Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

Industry super funds are genuinely good for most Australians, most of the time. Low fees, strong long-term returns, and a not-for-profit structure make them a solid default. If your super is the only thing you need to think about, there may not be a problem at all.

But here is the part worth sitting with: a fund manages your money. A financial adviser manages your life around your money. Those are two very different things, and the gap between them tends to grow the older you get, the more complicated your situation becomes, and the closer you are to actually needing your super to support you.

This post explains what industry super funds do well, where they stop, and when personalised financial advice starts to matter enough to act on.

Jump to a Section

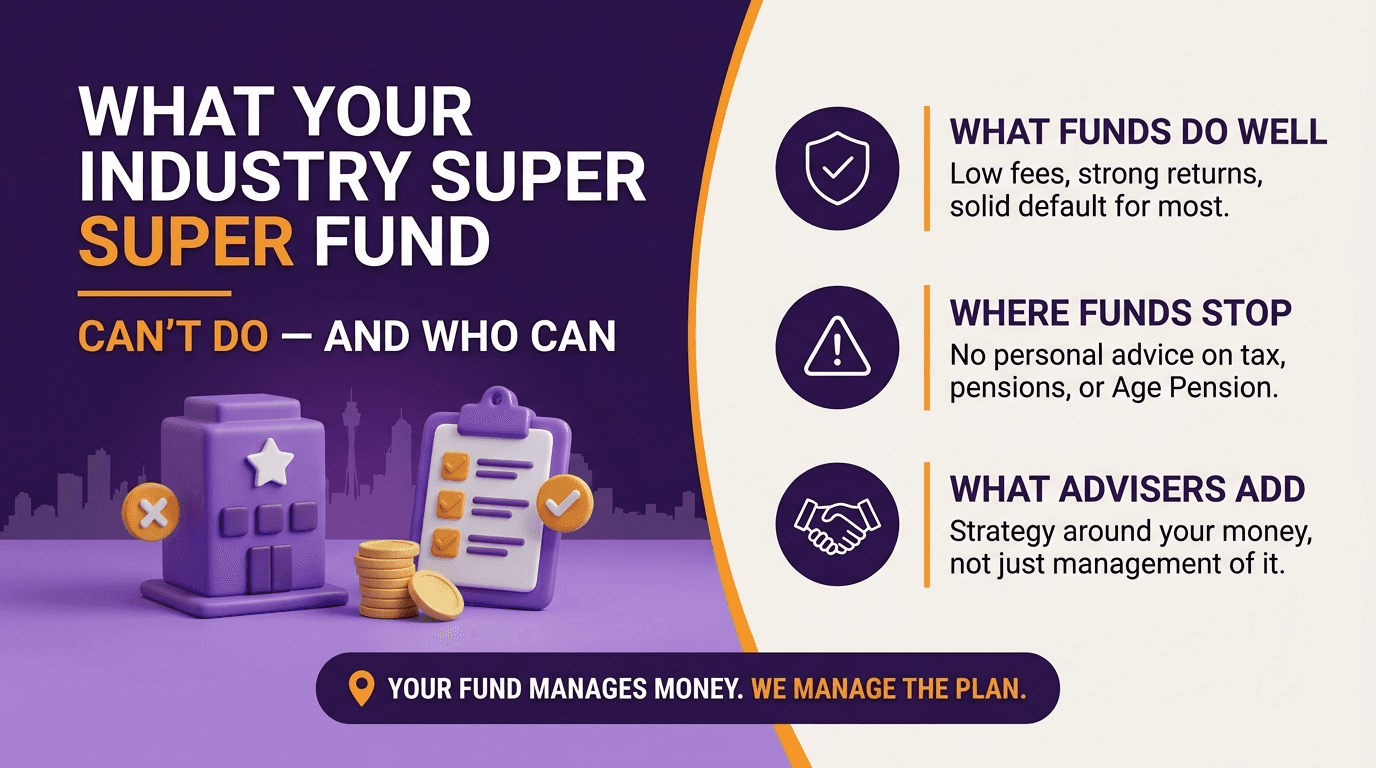

What Industry Super Funds Do Well (And Why That Is Not Always Enough)

What Your Super Fund Cannot Do: The Advice Gap Explained

When Personalised Financial Advice Starts to Matter More Than Your Fund

Is Financial Advice Worth the Cost? The Honest Answer

Seven Common Mistakes Australians Make by Relying Solely on a Default Fund

Meet Sarah and Tom

Frequently Asked Questions

When to See a Financial Adviser: A Practical Checklist

What Industry Super Funds Do Well (And Why That Is Not Always Enough)

Let's be direct: the case for industry funds is real.

