Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

Fringe Benefits Tax Explained for Small Business Owners in Australia

If you employ staff and provide them with benefits beyond their wages, Fringe Benefits Tax is a compliance obligation you cannot afford to overlook. Many small business owners discover their FBT exposure only after an ATO review. That is not the ideal moment to learn how the system works.

FBT sits outside income tax, runs on a different year, and is calculated in a way that surprises most business owners the first time they see the numbers. The rate is 47%. The record-keeping requirements are real. And the exemptions, while genuinely useful, require planning to access correctly.

As registered tax agents working with business owners across Brisbane and Melbourne, this is one of the compliance areas we see catch people out most often, particularly trades businesses running work vehicles and professional services firms with staff entertainment budgets. This guide explains what FBT is, what triggers it for small businesses, how the calculation works, what is exempt, and what you need to do to stay on the right side of the ATO.

TL;DR: The Key Points

Here is what you need to know before you read another word:

FBT is paid by the employer, not the employee, on certain non-cash benefits provided to employees and their associates

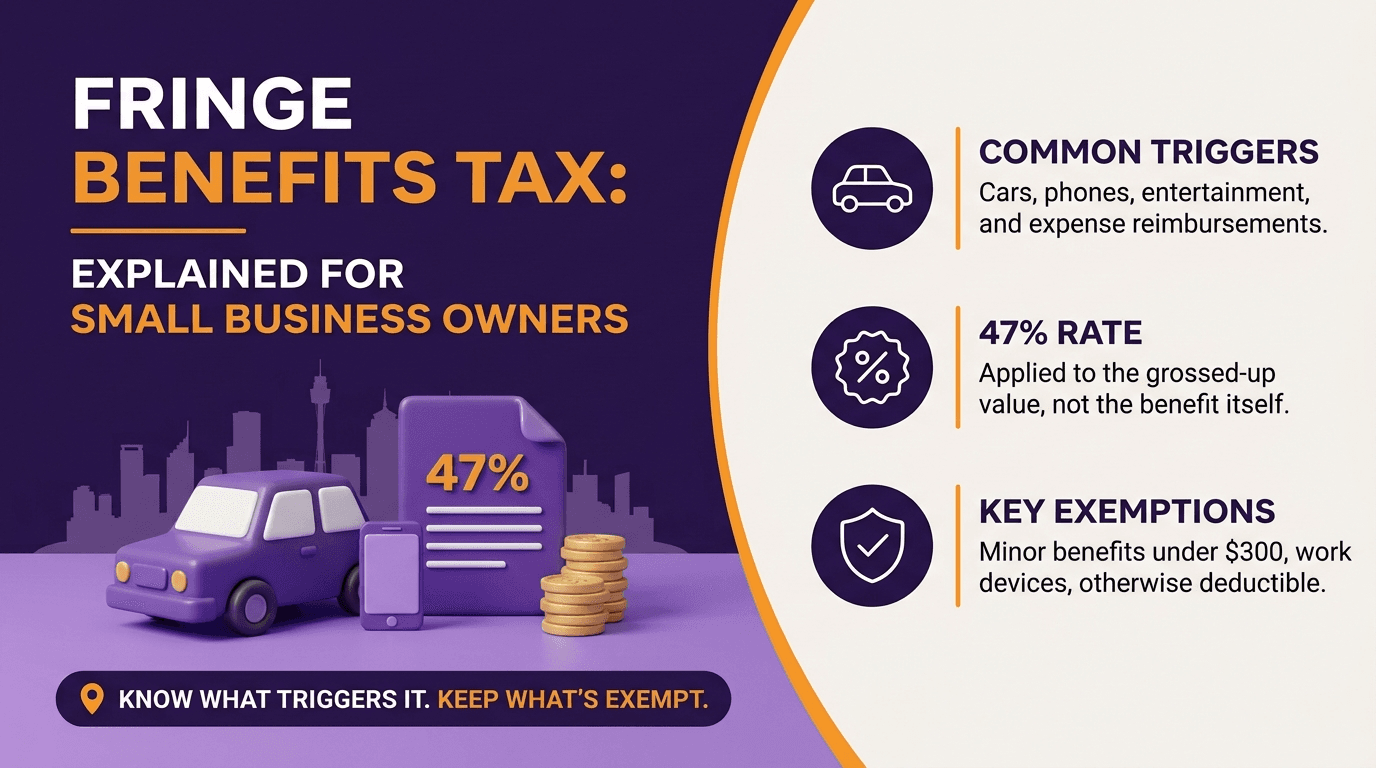

The FBT rate is 47%, applied to the grossed-up taxable value of the benefit

The FBT year runs from 1 April to 31 March, not the standard financial year

Common triggers include cars, car parking, loans, entertainment, and personal expense reimbursements

A minor benefits exemption applies to benefits valued at less than $300 (GST-inclusive) where the benefit is infrequent and irregular

Employee contributions toward a benefit reduce the taxable value before FBT is calculated

Record-keeping is mandatory and must be in place before you lodge your return

FBT returns are generally due 21 May following the end of the FBT year, or later if lodged through a registered tax agent

Jump to a Section

What Is Fringe Benefits Tax?

Who Pays FBT and Who Is Affected?

The FBT Year and Key Dates

What Triggers FBT? Common Benefits Explained

How Is FBT Calculated?

FBT Exemptions and Reductions

FBT Record-Keeping Obligations

FBT Returns and Registration

Common FBT Mistakes Small Business Owners Make

FAQ

What Is Fringe Benefits Tax?

Fringe Benefits Tax is a tax employers pay on certain non-cash benefits they provide to employees or their associates, such as a spouse or family member. It is entirely separate from income tax and the liability sits with the employer. The employee does not pay FBT directly, although benefits above a certain threshold must be reported on the employee's income statement as a reportable fringe benefits amount, which can affect income tests for Medicare levy surcharge, HECS-HELP repayments, and some government payments.

