Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

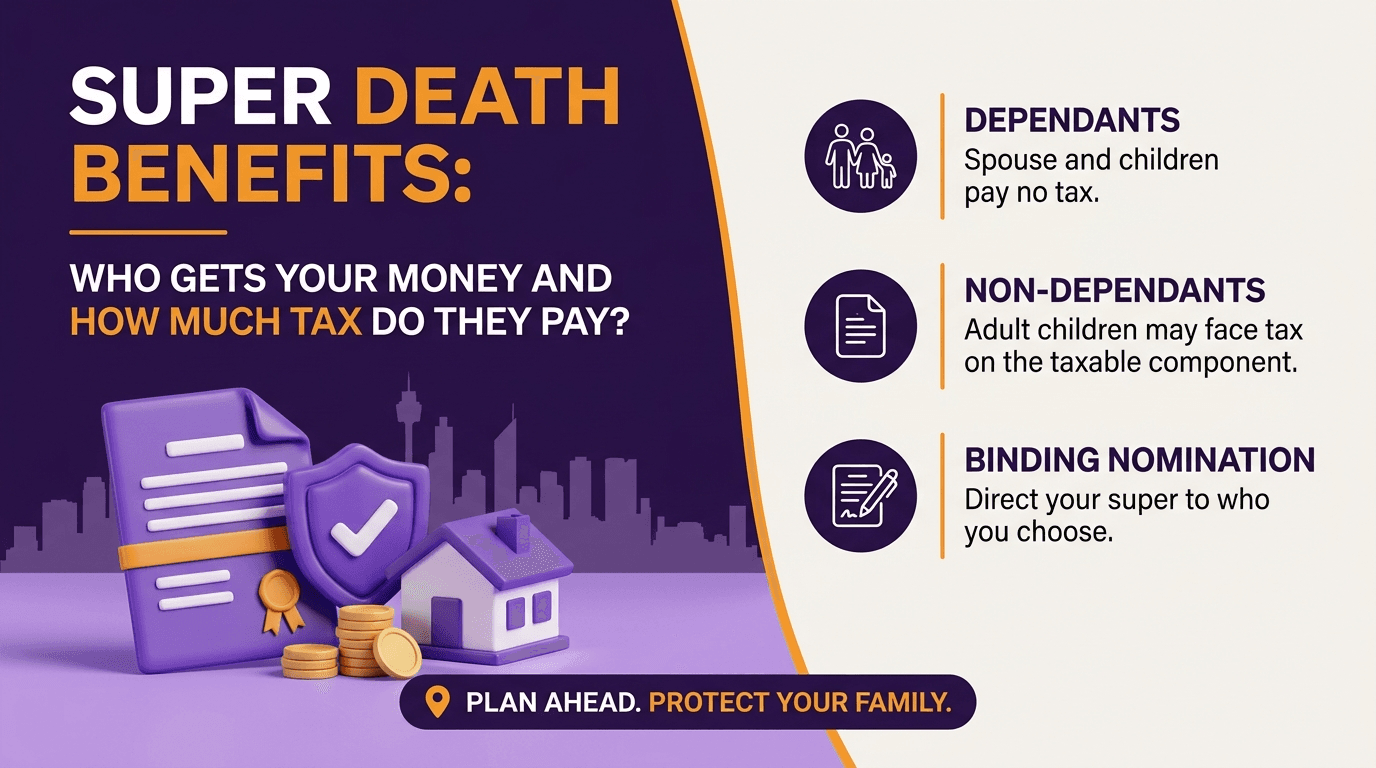

Super Death Benefits: Who Gets Your Money and How Much Tax Do They Pay?

For many Australians, super is now one of the largest assets they own, often second only to the family home. Yet most members have only a vague idea of what happens to their super when they die.

The rules are not intuitive. Super does not automatically pass through your will. Different beneficiaries pay vastly different amounts of tax. And without proper documentation, your super can end up with someone you never intended.

This guide explains who can receive your super after death, how much tax they pay, and how to structure your nominations to align with your wishes.

Quick Answer

Here is what every Australian should know about super death benefits:

Super does not automatically pass through your will

Only dependants can receive super tax-free; non-dependants pay tax of up to 17% (15% plus Medicare) on the taxable component

A binding death benefit nomination (BDBN) legally compels the trustee to pay according to your wishes

A reversionary pension automatically continues to a nominated beneficiary, often the most tax-effective option

Adult children are typically classified as non-dependants and pay tax on most of the super they inherit

Bottom line: Super death benefits are governed by their own rules, separate from your will. Without proactive structuring, your beneficiaries may pay more tax than necessary or receive funds you did not intend for them.

How Super Is Distributed After Death

When a super member dies, the trustee of their fund determines who receives the death benefit. This can happen in several ways:

Binding death benefit nomination (BDBN). A legally binding instruction to the trustee, valid for typically 3 years (lapsing) or indefinitely (non-lapsing) depending on the fund.

Reversionary pension. An automatic continuation of an existing pension to a nominated beneficiary, usually a spouse.

Non-binding nomination. A guideline only, the trustee retains discretion.

No nomination. The trustee uses its discretion based on dependants and the deceased's estate.

Trustee discretion means decisions can take months to finalise and may not match the deceased's expectations. Family disputes are common where nominations are ambiguous or absent.

Bottom line: Super distribution is too important to leave to discretion. Active structuring is essential.

Who Can Receive a Super Death Benefit?

Super law restricts who can receive a death benefit directly. Eligible recipients include:

Spouse (married, de facto, or same-sex)

Children of any age, including adult children

Financial dependants (someone financially supported by the deceased)

Interdependants (someone in a close personal relationship sharing finances and domicile)

The estate (legal personal representative, distributing per the will)

Notably, the following cannot receive super directly:

Friends

Charities

Siblings, parents, or extended family (unless they qualify as financial dependants)

If you wish to leave super to anyone other than the eligible recipients above, it must flow through your estate via your will.

Bottom line: Super has its own list of eligible recipients. Anyone outside that list can only receive super through the estate.

Tax Treatment: Dependants vs Non-Dependants

The single most important distinction in super death benefits is the difference between a dependant and a non-dependant for tax purposes. The two definitions are not the same.

Recipient | Tax Status | Tax on Taxable Component | Tax on Tax-Free Component |

Spouse | Dependant | Tax-free | Tax-free |

Child under 18 | Dependant | Tax-free | Tax-free |

Child 18+ (financially independent) | Non-dependant | Up to 17% | Tax-free |

Child 18+ (financial dependant) | Dependant | Tax-free | Tax-free |

Financial dependant | Dependant | Tax-free | Tax-free |

Interdependant | Dependant | Tax-free | Tax-free |

Estate (eventually to non-dependant) | Non-dependant treatment | Up to 15% (no Medicare) | Tax-free |

The taxable component is the portion of super derived from concessional contributions (employer SG, salary sacrifice, personal deductible) and earnings on those amounts. The tax-free component derives from non-concessional contributions.

For most Australians, the taxable component is the larger portion. Adult children inheriting super typically pay 15% plus Medicare levy on this component.

Bottom line: Spouses and financial dependants receive super tax-free. Adult children typically pay tax of around 17% on the bulk of inherited super.

Binding Death Benefit Nominations Explained

A binding death benefit nomination (BDBN) is a legally enforceable instruction to your super fund's trustee about who should receive your death benefit and in what proportions.

Key features:

Must name only eligible recipients (spouse, children, financial dependants, interdependants, or estate)

Must specify proportions adding to 100%

Most BDBNs lapse after 3 years unless renewed; some funds offer non-lapsing nominations

Must be signed and witnessed correctly to be valid

Override the trustee's discretion entirely

Common BDBN errors include:

Allowing the nomination to lapse

Naming an ineligible recipient (the nomination becomes invalid)

Failing to update after major life events (marriage, divorce, new children)

Improper witnessing

A lapsed or invalid BDBN reverts to trustee discretion, defeating the entire purpose.

Bottom line: BDBNs require active management. Review every 3 years and after every major life event.

Reversionary Pensions: The Often-Best Option

For couples, a reversionary pension is frequently the most tax-effective and seamless way to pass super between spouses on death.

How it works:

The deceased's account-based pension automatically continues to the nominated reversionary beneficiary (typically the spouse)

No commutation occurs at the date of death

The pension continues uninterrupted with the spouse as the new owner

Tax-free for spouses and other dependants

Reversionary pensions also have important interactions with the transfer balance cap (TBC). The deceased's pension counts toward the survivor's TBC after a 12-month grace period, which provides time for planning.

For SMSF members, reversionary pensions also avoid the need for the trustee to make a discretionary decision and reduce the risk of estate disputes.

Bottom line: For couples with account-based pensions, reversionary nominations are often the simplest and most tax-effective structure.

Practical Examples

Example 1: John, 70, with Adult Children

John has $720,000 in super (split 90% taxable component, 10% tax-free) and three adult children. His wife Susan predeceased him five years ago. He has no current spouse and no financial dependants.

Without planning, his super on death would be paid to his children. The tax outcome:

$720,000 total super

90% taxable component = $648,000

Tax at 17% (15% plus Medicare) = approximately $110,000

Net to children: approximately $610,000

With planning, John implements a recontribution strategy during his lifetime, withdrawing super tax-free (he is over 60) and recontributing as non-concessional contributions, gradually shifting more of the balance into the tax-free component.

After three years of this strategy, his super is now 50% tax-free / 50% taxable. The tax on death drops to approximately $55,000, saving his children $55,000 in tax.

Example 2: Sarah and Mark, Both 67, Setting Up Reversionary Pensions

Sarah and Mark each have account-based pensions of $450,000. They want to ensure that if either dies, the other receives the super seamlessly and tax-effectively.

Their structure:

Both nominate each other as reversionary beneficiaries on their pensions

Both also implement binding death benefit nominations as a backup, naming each other as primary and their adult son as secondary

They review nominations every 2 years and after any major life event

When Mark dies five years later, his pension automatically continues to Sarah as a reversionary pension. There is no tax payable, no need for a trustee decision, and Sarah's income continues uninterrupted. The pension counts toward her transfer balance cap after the 12-month grace period.

Common Mistakes Australians Make

Assuming super passes through your will. It does not, unless your nomination directs it to your estate. Without a binding nomination, the trustee decides.

Letting binding nominations lapse. Most BDBNs expire after 3 years. Many Australians make a nomination once and never review it, leaving expired nominations in place when they die.

Naming ineligible recipients. Friends, siblings, parents (unless dependants), and charities cannot receive super directly. Nominations to them become invalid.

Not implementing a recontribution strategy. For Australians over 60 with significant taxable components and adult children as ultimate beneficiaries, recontribution can save heirs tens of thousands in tax.

Forgetting reversionary pensions. Couples with account-based pensions almost always benefit from reversionary nominations. Many do not realise the option exists.

Failing to update after life events. Marriage, divorce, new children, deaths in the family, and remarriage all change the optimal nomination structure. Most people never update.

Treating super as a simple bank account. Super has its own rules, its own tax treatment, and its own beneficiary system. It must be planned alongside the will, not as part of it.

FAQ

Who can I leave my super to? Eligible recipients include your spouse (married, de facto, or same-sex), children of any age, financial dependants, interdependants, and your estate. Anyone outside this list can only receive super through your estate.

Why do my adult children pay tax on my super? Adult financially independent children are treated as non-dependants for super death benefit tax purposes. They pay up to 17% (15% plus Medicare levy) on the taxable component of any super they inherit. The tax-free component is not taxed.

Is a will enough to direct my super? No. Super does not automatically pass through your will. To direct super to your estate (and then via your will), you must make a binding death benefit nomination naming the estate as the beneficiary.

What is the difference between binding and non-binding nominations? A binding nomination legally compels the trustee to pay according to your wishes. A non-binding nomination is a guideline only; the trustee retains discretion.

How long does a binding death benefit nomination last? Most binding nominations lapse after 3 years unless renewed. Some funds offer non-lapsing nominations that remain valid until changed or revoked.

What is a recontribution strategy? A recontribution strategy involves withdrawing super (tax-free from age 60) and recontributing it as non-concessional contributions, gradually increasing the tax-free component of your balance. This reduces the tax payable by non-dependant beneficiaries on death.

Can my de facto partner receive my super tax-free? Yes, provided the relationship meets the legal definition of a de facto relationship (typically including living together on a genuine domestic basis). Documentation matters, as super funds may require evidence of the relationship.

Ready to Get Your Super Estate Planning Right?

Super death benefits affect every Australian with a super balance, regardless of age. Book a free 15-minute consultation with the team at What If Advice to discuss your nomination strategy and ensure your super passes to the people you intend, with minimal tax.

Visit whatifadvice.com.au to book.

General Advice Disclaimer: This information is general in nature and does not take into account your personal financial situation, needs, or objectives. You should consider whether it is appropriate for you and seek personal financial advice before making any decisions.