Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

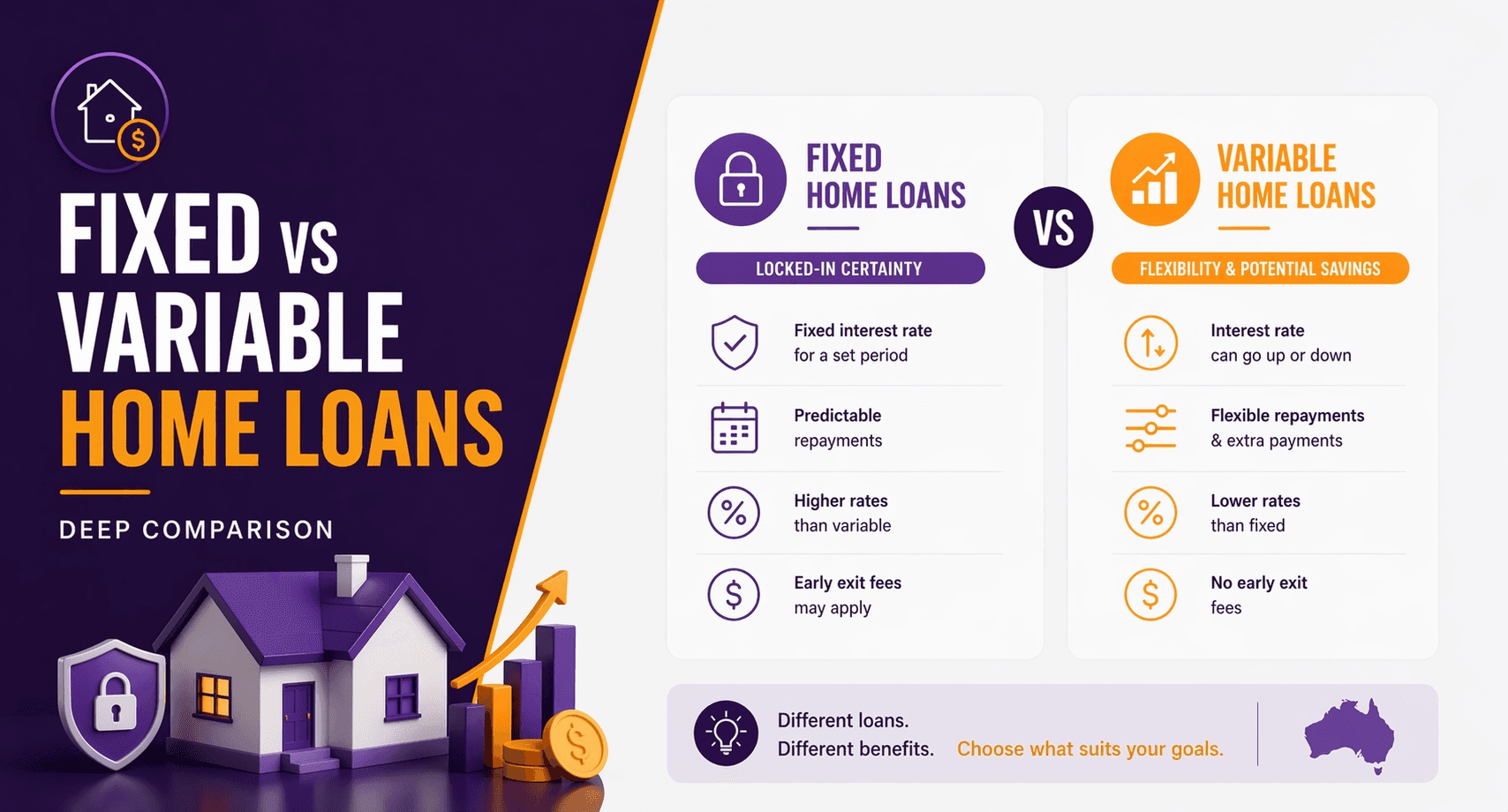

Fixed vs Variable Home Loans in Australia: Which Is Right for You?

Choosing between a fixed and variable home loan is one of the most important financial decisions you’ll make as a homeowner.

The short answer:

Fixed loans offer certainty

Variable loans offer flexibility

But the right choice depends on your risk tolerance, financial stability, and future plans.

