Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

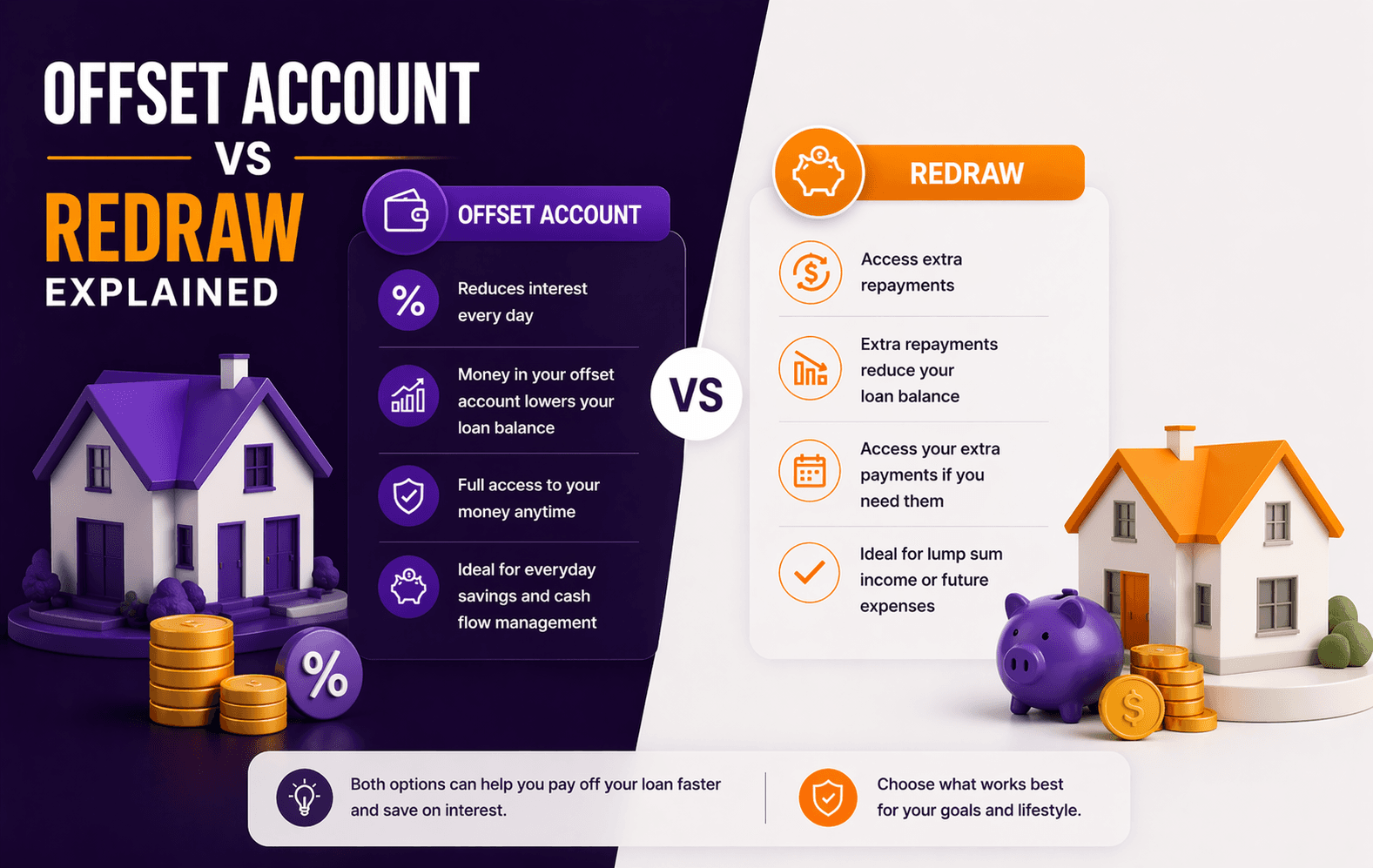

Offset Account vs Redraw: What’s the Difference?

Offset and redraw accounts both help reduce the interest you pay on your home loan.

The short answer:

Offset = more flexibility and control

Redraw = simpler, but with limitations

They may look similar, but the way they work can have very different outcomes, especially over time.

What Is an Offset Account?

An offset account is a transaction account linked to your home loan.

