Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

Financial Planner Melbourne CBD: What to Expect

You've decided you need a financial planner. Maybe you've just had a baby, sold a business, hit a promotion, or finally faced the fact that your super balance isn't going to retire you on its own.

So you Google "financial planner Melbourne CBD" and get hit with 200 results. Big firms, boutique practices, robo-advisors, accounting firms with a planning arm, all promising clarity, expertise, and outcomes.

How do you choose? What does the process actually look like? What will it cost, and how do you tell good advice from a glossy sales pitch? This guide walks you through exactly what to expect: fees, process, red flags, and all.

Quick Answer

Here's what to know before engaging a financial planner in Melbourne CBD:

A typical Statement of Advice in Melbourne in 2026 costs $3,500 to $6,000 for a one-off engagement, or $4,000 to $6,000 a year for ongoing advice

The CBD is home to most of Victoria's largest planning firms, plus boutique practices clustered around Collins Street, Bourke Street, and Southbank

Expect 2 to 4 meetings before you receive your written plan

Quality firms operate on fee-for-service, not commissions, and will disclose their fees clearly upfront

The first consultation is usually free and is more about fit than advice

Bottom line: Good Melbourne CBD planners charge real money for real value. The fee shouldn't be a surprise, and the value should be obvious within the first meeting.

Why Melbourne CBD Has Become Australia's Second Advice Hub

Melbourne CBD is the financial heart of Victoria. Walk down Collins Street, affectionately known as "the Paris end" near Spring Street and the financial corridor running west toward Docklands, and you'll pass dozens of financial planning firms, often tucked above law firms, accountants, and corporate offices.

The geography matters. The advice industry clusters in the CBD because that's where its clients work:

Corporate professionals in legal, accounting, banking, and consulting firms across Collins, Bourke, and William Streets

Healthcare specialists working at Royal Melbourne Hospital and the Parkville biomedical precinct, just north of the CBD

Tech and startup workers based in Cremorne, Richmond, and Southbank with significant equity packages

Pre-retirees in the inner suburbs (South Yarra, East Melbourne, Carlton, Albert Park) with sizeable super balances and complex tax situations

Business owners and self-employed professionals running practices through CBD-adjacent suburbs like Fitzroy and South Melbourne

That client mix shapes the advice. Melbourne CBD planners typically deal with higher-than-average incomes, complex remuneration structures (RSUs, ESOPs, bonuses), property portfolios, and Division 293 tax issues, not simple superannuation rollovers.

Bottom line: A CBD-based planner is generally better suited to professional and corporate complexity than a generalist suburban firm. But the fees reflect that.

What "Financial Planning" Actually Covers

A common misconception: financial planners just pick investments. That's maybe 15% of what a good planner does.

A comprehensive Melbourne CBD financial planner will work across:

Strategic financial planning, setting goals, building a roadmap, modelling outcomes over 10, 20, 30 years

Superannuation strategy, including contributions, investment options, transition to retirement, and SMSF assessment

Tax-effective wealth building, using salary sacrifice, deductible contributions, family trust structures, and CGT planning

Investment advice, covering asset allocation, diversification, platform selection, and risk profiling

Insurance, including life, TPD, income protection, and trauma cover, structured inside or outside super

Retirement income planning, covering account-based pensions, drawdown strategy, and Age Pension integration

Estate planning integration, working with your lawyer on wills, binding death benefit nominations, and beneficiaries

Cashflow and debt strategy, including mortgage optimisation, debt recycling, and savings frameworks

Notice how few of those are about picking shares. The real value of a planner sits in structure, strategy, and behavioural coaching, not stock tips.

Bottom line: If a planner's pitch is mostly about investment returns, find a different planner. The structural work is where the wealth gets built.