What Is a Fixed Rate Home Loan?

A fixed rate home loan locks in your interest rate for a set period, typically 1 to 5 years.

Key features:

Repayments stay the same during the fixed period

Protected from interest rate increases

Limited flexibility

Example:

If you fix your loan at 5.80% for 3 years, your repayments won’t change, even if the RBA increases rates.

What Is a Variable Rate Home Loan?

A variable rate loan means your interest rate can move up or down, usually in line with RBA cash rate changes.

Key features:

Repayments can change

More flexibility

Access to features like offset accounts and redraw

Example:

If rates drop from 6.20% to 5.70%, your repayments decrease.

If they rise, your repayments increase.

Fixed vs Variable: Side-by-Side Comparison

Feature | Fixed Loan | Variable Loan |

Repayment certainty | High | Low |

Flexibility | Limited | High |

Extra repayments | Restricted | Usually allowed |

Break costs | Can be high | None |

Offset account | Rare | Common |

Benefit from rate drops | No | Yes |

Protection from rate rises | Yes | No |

When a Fixed Rate Loan May Suit You

A fixed loan may be appropriate if:

1. You need repayment certainty

If your budget is tight, knowing exactly what you’ll pay each month helps reduce stress.

2. You expect rates to rise

Fixing can protect you from increases (subject to market conditions).

3. You prefer stability over flexibility

You’re less concerned about features like redraw or offset.

When a Variable Rate Loan May Suit You

A variable loan may be suitable if:

1. You want flexibility

You can make extra repayments and access funds if needed.

2. You expect rates to fall

You benefit immediately from rate reductions.

3. You plan to pay off your loan faster

Extra repayments reduce interest over time.

What About a Split Home Loan?

Many Australians choose a split loan, combining both options.

Example:

50% fixed

50% variable

This allows you to:

Lock in part of your repayments

Keep flexibility with the rest

It’s a practical middle ground if you’re unsure.

The Hidden Risk: Break Costs on Fixed Loans

One of the biggest downsides of fixed loans is break costs.

If you:

Refinance

Sell your property

Switch lenders

You may face significant fees, especially if interest rates have dropped since you fixed.

These costs can run into thousands of dollars depending on timing and loan size.

How RBA Rate Changes Affect Your Loan

The Reserve Bank of Australia (RBA) influences variable rates through the cash rate.

When the RBA raises rates → lenders increase variable rates

When the RBA cuts rates → repayments may decrease

Fixed rates, however, are influenced by future market expectations, not just current RBA movements.

Key Question: Should You Fix Your Home Loan?

There’s no universal answer.

Instead, consider:

Your income stability

Your ability to handle repayment increases

Your long-term plans (sell, refinance, hold)

Current interest rate environment

A decision that feels “safe” today can become restrictive tomorrow.

Real-Life Scenario

Sarah and James (Brisbane, $750,000 loan):

Fixed option: 5.90% for 3 years

Variable option: 6.20%

They chose:

60% fixed → stability

40% variable → flexibility

Result:

Predictable repayments

Ability to make extra repayments

Reduced exposure to rate changes

FAQs

1. Is it better to fix or go variable in Australia right now?

It depends on your financial situation and outlook. Fixed offers certainty, while variable offers flexibility and potential savings if rates fall.

2. Can I switch from fixed to variable?

Yes, but break costs may apply depending on your lender and timing.

3. Are variable rates always cheaper?

Not always. Over time, they may be lower, but they come with volatility.

4. What is a split home loan?

A loan divided between fixed and variable portions to balance certainty and flexibility.

5. Do fixed loans allow extra repayments?

Usually limited, often capped annually (subject to lender terms).

6. How often do variable rates change?

They typically change when lenders respond to RBA cash rate decisions.

7. Is an offset account worth it?

For many borrowers, yes. It can reduce interest significantly over time if used effectively.

Not Sure Which Loan Structure Is Right for You?

Choosing between fixed and variable isn’t just about interest rates. It’s about aligning your loan with your financial strategy, risk tolerance, and future plans.

A poorly structured loan can cost thousands over time or limit your flexibility when you need it most.

If you’re unsure which option suits your situation, speaking with a qualified adviser can help you make a more confident, informed decision.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional financial advice. Information is subject to current ATO and Services Australia rules and may change over time.