The balance in the account reduces the interest charged on your loan.

Example:

Loan: $600,000

Offset balance: $100,000

You’re only charged interest on:

$500,000

Key Features:

Works like a normal bank account

Full access to your money anytime

Reduces interest daily

What Is a Redraw Facility?

A redraw facility allows you to access extra repayments you’ve made on your loan.

Instead of sitting in a separate account, the money goes directly into your loan.

Example:

Loan: $600,000

You’ve paid an extra $50,000

Loan balance becomes:

$550,000

You may be able to “redraw” that $50,000 later.

Key Features:

Reduces your loan balance

Access to funds may be restricted

Usually no separate account

Offset vs Redraw: Side-by-Side Comparison

Feature | Offset Account | Redraw Facility |

Access to funds | Immediate | May be restricted |

Structure | Separate account | Built into loan |

Flexibility | High | Moderate |

Fees | Often higher | Usually lower |

Tax implications | Cleaner | Can be complex |

Bank control | Low | Higher |

Key Difference #1: Access and Control

With an offset account:

Your money is sitting in your account

You can withdraw it instantly

With redraw:

The money is technically paid into your loan

Access depends on lender policies

Some lenders:

Limit redraw amounts

Restrict frequency

May freeze access in certain situations

Key Difference #2: Tax Implications (Important for Investors)

This is where things quietly get serious.

Offset Account:

Your loan balance doesn’t change

Funds are clearly separate

Simpler from a tax perspective

Redraw Facility:

You reduce your loan balance

If you redraw for personal use, it can:

Affect tax deductibility

Create mixed-purpose loans

Subject to current ATO rules, this can complicate things significantly for investment properties.

Key Difference #3: Interest Savings

Both reduce interest, but in different ways:

Offset reduces the amount interest is calculated on

Redraw reduces the loan balance itself

In most cases, the interest outcome is similar if used consistently.

When an Offset Account May Be Better

You want full flexibility

You’re planning future investments

You want clean loan structuring

You value immediate access to funds

When Redraw May Be Suitable

You want a simpler setup

You’re focused on paying down your loan

You don’t need frequent access to funds

You want to avoid higher account fees

The Hidden Risk with Redraw

Many people treat redraw like a savings account.

It’s not.

Lenders can:

Change redraw terms

Limit access

In rare cases, restrict withdrawals

Your money is sitting inside the loan, not in your control in the same way as an offset account.

Real-Life Scenario

Chris (Owner-occupier):

Uses redraw:

Makes extra repayments

Occasionally redraws for emergencies

Works well because:

No complex tax implications

Focus is on reducing debt

Sarah (Investor):

Uses offset:

Keeps savings separate

Plans to use funds for future investments

Outcome:

Maintains tax clarity

Preserves flexibility

Cost Consideration

Offset accounts often come with:

Package fees

Higher loan costs

Redraw facilities:

Usually included

Lower cost overall

So the decision isn’t just functional, it’s also financial.

Key Question: Which Is Better?

There’s no universal winner.

Offset = flexibility + cleaner structure

Redraw = simplicity + lower cost

The right choice depends on:

Your financial goals

Whether the loan is for personal or investment use

How you plan to use the funds

Choosing based only on “what saves interest” misses the bigger picture.

FAQs

1. Does an offset account reduce repayments?

Not directly. It reduces interest, which may shorten your loan term or reduce interest paid.

2. Is redraw the same as an offset?

No. Redraw is part of your loan, while offset is a separate account.

3. Can banks restrict redraw access?

Yes, depending on lender policies and conditions.

4. Which saves more interest?

Both can save similar amounts if used effectively.

5. Is an offset account worth the fees?

Often yes, if you maintain a meaningful balance.

6. Can I have both offset and redraw?

Yes, many loans offer both features.

7. Is redraw bad for investment properties?

It can create tax complications if not structured properly (subject to ATO rules).

Not Sure Which Loan Features You Should Use?

Offset and redraw accounts can both reduce interest, but the way they’re structured can have long-term implications, especially if you’re investing or planning to access funds later.

Choosing the right setup can help:

Improve flexibility

Maintain tax efficiency

Support future financial decisions

A structured review of your loan can help ensure your features are working for you, not against you.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional financial advice. Information is subject to current ATO and Services Australia rules and may change over time.