The ATO introduced FBT to prevent employers and employees from structuring remuneration in ways that reduced income tax. Without it, paying an employee partly in wages and partly in untaxed benefits would create a clear tax advantage over a straight salary. FBT closes that gap.

For small business owners, FBT becomes relevant any time the business provides something of value to an employee beyond their cash wages, whether that is a company car, a staff lunch, a reimbursed personal expense, or a loan at a low interest rate.

Bottom line: FBT is the employer's tax on non-cash benefits provided to employees. Understanding what triggers it is the first step to managing the liability and accessing the exemptions that legitimately reduce it.

Who Pays FBT and Who Is Affected?

The employer pays FBT. If you operate as a company, trust, or partnership that employs people, FBT applies to benefits you provide to those employees. It also applies to benefits provided to associates of employees, including a company car made available to an employee's spouse or family member.

If you are a sole trader with no employees, FBT does not apply to benefits you provide to yourself. If you employ others, it can apply to benefits provided to them.

There is no small business exemption from FBT itself. Certain specific exemptions reduce or eliminate FBT on individual types of benefits, but the tax applies equally to a two-person business and a two-hundred-person business.

The FBT Year and Key Dates

The FBT year runs from 1 April to 31 March, which is different from the standard Australian financial year ending 30 June. This distinction affects record-keeping, calculations, and lodgement timing.

We are currently in the 2026-27 FBT year (1 April 2026 to 31 March 2027).

Key dates to know:

FBT year: 1 April to 31 March

FBT return due date: generally 21 May (for self-lodgers)

Extended due date: later in the calendar year if lodging through a registered tax agent (confirm the exact extended date for the current FBT year with your agent)

FBT instalments: businesses whose FBT liability exceeded $3,000 in the prior year may be required to pay quarterly PAYG instalments

A benefit provided in March falls in the current FBT year. A benefit provided in April falls in the next FBT year. That timing distinction matters for both liability and record-keeping.

What Triggers FBT? Common Benefits Explained

Most small business owners are surprised by how many common business practices create an FBT liability. Here are the benefits most frequently relevant to small businesses.

