Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

Shares and managed funds

Super (if over Age Pension age)

Bank savings

Vehicles and valuables

Your principal home is generally exempt (subject to current Services Australia rules).

The Key Thresholds (Simplified)

There are two important levels:

Threshold Type | What It Means |

Lower threshold | You receive the full pension |

Upper threshold | You receive no pension |

Between these:

Your pension is reduced gradually using the assets test taper rate

(Thresholds vary depending on whether you’re single, partnered, and whether you own your home. Subject to current Services Australia rules.)

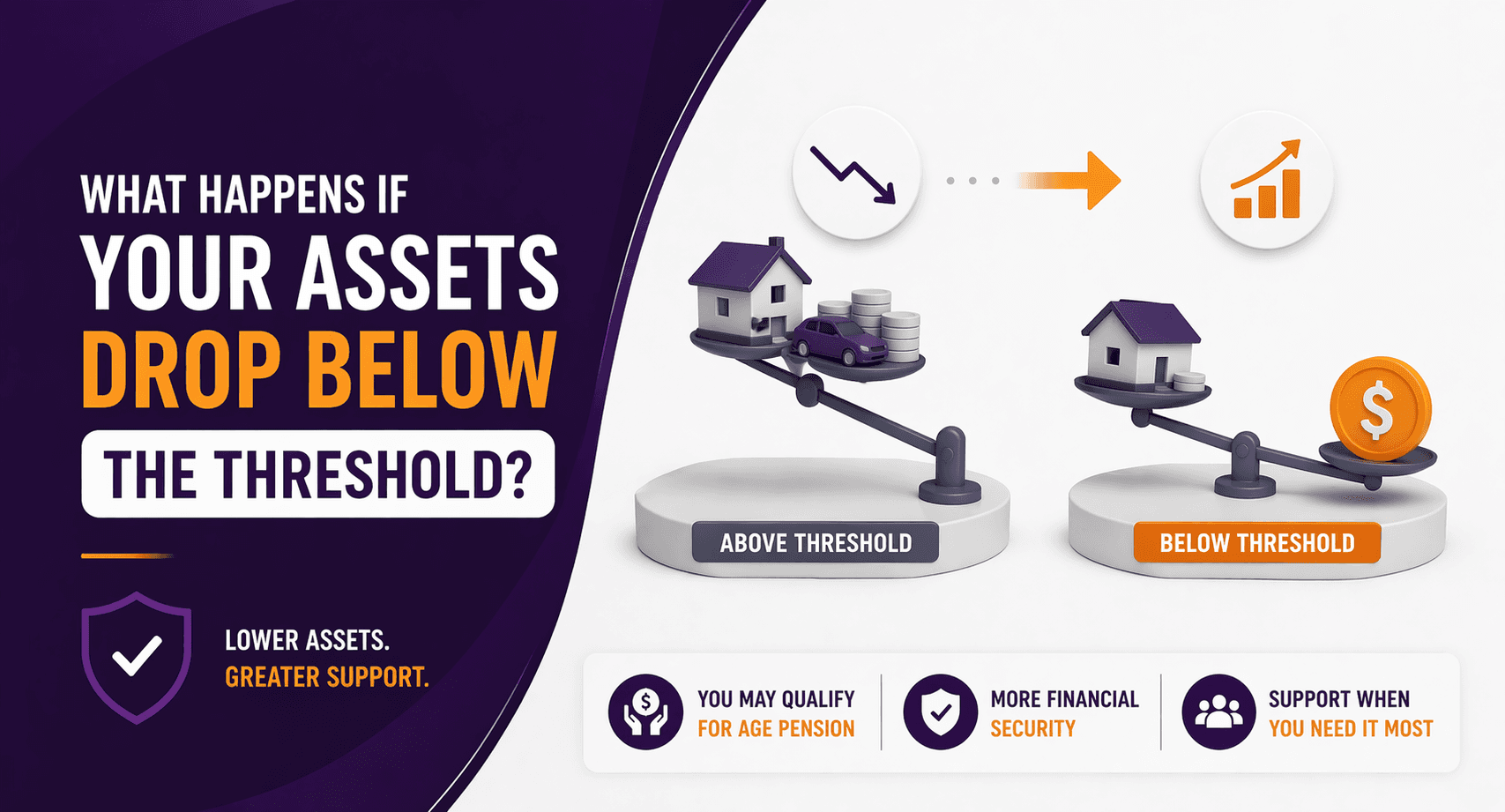

What Happens When Your Assets Drop Below the Threshold

1. Your Pension Can Increase

If your assets fall:

Your entitlement may increase

You may move closer to the full Age Pension

Example:

You had $450,000 in assessable assets = reduced pension

Market drops to $380,000 = pension increases

Why? Because Centrelink assumes you need more support.

2. You May Become Eligible Again

If your assets were previously:

Above the upper threshold (no pension)

And they drop below it:

You may become eligible for a part Age Pension

This is common during:

Share market downturns

Property value corrections

Retirement drawdowns

3. Flow-On Benefits May Increase

It’s not just the pension.

Dropping below thresholds can unlock:

Pensioner Concession Card

Lower PBS medication costs

Discounts on utilities and council rates

This can materially improve cash flow, even if the pension increase is modest.

4. Your Income Test Still Applies

Here’s where people get caught.

Even if your assets drop:

You’re still assessed under the income test

Centrelink uses:

Deeming rates on financial assets

Actual income for other assets

👉 You receive the lower result of:

Income test outcome

Assets test outcome

So your pension may not increase as much as expected.

Example Scenario (Realistic)

Situation | Before Drop | After Drop |

Assets | $500,000 | $400,000 |

Pension | $300/fortnight | $550/fortnight |

Status | Part pension | Higher part pension |

Same person. Same lifestyle. Different outcome purely due to asset values.

Do You Need to Notify Centrelink?

Yes. And this is where people get lazy and lose money.

You must report:

Changes in asset values

Sale or disposal of assets

Significant market changes (if relevant)

If you don’t:

You could be underpaid

Or worse, overpaid and later forced to repay

Report via:

myGov / Centrelink

Or through your adviser

What Counts as an Asset (Quick Guide)

Common assessable assets:

Cash and bank accounts

Shares, ETFs, crypto

Investment properties

Super (if over Age Pension age)

Vehicles and boats

Generally exempt:

Your home

Personal belongings (within limits)

Subject to current Services Australia rules.

Strategic Insight: This Isn’t Just Passive

A drop in assets isn’t always bad.

In some cases, it creates:

Higher pension income

Greater government support

Better overall cash flow

But relying on this is not a strategy.

Smart planning focuses on:

Structuring assets efficiently

Managing drawdowns

Aligning investments with pension outcomes

Common Mistakes to Avoid

1. Assuming the increase is automatic

It isn’t always. Reporting matters.

2. Ignoring the income test

This often limits the benefit.

3. Holding inefficient assets

Some assets reduce pension more than others.

4. Not reviewing annually

Your situation changes every year. So should your strategy.

When Should You Seek Advice?

You should speak to a financial adviser if:

Your assets fluctuate significantly

You’re close to pension thresholds

You want to maximise entitlements legally

You’re transitioning into retirement

This is where small adjustments can mean:

Thousands per year in difference

FAQs

1. Will my pension automatically increase if my assets drop?

Not always. You may need to report changes to Centrelink. Payments are reassessed based on updated information.

2. What is the assets test threshold in Australia?

It varies depending on your situation (single, couple, homeowner status) and is updated regularly by Services Australia.

3. Can I regain the Age Pension if my assets fall?

Yes. If your assets drop below the upper threshold, you may become eligible again.

4. Does Centrelink track asset values automatically?

No. You are responsible for reporting changes unless data is already linked.

5. What assets are exempt from the test?

Your primary residence is generally exempt. Some personal items may also be excluded.

6. How often should I review my assets?

At least annually, or whenever there is a significant financial change.

Not Sure How Your Assets Affect Your Pension?

Small changes in your asset position can significantly impact your Age Pension and overall retirement income.

At What If Advice, we help Australians:

Understand Centrelink rules clearly

Structure assets efficiently

Maximise retirement income legally

Book a strategy session to understand exactly where you stand, and what to do next.

Disclaimer

This information is general in nature and does not take into account your personal objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek professional advice. Rules relating to Centrelink, the ATO, and Services Australia are subject to change.