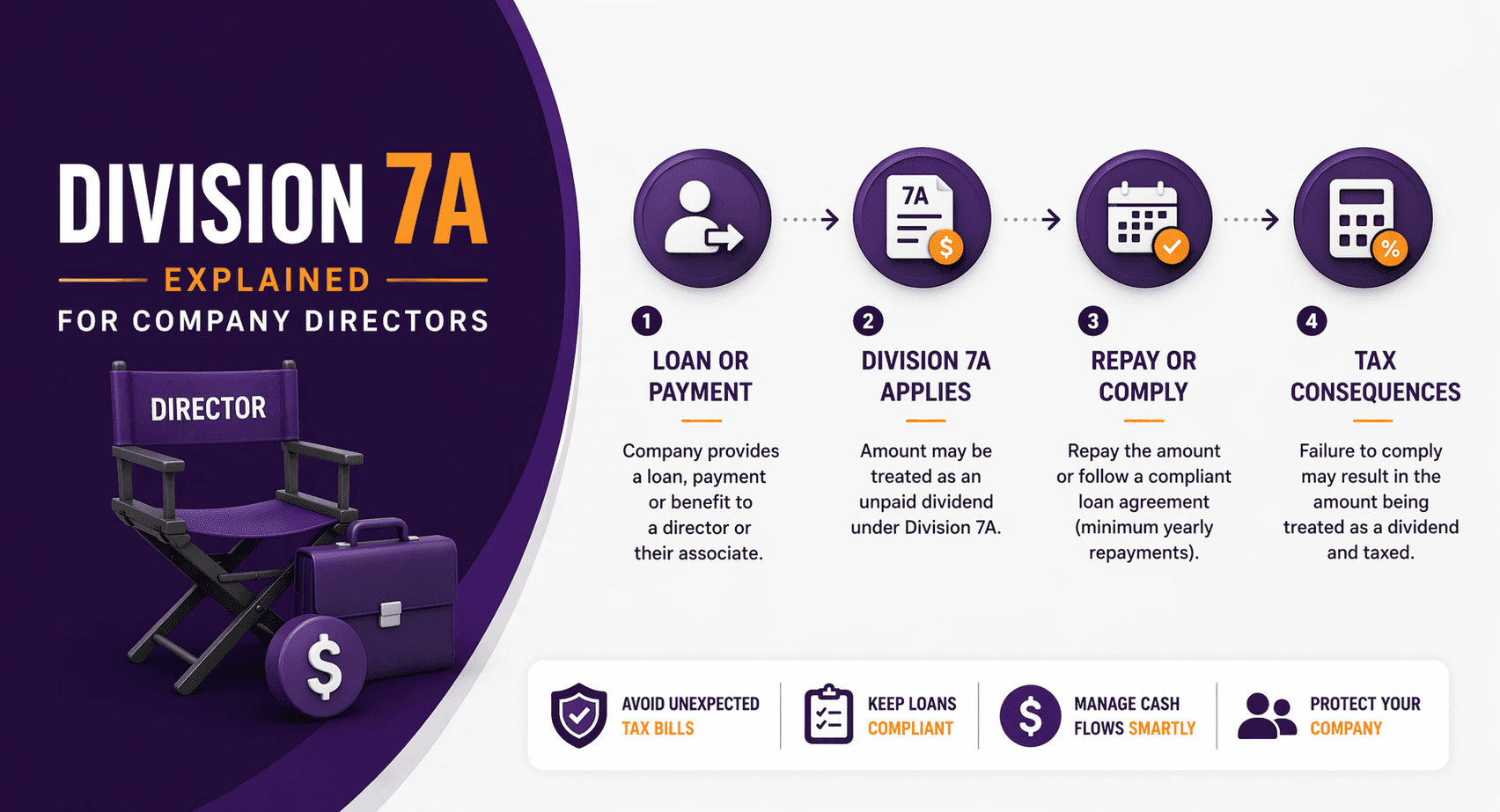

Division 7A Explained for Company Directors (Australia)

If you take money out of your company without structuring it properly, the ATO may treat it as a taxable dividend under Division 7A.

No paperwork. No planning. No mercy.

Division 7A exists to stop directors and shareholders from accessing company profits tax-free. If you’re running a company, you need to understand how it works.

What Is Division 7A?

Division 7A is part of the Income Tax Assessment Act 1936.

It applies when a private company provides:

Loans

Payments

Debt forgiveness

to:

Shareholders

Associates of shareholders

If not structured correctly, the ATO treats these as unfranked dividends.

Meaning:

You pay tax on the amount personally, without franking credits.