Car fringe benefits. Providing a car to an employee, or making one available for private use, is one of the most common FBT triggers. A company car that an employee can drive home, use on weekends, or take on personal trips creates a car fringe benefit for every day it is available for private use.

Two methods apply for calculating the taxable value of a car fringe benefit:

Method | How It Works | When It Tends to Work Best |

Statutory formula | Applies a fixed 20% rate to the car's base value | Cars with lower business use or where no logbook has been maintained |

Operating cost | Applies the private-use percentage to total running costs | Cars with high business use supported by a valid logbook |

The operating cost method can significantly reduce FBT where business use is high, but it requires a logbook maintained for at least 12 consecutive weeks and updated every 5 years (or when circumstances change materially).

Electric vehicles: eligible low-emission vehicles, including certain battery electric and plug-in hybrid vehicles, may be exempt from FBT subject to conditions and current ATO rules. Eligibility depends on the vehicle type, the purchase price, and the relevant FBT year. Seek specific advice before assuming an electric vehicle qualifies.

Car parking fringe benefits. Providing a car park to an employee can trigger FBT where a commercial parking station within 1 kilometre of the work location charges more than the ATO's current car parking threshold. The taxable value is based on the commercial parking rate and the number of days the park is available.

Small businesses that do not have a commercial parking station within 1 kilometre of the work location, or where the parking is provided in a location that falls outside the definition, may not have a car parking fringe benefit. The conditions are specific and worth confirming with a registered tax agent.

Expense payment fringe benefits. Reimbursing an employee's personal expenses, or paying a bill on their behalf, creates an expense payment fringe benefit. Common examples include:

Paying or reimbursing a personal phone bill

Covering gym membership fees

Reimbursing school fees for an employee's child

Paying a personal insurance premium

Where the expense is wholly work-related and the employee could have claimed it as a tax deduction themselves, the otherwise deductible rule may eliminate the FBT. Where there is a private component, FBT applies to that proportion.

Loan fringe benefits. Providing an employee with a loan at an interest rate below the ATO's benchmark interest rate creates a loan fringe benefit. The taxable value is the difference between what the employee pays and what they would have paid at the benchmark rate.

Business owners who have lent money to employees, provided interest-free payment arrangements, or paid personal debts on an employee's behalf should review whether this applies to their arrangements.

Living-away-from-home allowances. Paying an allowance, or reimbursing accommodation and food costs, for an employee who temporarily relocates for work creates a living-away-from-home fringe benefit. The rules are detailed and depend on whether the employee maintains a home elsewhere, the duration of the arrangement, and strict substantiation requirements. This is a common trigger in construction, professional services, and project-based industries.

Entertainment benefits. Providing meals, drinks, or entertainment to employees can create a meal entertainment fringe benefit. Key points for small businesses:

Staff functions where the cost per head exceeds the minor benefits threshold can trigger FBT

A business lunch attended by both employees and clients may create FBT on the employee portion

Food and drink consumed on business premises as part of a working meal is generally treated differently to restaurant entertainment

Entertainment-related FBT is an area where many small businesses create a liability without realising it, particularly around year-end staff events.

Bottom line: Cars, expense reimbursements, entertainment, and loans are the four most common FBT triggers for small businesses. Reviewing your current employee benefits against these categories is the right starting point.

What if the most generous things you do for your team are also creating an unexpected tax bill? FBT is exactly that situation. Understanding the rules puts you back in control.

Not sure whether your current employee benefits are triggering FBT? The registered tax agents at What If Advice can review your arrangements and identify your exposure before the next return is due. Call 1800 942 843 or email tax@whatifadvice.com.au.

How Is FBT Calculated?

FBT calculation involves a concept most business owners find counterintuitive: the grossed-up value.

The ATO grosses up the taxable value of the benefit to represent the gross income an employee would have needed to earn, and pay income tax on, to fund the same benefit from their own after-tax wages. The FBT rate of 47% is then applied to this grossed-up amount.