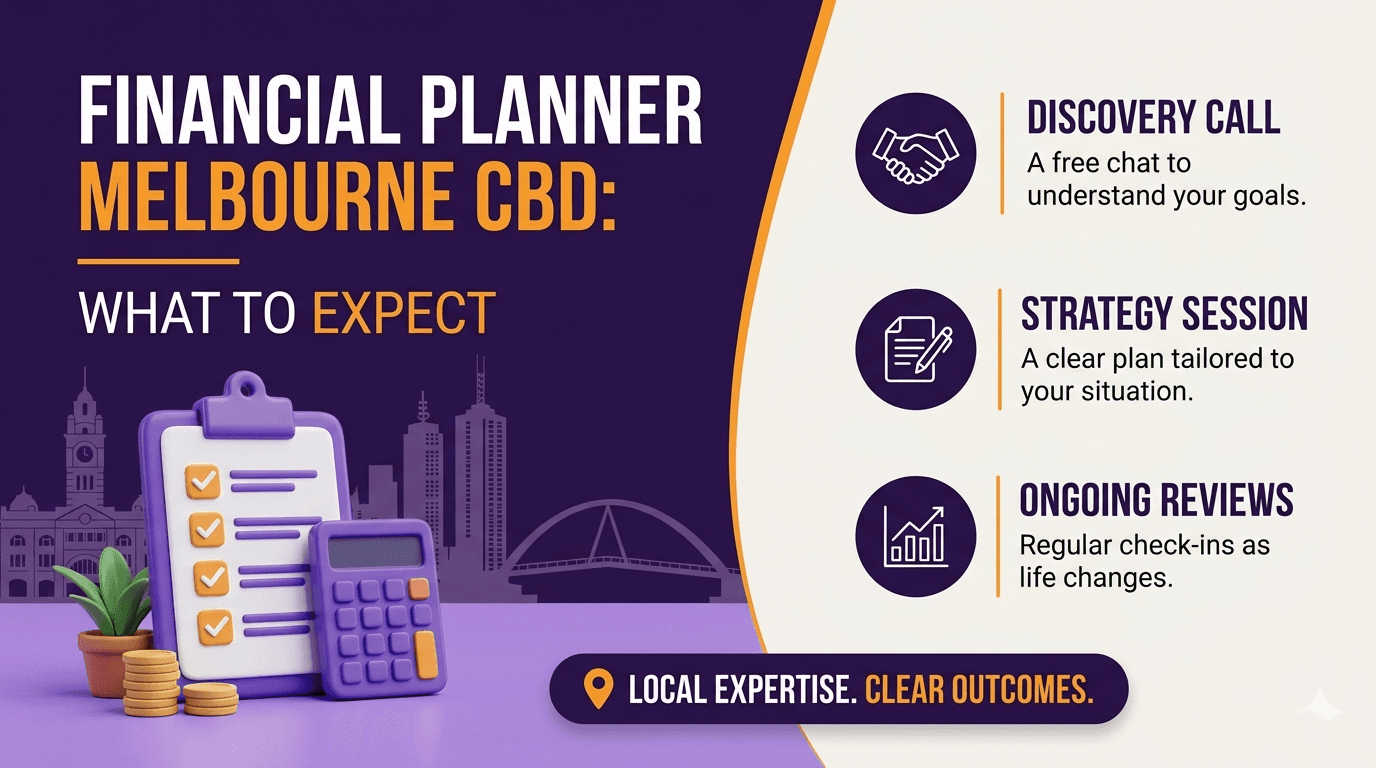

What the Process Actually Looks Like

Most quality Melbourne CBD planners follow a similar process, even if the branding differs. Here's what a typical engagement looks like end to end:

Stage | What Happens | Cost |

1. Discovery call | 15 to 30 minute phone call to confirm fit and scope | Usually free |

2. Initial meeting | 60 to 90 minute meeting in their office or online; you share your situation, they explain their approach | Usually free, though some charge $95 to $330 |

3. Fact-find and research | You provide documentation; they analyse your full situation | Included in plan fee |

4. Strategy meeting | They walk you through proposed strategies before writing the plan | Included |

5. Statement of Advice (SOA) | Written, formal, compliant document with specific recommendations | $3,500 to $6,000 typical |

6. Implementation | Executing the advice: rollovers, applications, contribution changes | Sometimes included, sometimes extra |

7. Ongoing review | Annual or bi-annual reviews and ongoing tactical advice | $4,000 to $6,000/year typical |

The whole process typically takes 1 to 3+ months from start to finish. Quality planners are in high demand and don't churn out plans like fast food.

Bottom line: Good advice takes time. If a planner promises a full SOA in two weeks, ask hard questions about how thorough it really is.

What It Costs in 2026

Fees are the question everyone wants to ask but few do. Let's be direct.

In Melbourne CBD in 2026, expect:

Initial consultation: free, or around $200 to $400 at some firms

One-off Statement of Advice: $3,500 to $6,000 for typical complexity

Simple single-issue advice: $1,500 to $2,500 (one super rollover, one insurance review)

Ongoing advice: $4,000 to $6,000 per year, sometimes more for complex SMSF or business owner clients

Hourly rates (less common): $200 to $500 per hour

Percentage of assets under management: 0.5% to 1.5% per year, though pure fee-for-service is increasingly the norm

A few things have changed in 2026 worth knowing:

The Statement of Advice format is being reformed. New rules will replace the long and confusing "Statement of Advice" with shorter, clearer records

Insurance commissions now require explicit consent. Advisers must get your explicit written consent before they accept any payment from an insurer

Advice fees are partially tax-deductible when they relate to managing existing investments that produce assessable income or for tax planning advice, following Taxation Determination TD 2024/7

Bottom line: Quality advice in Melbourne CBD costs real money, but a good planner pays for themselves many times over through tax savings, structural improvements, and avoiding expensive mistakes.

What Good Looks Like (And What to Avoid)

Not all planners are equal. Here's how to spot the good ones, and what to walk away from.

Signs of a quality planner:

They listen far more than they talk in the first meeting

They explain fees clearly, in writing, before you commit

They're listed on the ASIC Financial Advisers Register (check moneysmart.gov.au)

They use fee-for-service, not product commissions

They explain trade-offs honestly, not just upside

They reference your actual situation, not generic case studies

Red flags to walk away from:

They lead with investment products, not strategy

They're vague about fees or insist on talking numbers later

They promise specific returns or "guaranteed" outcomes

They pressure you to sign at the first meeting

They don't ask about your goals, only your assets

They aren't on the ASIC register

Bottom line: Trust your gut after the first meeting. If something feels off (pressure, vagueness, hard-sell), there are 200 other Melbourne CBD planners who won't make you feel that way.