The not-for-profit structure means returns flow back to members rather than shareholders. The largest funds have delivered consistent long-term performance, with leading options posting around 8.7 to 8.9 per cent returns over ten years in their balanced options. Fees at the major funds run around $370 to $385 per year on a $50,000 balance, which is well below the retail fund average.

Industry super funds account for roughly 36 per cent of all Australian super assets and hold around 57 per cent of all super accounts nationally. That scale gives them access to assets, infrastructure, and investment options that smaller funds simply cannot match.

In 2025, all 52 MySuper products passed APRA's annual performance test, which means the floor for industry fund quality has never been higher. Regulatory scrutiny has improved transparency, and most Australians in a major industry fund are being looked after reasonably well.

So what is the problem?

There is not one, if your super is the only thing you need to think about. The problem emerges when your financial life gets more complicated than any fund is equipped to handle.

What Your Super Fund Cannot Do: The Advice Gap Explained

An industry super fund can manage investments on your behalf. It can provide general information and limited intra-fund guidance. What it cannot do is give you personal financial advice.

It cannot tell you whether you should be salary sacrificing more given your specific tax bracket. It cannot model what your retirement looks like if you retire at 60 instead of 67, taking into account your mortgage payoff date, your partner's income, and your eligibility for the Age Pension. It cannot assess whether your default insurance cover inside super is appropriate for someone in your profession with two dependants and an income protection policy already in place.

According to KPMG's 2026 Super Insights report, funds are under increasing pressure to provide timely, accessible guidance that supports better member decision-making, particularly at key moments across the super journey. The reason that pressure exists is because there is a structural gap between what funds offer and what members actually need as they approach retirement.

Well-intentioned intra-fund advice models fail those with even moderate complexity. And moderate complexity is not unusual. It covers dual-income couples, business owners, people with investment properties, people approaching the Age Pension assets threshold, and anyone whose retirement timeline has changed.

When Personalised Financial Advice Starts to Matter More Than Your Fund

Pre-retirees who need to optimise the last five to ten years

The decade before retirement is the most financially consequential period in most Australians' working lives. A significant market downturn just before or just after retirement can do more long-term damage than a downturn at 35, because there is far less time to recover. This is sequencing risk, and managing it through appropriate investment positioning is one of the clearest examples of where personalised advice adds measurable value.

Deciding how to position your portfolio during this period, when to shift from accumulation to pension phase, and how to structure drawdown to maximise Age Pension eligibility are decisions that compound heavily. A fund can tell you what options are available. A financial adviser can model the specific impact on your specific balance.

The ASFA Retirement Standard sets comfortable retirement targets at $630,000 for a single homeowner and $730,000 for a couple (as at 2026). Figures are updated regularly, so check the ASFA website for the most current benchmarks. The median super balance for Australians aged 60 to 64 sits at approximately $250,000. That gap between where most people are and where they need to be is not going to close itself, and for many Australians, the strategies available in the final working years are the most powerful tools they have left.

Catch-up concessional contributions, transition to retirement strategies, account-based pension structures, and careful timing around the assets test all require a personalised approach. None of them can be properly modelled through a general information call to your fund's helpline.

Business owners and self-employed Australians

If you run a business, your super situation is almost certainly more complex than the industry fund default is designed to address.

Contribution patterns are irregular. Structuring decisions about how to extract income from your business, and what form that income takes, have direct implications for your concessional contributions strategy. The interaction between your business structure, your personal tax position, and your super can deliver materially different outcomes depending on how it is managed.

This is precisely the territory where working with an adviser who understands both the accounting and the financial planning side of your situation starts to pay for itself. Having both disciplines in the same room, looking at the same picture, changes the quality of the decisions available to you.