Two gross-up rates apply for the 2026-27 FBT year:

Rate Type | When It Applies | 2026-27 Rate |

Type 1 (higher gross-up) | Business can claim a GST input tax credit on the benefit | 2.0802 |

Type 2 (lower gross-up) | Business cannot claim a GST input tax credit on the benefit | 1.8868 |

These rates are unchanged from the 2025-26 FBT year, but gross-up rates are reviewed each year, so always confirm the current figures before lodging.

A simple example:

A business provides an employee with a laptop worth $2,200 (GST-inclusive) for private use. The business can claim the GST credit (Type 1 applies):

Taxable value: $2,200

Gross-up factor: 2.0802

Grossed-up value: $2,200 x 2.0802 = $4,576

FBT payable: $4,576 x 47% = $2,151

For a $2,200 benefit, the employer pays $2,151 in FBT. That is why FBT surprises so many business owners when they first run the numbers.

Employee contributions reduce this figure. If the employee contributes $500 toward the benefit, the taxable value drops to $1,700 before grossing up, reducing the FBT proportionally. Structuring employee contributions is one of the most practical ways to reduce FBT liability.

FBT Exemptions and Reductions

Several exemptions and reductions apply to benefits commonly provided by small businesses. Getting these right is where good FBT planning delivers real savings.

Minor benefits exemption. A benefit is exempt from FBT if its GST-inclusive value is less than $300 and it would be unreasonable to treat it as a fringe benefit given its infrequent and irregular nature. Both conditions must be satisfied.

This exemption is commonly used for:

Occasional gifts to employees (such as a Christmas gift under $300)

Infrequent bottles of wine or flowers

One-off meals or entertainment under the threshold

The exemption does not apply to salary-packaged benefits or benefits provided as part of a regular arrangement. Each benefit is assessed individually. Providing the same employee with a $290 gift every month does not qualify for the exemption because the pattern makes it unreasonable to treat each one as minor and infrequent.

The threshold is less than $300, not $300. A benefit valued at exactly $300 does not qualify.

Work-related items exemption. Certain work-related items provided primarily for use in the employee's employment are exempt from FBT, including:

Portable electronic devices such as laptops, tablets, and mobile phones (primarily for work use)

Tools of trade

Computer software

Protective clothing

Briefcases

The standard rule limits the exemption to one device per employee per FBT year for items with substantially identical function. Small business entities with aggregated annual turnover under $50 million can exempt multiple devices of the same type per employee per year, which is a meaningful advantage for businesses equipping staff with both a laptop and a phone.

The device must be primarily for work use. Providing a personal laptop as a secondary device for an employee who has little work need for it does not qualify.

Otherwise deductible rule. Where an employee could have claimed the expense as a tax deduction if they had paid it themselves, the taxable value of the fringe benefit is reduced accordingly, sometimes to zero. This is why reimbursing work-related subscriptions, professional memberships, and genuinely work-specific equipment often creates no FBT.

The rule applies only where the expense would be fully deductible to the employee. A mixed personal and work expense creates only a partial reduction, proportional to the deductible component.

Exempt benefits. Some benefits fall entirely outside the FBT system and are not subject to FBT regardless of value:

Superannuation contributions (employer contributions are not fringe benefits)

Genuine salary and wages

Eligible electric vehicles (subject to conditions and current ATO rules)

Car expenses reimbursed using the ATO's cents-per-kilometre rate (subject to conditions)

Every exemption on this list is a compliance detail, not a loophole, and getting the conditions wrong is its own kind of exposure. If you are structuring benefits around these rules, it is worth having a registered tax agent confirm you actually qualify before you rely on them.

Want to know which of these exemptions your business could actually be using? The registered tax agents at What If Advice can walk through your current benefits and flag where you are leaving legitimate exemptions on the table. Call 1800 942 843 or email tax@whatifadvice.com.au.

FBT Record-Keeping Obligations

FBT record-keeping is not optional and is not something to organise after lodgement. The ATO requires employers to maintain records that substantiate the taxable value of benefits, the basis for any exemption or reduction claimed, and the FBT calculation itself.

Key record-keeping requirements by benefit type:

Car logbooks: must cover at least 12 consecutive weeks and must be current (renewed every 5 years or when business use changes materially). Without a valid logbook, the statutory formula method applies by default.

Car parking records: documentation of the commercial parking rate and the number of days the car park was available.

Expense payment records: receipts, invoices, and evidence confirming the work or private nature of the expense.

Employee declarations: for certain benefits, the employee must provide a signed written declaration confirming work use or another relevant fact. These declarations must be obtained before the FBT return is lodged. A declaration obtained after lodgement does not create an entitlement to the reduction retrospectively.

Records must generally be kept for 5 years. Missing records do not eliminate the FBT liability. They eliminate your ability to demonstrate that an exemption or reduction applies, which typically means the full taxable value is assessed.

FBT Returns and Registration

Do you need to register for FBT?

If you provide, or are likely to provide, fringe benefits to employees, you are required to register for FBT with the ATO. Registration does not mean you will always have a payable liability; it means the ATO knows you are in the system and you are obligated to lodge and pay when required.

You register through the ATO business portal or through your registered tax agent.

FBT returns:

An FBT return must be lodged for any FBT year in which you had a taxable liability. If you had no fringe benefits or all benefits were exempt, you are generally not required to lodge, but confirming this with your tax agent is worthwhile.

The return reports the total taxable value of benefits by category, the gross-up calculations, FBT payable, and any employee contributions reducing the liability.

Reportable fringe benefits on income statements:

Where an employee's total fringe benefits amount exceeds $2,000 in the FBT year, the grossed-up amount must be reported on their income statement. This figure is not counted as income for income tax purposes but is included in income tests for Medicare levy surcharge, HECS-HELP repayments, private health insurance rebates, and certain government payments. It is worth making employees aware of this when salary packaging arrangements are discussed.

Common FBT Mistakes Small Business Owners Make

Assuming a business purchase is automatically FBT-free. If an employee uses the asset privately, the private-use element can trigger FBT regardless of the original business purpose of the purchase.

Not registering for FBT when required. Many small businesses provide fringe benefits for years without registering. The ATO can assess back years and apply penalties and interest on unpaid amounts.

Using the statutory formula method for cars without checking the operating cost method. For vehicles with high business use supported by a valid logbook, the operating cost method often produces a significantly lower taxable value.

Providing gifts or entertainment just above the minor benefits threshold. A gift of $305 does not qualify for the minor benefits exemption. A gift of $295 does. The $10 difference in gift cost triggers an FBT liability that far exceeds the saving.

Running year-end staff functions without checking the per-head cost. A staff function at $350 per person does not satisfy the minor benefits exemption. Structuring the event at under $300 per head does, provided the other conditions are met.

Failing to obtain employee declarations before lodgement. Some reductions require a signed declaration from the employee. A declaration gathered after the return is lodged does not create a retroactive entitlement to the reduction.

Treating the FBT year the same as the income tax year. Confusing the two creates timing errors in records, calculations, and lodgement.

What if a small adjustment to how you structure employee benefits saves thousands in FBT each year? In many cases, the difference between a taxable benefit and an exempt one is a question of timing, value, or documentation. That is a worthwhile conversation to have before the FBT year ends.

Recognise your business in that list? The registered tax agents at What If Advice can check your current arrangements against these exact mistakes before your next return is due. Call 1800 942 843 or email tax@whatifadvice.com.au.

FAQ

What is the FBT rate in Australia?

The FBT rate is 47%, applied to the grossed-up taxable value of fringe benefits. The grossing-up process reflects the gross income an employee would have needed to earn, and pay income tax on, to fund the same benefit from after-tax wages. The result is that FBT can cost significantly more than the face value of the benefit itself.

Does FBT apply to sole traders?

FBT applies to benefits provided to employees. A sole trader with no employees does not have FBT obligations in relation to benefits they provide to themselves. If a sole trader employs others and provides them with benefits, FBT applies to those arrangements in the same way as any other employer.

Can an employee contribution reduce FBT?

Yes. Where an employee makes a payment to the employer in connection with a fringe benefit, the taxable value is reduced by the contribution amount before the gross-up calculation is applied. This is one of the most practical and commonly used methods of reducing FBT liability, particularly in salary packaging arrangements.

