Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

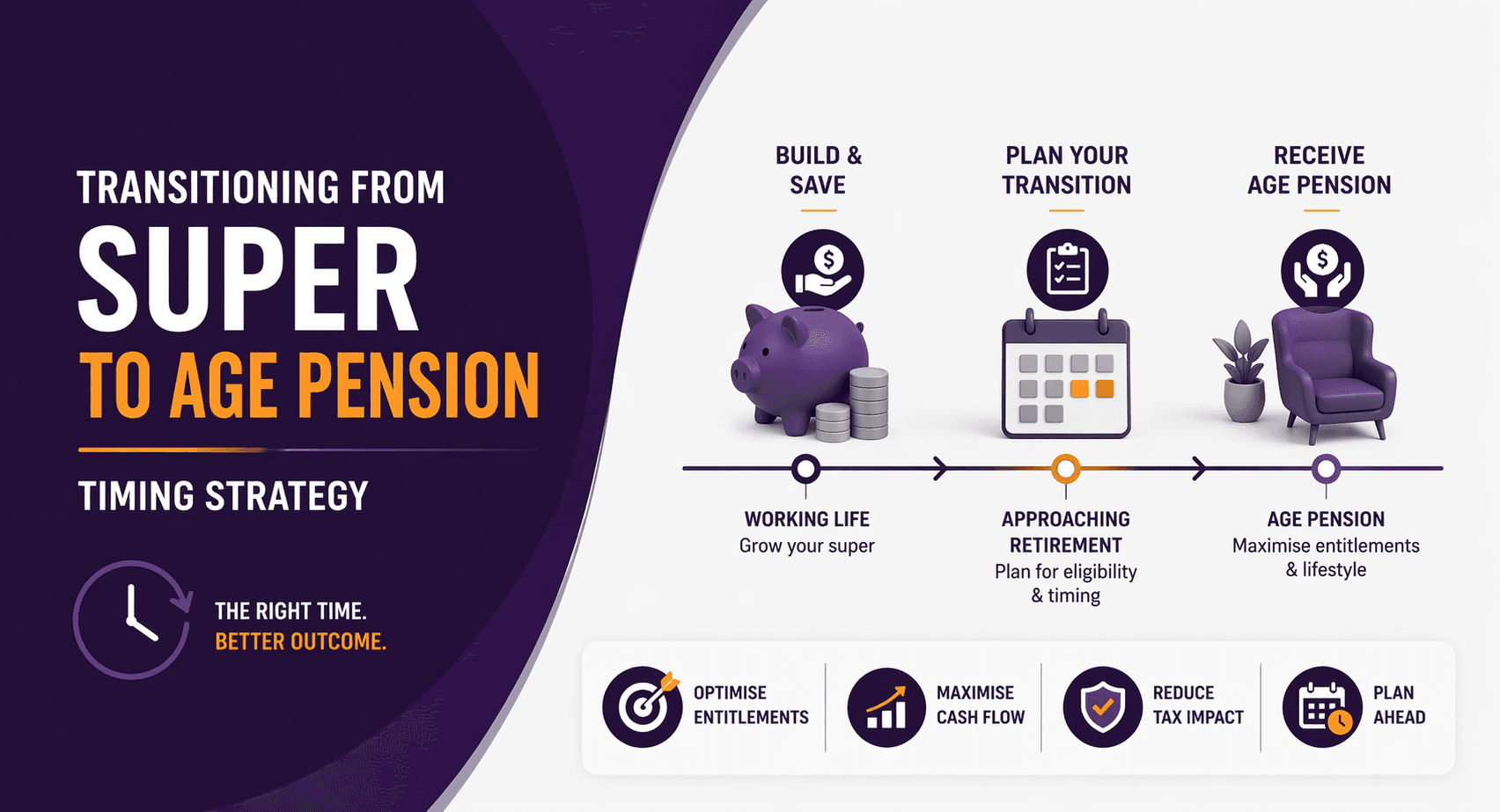

Transitioning from Super to Age Pension: Timing Strategy for Australians

The transition from superannuation to the Age Pension is one of the most important financial decisions in retirement.

Get the timing right, and you can maximise your income and preserve your wealth. Get it wrong, and you could miss out on entitlements or draw down your super faster than necessary.

Here’s how the transition actually works and how to approach it strategically.

When Does the Age Pension Start?

You can apply for the Age Pension when you reach Age Pension age, which is currently:

67 years old (subject to current Services Australia rules)

But eligibility isn’t automatic.

You must pass:

The assets test

The income test

Residency requirements

What Happens Before Age Pension Age?

Before 67:

Your super is your primary income source

You may be drawing from:

Account-based pensions

Transition to Retirement (TTR) strategies

Important:

Super in accumulation phase is generally not counted under the assets test before Age Pension age

Once you reach pension age, it becomes assessable

This is where timing starts to matter.

The Key Transition Point: Turning 67

At Age Pension age:

Your super is assessed under Centrelink rules

Your eligibility is recalculated

This creates three possible outcomes:

1. Full Age Pension

If your assets and income are below thresholds.

2. Part Age Pension

Most common scenario.

You combine:

Super withdrawals

Partial government support

3. No Pension

If your assets/income exceed limits.

Timing Strategy: When Should You Apply?

Option 1: Apply Immediately at 67

Best if:

You’re already below thresholds

You want to access benefits early

You need additional income

Pros:

Immediate cash flow

Access to concession cards

Cons:

May not be optimal if assets are still high

Option 2: Delay Application Strategically

Sometimes waiting is smarter.

Example:

You retire at 67 with $600,000 in super

Above threshold = no pension

Over 2–3 years, you draw down = balance drops

You become eligible later

This can result in:

Higher pension entitlement when you do apply

Option 3: Stage Your Drawdown

Instead of random withdrawals:

Plan how much super you draw each year

Goal:

Gradually reduce assets to:

Qualify for part pension

Eventually reach optimal balance

This is where actual strategy lives.

Super Drawdown vs Age Pension: Finding the Balance

You’re balancing two forces:

Strategy | Outcome |

High super balance | Lower pension |

Lower super balance | Higher pension |

Balanced approach | Optimised total income |

The objective is not:

👉 “Get the biggest pension”

It’s:

👉 “Maximise total retirement income”

Example Scenario

Stage | Super Balance | Pension | Total Income |

Age 67 | $650,000 | $0 | $40,000 (super only) |

Age 70 | $500,000 | $300/fortnight | Higher combined |

Age 75 | $350,000 | Near full pension | Stable income |

Same person. Different outcomes based on timing and drawdown.

Key Factors That Affect Your Transition

1. Asset Structure

Not all assets are treated equally.

Super = assessable after pension age

Home = generally exempt

Financial assets = deemed income

2. Income Test (Deeming Rules)

Centrelink assumes your assets generate income:

Even if they don’t

This impacts:

Your pension entitlement

Your optimal withdrawal strategy

3. Life Expectancy & Spending Needs

You need to balance:

Sustainability

Lifestyle

Government support

Too conservative = miss lifestyle

Too aggressive = run out of funds

Common Mistakes to Avoid

1. Applying too early without strategy

You might qualify later for more.

2. Drawing super randomly

No structure = inefficient outcomes.

3. Ignoring deeming rates

These affect your pension more than expected.

4. Not reviewing annually

Rules, thresholds, and your finances change.

Strategic Insight: This Is a Planning Exercise, Not a Switch

This isn’t:

“Super stops = Pension starts”

It’s:

A multi-year transition strategy

Done properly, it can:

Extend your retirement savings

Increase lifetime income

Improve cash flow stability

When Should You Get Advice?

You should consider professional advice if:

You’re within 3–5 years of Age Pension age

Your super balance is near thresholds

You want to optimise income, not just qualify

This is where structured planning makes a measurable difference.

FAQs

1. Can I receive super and Age Pension at the same time?

Yes. Many Australians receive a part Age Pension while drawing income from super.

2. Should I spend my super to qualify for the pension?

Not necessarily. The goal is to maximise total income, not just pension eligibility.

3. When should I apply for the Age Pension?

Usually at or after Age Pension age, but timing depends on your asset position and strategy.

4. Does my home affect my Age Pension?

Your principal residence is generally exempt (subject to current Services Australia rules).

5. How is super treated after Age Pension age?

It becomes assessable under the assets and income tests.

6. Can delaying the pension increase my benefits?

Yes, in some cases, if your assets reduce over time.

7. What is the biggest mistake people make?

Treating the transition as automatic instead of strategic.

Planning Your Transition to the Age Pension?

The difference between a good retirement and a great one often comes down to timing.

At What If Advice, we help Australians:

Structure super drawdowns effectively

Understand Centrelink rules clearly

Maximise total retirement income

Book a strategy session to map out your transition with clarity and confidence.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional advice. Rules relating to Centrelink, the ATO, and Services Australia are subject to change.