Why Division 7A Exists

Simple reason:

To stop people doing this:

Company earns profit

Instead of paying dividends- “loan” to director

Director uses money tax-free

Division 7A shuts that down.

When Division 7A Is Triggered

1. You Take Money Out of the Company

Example:

Director withdraws $50,000 for personal use

No salary, no dividend, no loan agreement

This can trigger Division 7A.

2. You Use Company Funds Personally

Example:

Company pays for personal expenses

No proper accounting treatment

3. You Have an Unpaid Loan Balance

If you owe money to your company at year-end:

It may be treated as a deemed dividend

4. Unpaid Present Entitlements (UPEs)

Where:

A trust allocates income to a company

But doesn’t actually pay it

This can also trigger Division 7A (subject to current ATO guidance).

What Happens If Division 7A Applies

The amount is treated as a:

Deemed unfranked dividend

This means:

Added to your personal income

Taxed at your marginal rate

No franking credits

Example

Scenario | Outcome |

Withdraw $80,000 | No structure |

ATO treatment | $80,000 deemed dividend |

Tax result | Full personal tax payable |

Not exactly the clever workaround people think it is.

How to Avoid Division 7A (Properly)

Option 1: Declare a Dividend

Formal dividend declaration

Includes franking credits (if available)

✔ Clean

✖ Still taxable

Option 2: Pay Salary or Wages

PAYG withholding applies

Tax deductible to company

✔ Structured

✔ Compliant

Option 3: Use a Complying Loan Agreement

This is the most common strategy.

To be compliant:

Written loan agreement

Interest charged at ATO benchmark rate

Minimum yearly repayments

Division 7A Loan Rules (Key Requirements)

Requirement | Detail |

Interest rate | ATO benchmark rate (updated yearly) |

Term | Max 7 years (unsecured) or 25 years (secured) |

Repayments | Minimum yearly repayments required |

Documentation | Must be in place before tax deadline |

Miss any of these - Division 7A risk.

Minimum Yearly Repayments (MYR)

If you have a Division 7A loan:

You must make minimum repayments each year

Fail to do so:

Entire loan can be treated as a deemed dividend

Common Mistakes Directors Make

1. Treating the company as a personal bank

It’s not. The ATO agrees.

2. No loan agreement in place

Handshake agreements don’t count.

3. Missing minimum repayments

This is one of the most common triggers.

4. Poor bookkeeping

If it’s not recorded properly, it’s a problem.

5. Ignoring UPE risks

Trust-company structures need careful handling.

Practical Scenario

Director Withdrawal Without Planning

Director withdraws $100,000

No loan agreement

No dividend declared

Result:

$100,000 taxed personally

No franking credits

Potential cash flow pressure

Director Withdrawal With Strategy

Loan agreement in place

Interest applied

Minimum repayments scheduled

Result:

No immediate tax

Structured repayment

Same action. Completely different outcome.

Strategic Insight: Division 7A Is a Timing and Structure Game

This isn’t about avoiding tax.

It’s about:

Timing income correctly

Structuring withdrawals properly

Managing cash flow

Done right:

You stay compliant

You stay flexible

Done wrong:

You get hit with unexpected tax bills

When Should You Get Advice?

You should seek advice if:

You’re taking money from your company

You have a shareholder loan balance

You operate a trust-company structure

You’re unsure about compliance

Because fixing Division 7A issues later is:

Messy

Expensive

Sometimes too late

FAQs

1. What is Division 7A in simple terms?

It’s a rule that prevents private company profits being accessed tax-free through loans or payments to shareholders.

2. What is a deemed dividend?

An amount treated as a dividend for tax purposes, even if no formal dividend was declared.

3. Can I borrow money from my company?

Yes, but only if it’s structured under a complying Division 7A loan agreement.

4. What happens if I don’t repay the loan?

The unpaid amount may be treated as a taxable dividend.

5. What is the Division 7A interest rate?

It’s the ATO benchmark interest rate, updated annually.

6. Does Division 7A apply to trusts?

Yes, particularly with unpaid present entitlements (UPEs), subject to ATO rules.

7. Can Division 7A be fixed after year-end?

Sometimes, but options are limited and often require professional advice.

Taking Money Out of Your Company? Do It Properly

Division 7A issues are one of the most common, and avoidable; tax problems for directors.

At What If Advice, we help business owners:

Structure withdrawals correctly

Stay compliant with ATO rules

Avoid unexpected tax bills

Book a strategy session to make sure your structure works for you, not against you.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional advice. Taxation laws, including Division 7A, are subject to change and ATO interpretation.