Dual-income professional couples

For couples with two incomes, two super balances, and potentially different retirement timelines, a coordinated strategy can significantly outperform two individuals each managing their own fund independently.

Decisions about contribution splitting, who maximises salary sacrifice in which year, and how to structure assets ahead of the Age Pension means test require someone to look at the household picture rather than two separate member accounts.

Anyone approaching the Age Pension assets threshold

The Age Pension assets test free area sits at approximately $301,750 for a single homeowner and $451,500 for a couple. Above those thresholds, the pension reduces by $3 per fortnight for every $1,000 in assets.

For many Australians, relatively small decisions about how assets are held, when contributions are made, and how retirement income is drawn can have a meaningful impact on Age Pension entitlement. These are not theoretical optimisations. They are real differences in household income across a retirement that may last twenty to thirty years.

Not sure which of these scenarios sounds like you?

The What If Advice team works with pre-retirees, business owners, and dual-income couples across Brisbane and Melbourne. A conversation costs nothing. Email clientservices@whatifadvice.com.au or book a spot at our next Retire Ready Roundtable at whatifadvice.com.au/workshops.

What the Comparison Actually Looks Like

Industry Super Fund | Personalised Financial Advice | |

Low fees on investments | Yes | Fund-dependent |

Strong long-term returns | Generally yes | Depends on strategy |

Investment choice | Limited to fund options | Broader, structured to your goals |

Tax strategy and salary sacrifice advice | General information only | Personalised |

Retirement income modelling | Generic calculators | Specific to your situation |

Age Pension optimisation | Not available | Core service |

Business or self-employment structuring | Not available | Core service |

Insurance review | Limited | Full assessment |

Estate planning coordination | Not available | Available |

Entry point | Low cost, default | Single-issue or comprehensive advice |

The comparison is not fund versus adviser. For most Australians, it should be fund plus adviser, where the fund holds and grows the money, and the adviser builds the strategy around it.

Is Financial Advice Worth the Cost? The Honest Answer

The most common reason Australians do not seek financial advice is cost. That is a legitimate concern, and it deserves a straight answer.

Financial advice involves upfront fees, and for some people at some points in their lives, a comprehensive ongoing advice relationship may not be the right fit. Single-issue advice, which covers one specific question or decision, can be a useful and more accessible starting point for anyone who is not ready to commit to a full planning relationship.

The real question is what the alternative costs. A difference of 0.75 per cent in fees across a career can translate to $92,700 less at retirement on an average income, based on a starting income of $83,200 and average returns of 6.4 per cent per year. The impact of a poor transition-to-retirement decision, an unreviewed insurance policy, or a missed contribution strategy over five years tends to be considerably larger than the cost of advice.

The honest framing is that financial advice is not cheap. But unadvised decisions in the wrong decade are not free either.

Seven Common Mistakes Australians Make by Relying Solely on a Default Fund

Most Australians who rely solely on a default fund make at least one of the following mistakes, often without realising the cost.

Staying in the default MySuper investment option long after it suits their risk profile. Most defaults shift toward conservative as members age, regardless of individual circumstances.

Carrying default insurance cover that does not match their actual situation. Default cover is often insufficient for high earners and redundant for those with existing personal policies.

Missing catch-up contribution opportunities. Members with balances under $500,000 who have not maximised contributions in prior years may have significant unused cap space they are not using.

Not reviewing fund and investment option when transitioning to pension phase. The best accumulation product is not always the best pension product, and the wrong structure at this stage can be costly.

Ignoring the interaction between super drawdown and Age Pension eligibility. The order in which assets are drawn down, and how assets are structured at retirement, can meaningfully affect entitlement.

Running two balances independently in a couple without coordinating strategy. Significant opportunities for contribution splitting, tax management, and assets test positioning are routinely missed.

Treating super as a set-and-forget account until age sixty-five. The compounding impact of strategic decisions in the final ten years of work is disproportionate to the time involved.

Meet Sarah and Tom

Sarah is 52, works in marketing, and has $310,000 in her industry super fund. She has been in the same fund since her first job and has never changed her investment option. She makes no additional contributions beyond the Superannuation Guarantee, has not reviewed her insurance, and does not know whether she is on track for a comfortable retirement.

By the ASFA benchmark for her age, she is roughly in range. But only just, and the next fifteen years will determine everything. What Sarah does not yet know is that her income history likely gives her access to unused concessional contribution cap space through the carry-forward rules, and that a review of her investment option in her early 50s, while she still has time on her side, could materially shift her trajectory heading into retirement.

Tom is 58, self-employed as a trades contractor, and has $420,000 across two super accounts he has never consolidated. He has an unpredictable income, makes ad hoc contributions when cash allows, and has no retirement income plan. He wants to retire at 63.

He does not know what the Age Pension means test would look like for him, whether his business sale proceeds could be contributed to super, or how much he would need to draw down each year to avoid running out. What Tom's situation actually calls for is a financial planner and an accountant working from the same plan, because the small business CGT concessions, the timing of his business sale, and the structure of his retirement income are decisions that interact with each other. Getting one right while getting another wrong is a costly way to exit a business.

Both Sarah and Tom are in industry funds delivering reasonable returns. Neither of them has a financial plan. The fund is doing its job. The job the fund cannot do is the part that will determine what their retirements actually look like.

Frequently Asked Questions

How do I know if my super fund is performing well?

For many Australians, the answer is yes. The top-performing industry funds have delivered strong long-term returns and keep fees competitive. The more important question is not just whether returns are good, but whether your investment option, contribution level, and retirement strategy actually match your circumstances.

Do I need a financial adviser if I already have a good super fund?

A good fund manages your investments. A financial adviser manages the strategy around those investments, including tax, contributions, insurance, pension structuring, and Age Pension eligibility. These are complementary services, not alternatives.

How much does personal financial advice actually cost?

Advice fees vary significantly depending on the scope of work and the adviser. Initial consultations and single-issue advice tend to be more accessible than ongoing comprehensive planning. Many Australians find that the cost of advice, measured against the value of a well-structured decade before retirement, makes sense to pursue.

Can my super fund give me financial advice?

Your fund can provide general information and limited intra-fund guidance. It cannot give you personal advice that takes into account your specific financial situation, goals, tax position, or family circumstances. For personal advice, you need a licensed financial adviser.

What is sequencing risk in superannuation?

Sequencing risk is the danger that poor investment returns occur at the wrong time, specifically in the years just before or just after retirement. A downturn that hits at 60 does significantly more damage than one at 35, because there is far less time to recover. Managing this risk through appropriate investment positioning is one of the clearest examples of where personalised advice adds value.

Do I need to switch super funds to get financial advice?

No. Many financial advisers work with clients who remain in their existing industry fund. A change of fund is a separate decision from seeking advice, and one does not require the other. An adviser will assess whether your current fund is appropriate as part of a broader review.

What happens to my super insurance if I switch funds?

Switching funds can affect your default insurance cover, sometimes significantly. It is important to review your insurance situation, including any cover held personally outside super, before making any changes. This is one reason an adviser-led review is useful before switching.

When to See a Financial Adviser: A Practical Checklist

If any of the following applies to you, a conversation with a financial adviser is worth having sooner rather than later.

You are within fifteen years of your intended retirement age.

You are self-employed or run a business.

You have two incomes and two super balances in a household with no coordinated strategy.

You have not reviewed your insurance inside super in more than three years.

You are unsure whether you are on track for the retirement you have in mind.

You have experienced a significant financial event, such as an inheritance, property sale, or income change.

The What If Advice team includes financial advisers across Brisbane and Melbourne who work with clients at every stage, from early planning through to retirement income strategy and Age Pension optimisation.

If you would like to understand where you stand, a conversation costs nothing. Email us at clientservices@whatifadvice.com.au or join us at our next Retire Ready Roundtable workshop at whatifadvice.com.au/workshops.

This article contains general information only and does not constitute personal financial advice. Your personal objectives, financial situation, and needs have not been taken into account. Before making any financial decision, consider whether this information is appropriate for your circumstances and seek advice from a qualified financial adviser. What If Advice operates under Beryllium Advisers Pty Ltd, AFSL 528250.