Practical Examples

Example 1: Priya, 38, Senior Lawyer in Collins Street

Priya earns $220,000 at a top-tier Collins Street law firm. She has $310,000 in super, an apartment in South Yarra, and feels disorganised about her finances despite the income.

She engages a CBD planner with a $5,500 SOA fee. The planner's recommendations:

Salary sacrifice an extra $15,000 per year into super (utilising her full concessional cap)

Use carry-forward concessional contributions from prior years where eligible

Consolidate two old super accounts (saves $600/year in fees)

Review her income protection cover, currently underinsured for her income level

Build a debt recycling strategy against her South Yarra apartment

Outcome over 10 years: an estimated additional $280,000 in net wealth compared to her DIY trajectory, including tax savings, insurance optimisation, and accelerated super growth. The $5,500 fee paid for itself in year one through tax savings alone.

Example 2: Tom and Marcus, Mid-50s Couple from Albert Park

Tom is a CFO earning $280,000. Marcus runs a creative agency from Cremorne earning $140,000. Combined super: $680,000. They want to retire by 62 and travel.

They engage a CBD planner offering ongoing advice at $5,000/year. The strategy:

Maximise both concessional caps for 7 more years

Tom uses non-concessional contributions to pump after-tax savings into super

Both start a TTR pension at 60 to optimise tax in their final working years

Plan a phased retirement: Marcus winds the agency down gradually, Tom drops to 4 days then 3

Build a retirement income strategy that bridges from 62 to Age Pension eligibility at 67

Modelled outcome: combined balance of roughly $1.45M by 62, sustainable retirement income of $95,000+ per year until life expectancy. The ongoing fee of $5,000/year is a rounding error against the strategic value.

Common Mistakes Melbourne CBD Professionals Make

Choosing a planner based on office location alone. Just because they're 50 metres from your office doesn't make them right for you. Fit, expertise, and fee structure matter far more than the walk from your desk.

Not asking for fees in writing upfront. A good planner will quote you a fee before you've signed anything. If they're cagey about pricing, walk.

Confusing accountants with financial planners. Accountants handle tax compliance and historical reporting. Planners handle forward-looking strategy. They're complementary, not interchangeable.

Engaging a planner just to "pick investments." That's the lowest-value part of the job. The structural work covering super, tax, insurance, and estate is where the real value sits.

Ignoring conflicts of interest. Some "planners" are actually salespeople for specific products or platforms. Always ask: "How do you get paid?" If the answer involves commissions or product trails, dig deeper.

Not checking the ASIC register. Every legitimate financial adviser in Australia is listed on moneysmart.gov.au. If they're not there, they're not licensed. Walk away.

Going DIY when you shouldn't. High-income professionals with complex remuneration, equity packages, or business structures often lose more in tax inefficiency than a planner's annual fee, every single year.

FAQ

How much does a financial planner cost in Melbourne CBD? Expect $3,500 to $6,000 for a one-off Statement of Advice, or $4,000 to $6,000 per year for ongoing advice. Simple single-issue advice runs around $1,500 to $2,500. Complex situations such as SMSF, business owners, or blended families can run higher.

Are financial planning fees tax-deductible? Some are. Fees relating to managing existing investments that produce assessable income or for tax planning advice are generally deductible following Taxation Determination TD 2024/7. Initial advice on a new investment is typically not. Always check with your accountant (subject to current ATO rules).

How do I check if a financial planner is licensed? Visit the ASIC Financial Advisers Register at moneysmart.gov.au and search by name. Every legitimate planner in Australia must be listed there, with their education, experience, and any disciplinary history visible.

What's the difference between a financial planner and a financial adviser? In Australia, the terms are largely interchangeable. The protected term is "financial adviser" or "financial planner", and both require AFSL licensing, degree-level qualifications, and Continuing Professional Development. Marketing differences aside, the regulatory standards are the same.

Do I need a financial planner if I'm in an industry super fund? Not necessarily, but you'll likely benefit. Industry funds offer general advice limited to your account. A licensed planner looks across your entire situation: super, property, tax, insurance, Centrelink, estate, and spouse strategy. The whole picture matters more than the fund itself.

How long does the financial planning process take? From start to finish it can take 1 to 3+ months to receive your financial plan, get it going and have it in play. Good planners are in high demand and don't rush quality work. Plan ahead, and don't engage one the week before you need a decision.

Should I engage a planner at the start of my career or only later? Earlier than most people think. Even at 30, structural advice on super, insurance, and cashflow can add hundreds of thousands in lifetime wealth. The compounding works only if you start.

Ready to See What Quality Advice Looks Like?

Book a free 15-minute consultation with the team at What If Advice, with offices in Melbourne and Brisbane, and find out exactly what tailored advice would look like for your situation.

No pressure, no jargon, just a clear conversation about what's possible. Visit whatifadvice.com.au to book.

General Advice Disclaimer: This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions.