Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

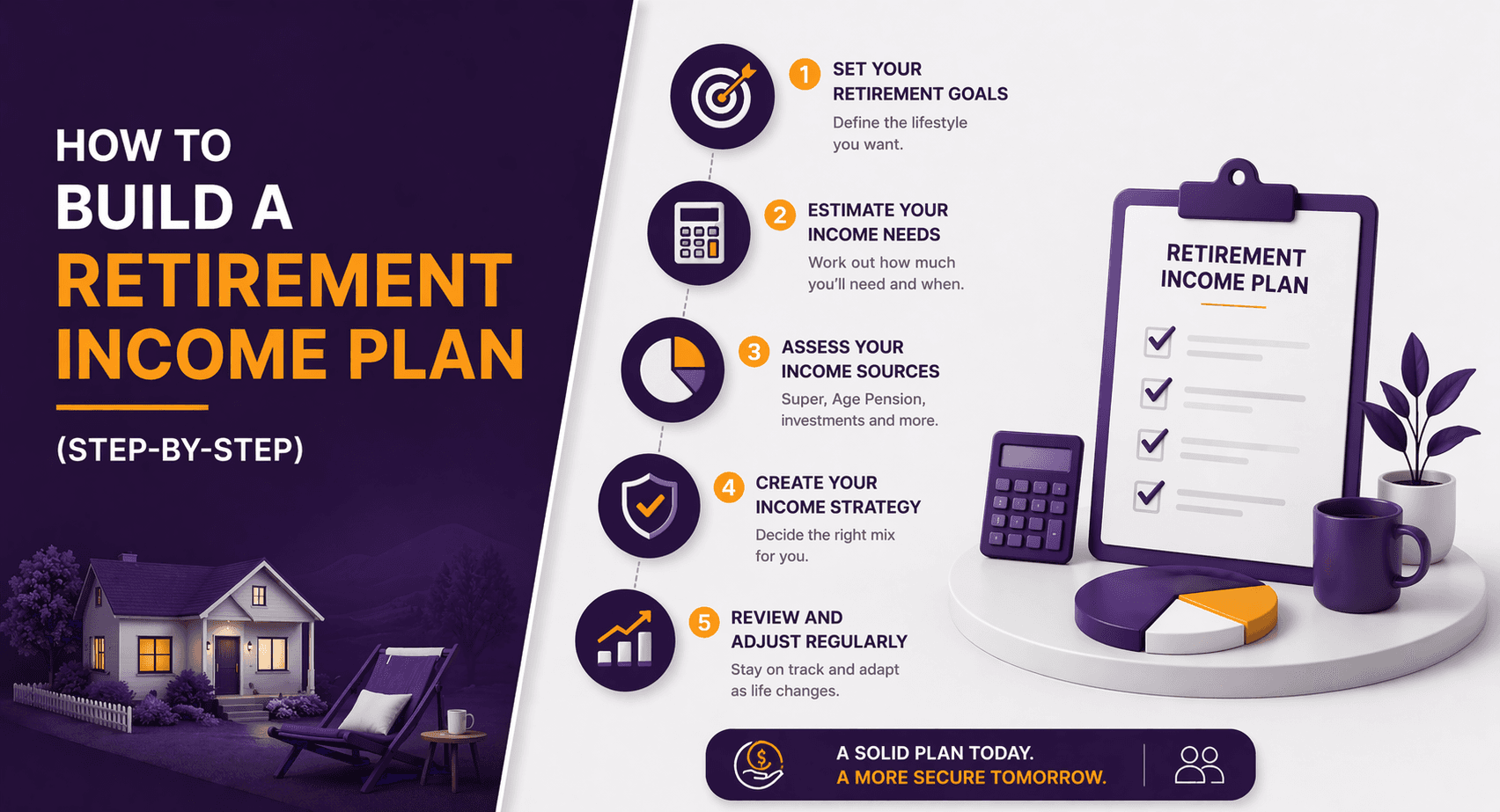

How to Build a Retirement Income Plan (Step-by-Step)

If you’re approaching retirement, the key question isn’t just “How much super do I have?” — it’s “How will I turn this into reliable income?”

A retirement income plan ensures your superannuation, investments and government benefits work together to provide sustainable income throughout retirement. Without a plan, retirees risk running out of money too early or being overly conservative and underspending.

Below is a step-by-step framework tailored for Australians.

Step 1: Define Your Retirement Income Target

Start with clarity.

Ask:

How much do I need each year?

What lifestyle do I want?

Will I travel? Downsize? Support family?

The Association of Superannuation Funds of Australia (ASFA) publishes retirement standards (subject to updates). As a general guide:

Lifestyle | Single (Annual) | Couple (Annual) |

Modest | ~$32,000 | ~$46,000 |

Comfortable | ~$51,000 | ~$72,000 |

Your personal target may differ depending on debt levels, housing, health and travel plans.

Action: Calculate your required annual spending in today’s dollars.

Step 2: Assess Your Income Sources

Most Australian retirees draw income from a mix of:

Superannuation (account-based pension)

Age Pension (if eligible)

Investment income (shares, property)

Cash savings

Part-time work

Superannuation

At retirement, your super can be converted into an account-based pension, allowing regular tax-effective withdrawals.

Earnings inside pension phase are generally tax-free (subject to current ATO rules).

Minimum annual drawdown rates apply.

Age Pension

Eligibility depends on:

Age (currently 67 for most Australians)

Income test

Assets test (subject to Services Australia rules)

Many Australians qualify for at least a part Age Pension, which can materially support retirement cash flow.

Action: Estimate your Age Pension eligibility using Services Australia guidelines.

Step 3: Structure Your Super for Income

Converting super to an account-based pension is common, but structure matters.

Key considerations:

Withdrawal rate (sustainable vs aggressive)

Investment allocation in retirement

Tax efficiency

Beneficiary nominations

A common starting point is a 4–5% annual withdrawal rate, but this depends on life expectancy, market returns and risk tolerance.

Example:

If you retire with $800,000 in super:

5% withdrawal = $40,000 per year

Combined with part Age Pension, total income may exceed $55,000–$65,000

This must be modelled carefully to reduce longevity risk.

Step 4: Build a Sustainable Withdrawal Strategy

Your retirement income plan should answer:

How long must the money last?

What happens in a market downturn?

How much income is flexible?

The “Bucket Strategy” (Common Australian Approach)

Many retirees use a 3-bucket strategy:

Cash Bucket (1–3 years of income)

Income Investments (bonds, conservative assets)

Growth Investments (shares for long-term growth)

This helps manage market volatility without panic selling.

Step 5: Manage Tax in Retirement

Retirement income can be tax-effective, but planning is essential.

Super pension income is generally tax-free after age 60 (subject to current ATO rules).

Investment income outside super may be taxable.

Capital gains tax may apply on non-super investments.

Pension phase transfer balance cap rules apply.

Strategic structuring can reduce lifetime tax paid.

Step 6: Plan for Inflation and Longevity

Australians are living longer. A 65-year-old today may live into their late 80s or 90s.

Inflation erodes purchasing power. Even 3% inflation halves purchasing power in roughly 24 years.

Your retirement income strategy must:

Maintain exposure to growth assets

Adjust income gradually

Be reviewed regularly

Step 7: Review and Adjust Annually

A retirement income plan is not “set and forget”.

Review annually to assess:

Portfolio performance

Withdrawal sustainability

Age Pension changes

Legislative updates (ATO / Services Australia rules)

Regular reviews reduce risk and improve outcomes.

Common Mistakes in Retirement Income Planning

Withdrawing too much too early

Holding too much cash long-term

Ignoring Age Pension eligibility

Failing to review beneficiary nominations

Not planning for aged care

A structured retirement income plan avoids these risks.

FAQs

1. What is a retirement income plan?

A retirement income plan outlines how your super, investments and government benefits will generate regular income throughout retirement.

2. How much super do I need to retire in Australia?

It depends on lifestyle goals. Many couples aim for $600,000–$1 million in super to support a comfortable lifestyle, but Age Pension eligibility significantly impacts this.

3. What is an account-based pension?

An account-based pension allows you to draw income from your super while keeping the remaining balance invested.

4. Can I receive the Age Pension and super income at the same time?

Yes, subject to income and asset tests set by Services Australia.

5. What is a safe withdrawal rate in retirement?

Often 4–5% annually is used as a starting guide, but this must be tailored.

6. Is retirement income taxed in Australia?

Super pension income is generally tax-free after age 60 (subject to current ATO rules). Other income may be taxable.

Build a Structured Retirement Income Plan With Confidence

Turning super into sustainable income requires careful modelling, tax awareness and understanding of Age Pension rules.

At What If Advice, we help Australians design tailored retirement income strategies aligned with current ATO and Services Australia rules. We model scenarios, test sustainability and provide clarity around long-term outcomes.

If you are within five to ten years of retirement — or already retired — professional planning can materially improve certainty and confidence.

Book a retirement strategy consultation with What If Advice today.

General Advice Disclaimer

This article provides general information only and does not take into account your personal objectives, financial situation or needs. Before making any financial decisions, you should consider whether the information is appropriate to your circumstances and seek personal advice from a licensed financial adviser. Rules relating to superannuation, taxation and Age Pension eligibility are subject to change under current ATO and Services Australia regulations.