What is the minor benefits exemption threshold?

The exemption applies to benefits with a GST-inclusive value of less than $300 where it is also unreasonable to treat the benefit as a fringe benefit given its infrequent and irregular nature. The threshold is strictly less than $300. A benefit valued at exactly $300 does not qualify.

Are laptops and phones FBT-exempt?

Portable electronic devices provided primarily for use in the employee's employment are generally exempt from FBT under the work-related items exemption. The standard rule limits the exemption to one device per employee per FBT year for items with substantially identical function. Small business entities with aggregated annual turnover under $50 million can exempt multiple similar devices per employee per year. The device must be primarily for work use.

Does FBT apply to salary packaging?

Yes. Salary packaging arrangements, where an employee receives part of their remuneration as benefits rather than cash wages, create fringe benefits that are subject to FBT. The net benefit of a salary packaging arrangement depends on the difference between the FBT cost and the income tax saving, which varies by benefit type and the employee's marginal tax rate. Certain employers such as hospitals and public benevolent institutions have FBT concessions that make salary packaging particularly effective; standard small businesses do not have these concessions.

When is the FBT return due?

FBT returns are generally due by 21 May following the end of the FBT year (31 March). Businesses that lodge through a registered tax agent may have access to an extended due date. Late lodgement and late payment penalties can apply.

What records do I need for an FBT return?

Records vary by benefit type. Generally, you need receipts and invoices for expense reimbursements, car logbooks and odometer records for car benefits, written employee declarations where required, documentation confirming the work-related nature of exempt items, and records showing how any reduction or exemption was calculated. Records must generally be kept for 5 years.

Can I claim a tax deduction for FBT paid?

Yes. FBT paid is deductible for income tax purposes in the year of payment. The gross cost of providing the fringe benefit is also generally deductible. This is different from entertainment expenses claimed as a straight income tax deduction, where restrictions apply. The combined income tax deductibility partially offsets the FBT cost, though the net position is still significant at 47%.

How do I know if I need to register for FBT?

If you are an employer who provides or is likely to provide fringe benefits to employees, you should register for FBT. If you are unsure whether your current arrangements create fringe benefits, a registered tax agent can review the arrangements, advise on registration requirements, and identify any exposure before the ATO does.

What happens if I do not lodge an FBT return when I should have?

If you were required to lodge and did not, the ATO can identify the shortfall through data matching, employer reviews, or an audit, and can assess back years rather than just the current one. Penalties and interest apply on top of the FBT itself, and the longer an unregistered liability runs, the larger the eventual bill tends to be. If you are unsure whether past years should have been lodged, it is worth having a registered tax agent review your history before the ATO does it for you.

Do I need to worry about FBT if I am a sole trader who has just taken on my first employee?

Yes. The moment you employ someone, even one person, the same FBT rules apply to you as to a business with fifty staff. There is no size-based exemption. Common first-hire triggers include giving the new employee a work phone for personal use, reimbursing a personal expense, or providing a ute they can also drive on weekends. It is worth reviewing what you are actually providing before you assume none of it counts.

Ready to review your FBT position?

FBT is one of the most commonly misunderstood employer tax obligations in small business. Getting it wrong creates ATO exposure. Getting it right, with the right exemptions in place and records maintained, keeps your costs where they should be.

The registered tax agents at What If Advice work with business owners across Brisbane and Melbourne to identify FBT exposure, apply the correct exemptions, and ensure lodgement is accurate and on time.

Call 1800 942 843 or email tax@whatifadvice.com.au.

General Advice Disclaimer: This information is general in nature and does not take into account your personal financial situation, needs, or objectives. FBT rules are technical and subject to change. You should consider whether this information is appropriate for your circumstances and seek advice from a registered tax agent before making any decisions about your FBT obligations.

Still asking what if about your tax obligations? That is exactly the right question to be asking. A review of your current employee benefit arrangements could identify exemptions you are not using and exposure you do not know you have. The team at What If Advice can help you find out. AFSL 528250.