Looking for specific financial advice?

This blog provides general educational content. For personalized advice tailored to your unique situation, book a free consultation with our team of ASIC-licensed financial advisers.

Introduction

For many Australians, superannuation becomes the main “pay packet” once work slows down or stops. But retirement doesn’t automatically mean your super gets paid out. In most cases, you choose when and how to access it, and the tax outcome depends on your age, the type of super component, and how you withdraw.

This guide explains what typically happens to your super when you retire, common withdrawal options (lump sum vs income stream), and the tax basics to be aware of, subject to current ATO and Services Australia rules.

Quick answer: what happens to your super when you retire?

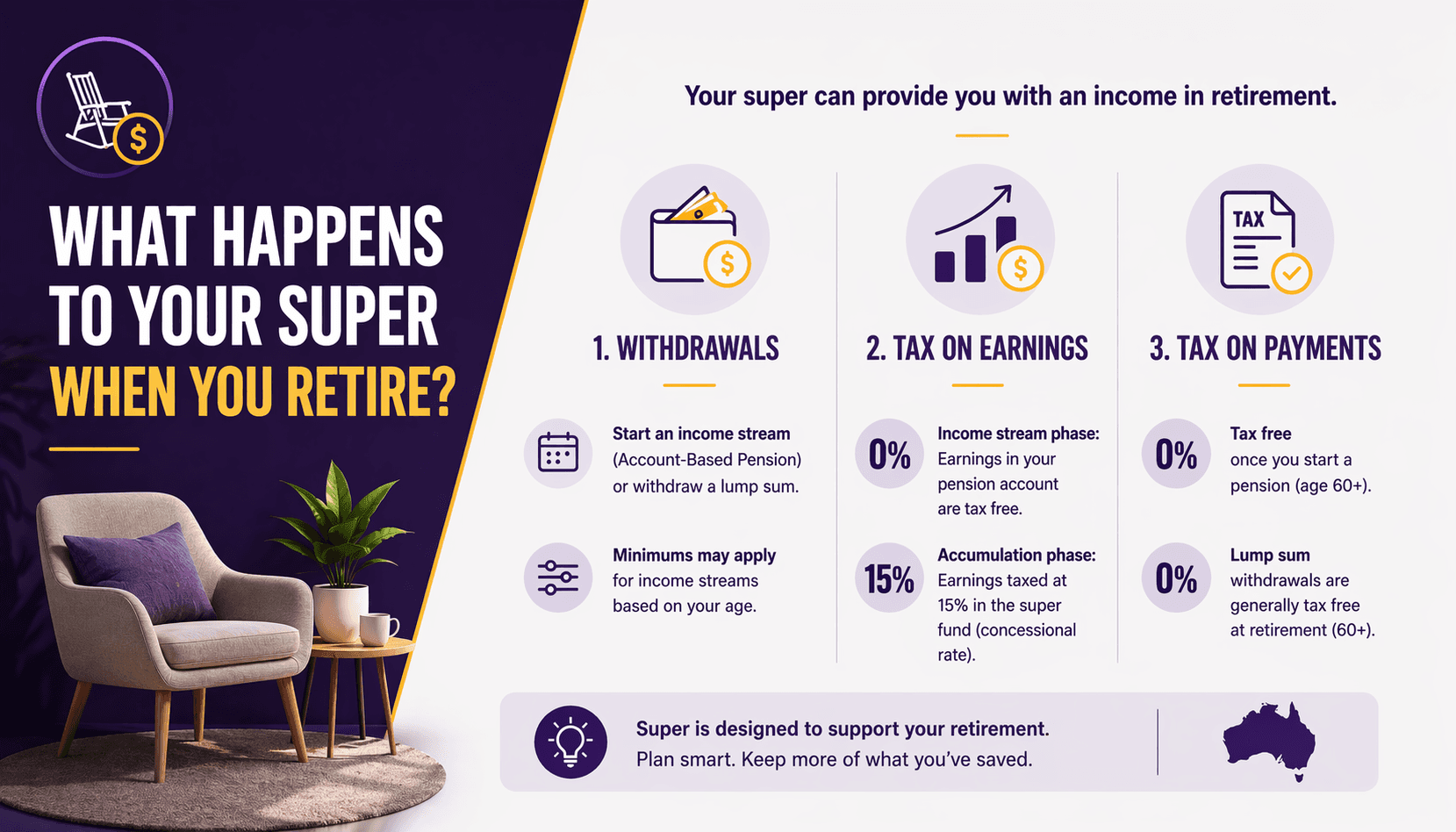

When you retire and meet a condition of release (usually reaching your preservation age and retiring, or turning 65), you can generally access your super.

Most retirees either:

Start an account-based pension (regular payments from super), or

Take a lump sum (one-off or multiple withdrawals), or

Use a mix of both.

Tax on withdrawals is often lower after age 60 for many people, but it’s not “tax-free in every scenario”. The details depend on your fund, your components, and your personal circumstances.

When can you access your super in retirement?

Access is governed by “conditions of release” under super rules, subject to current ATO rules. Common pathways include:

Reaching preservation age and retiring (stopping work with no intention to return, generally)

Turning 65 (you can usually access super regardless of work status)

Transition to retirement (TTR) income stream once you reach preservation age (even if still working), noting different rules may apply

If you’re unsure whether you’ve met a condition of release, check with your super fund first, getting this wrong can cause delays and tax complications.

What are your main options for taking money out?

Option 1: Start an account-based pension (income stream)

An account-based pension lets you keep your balance invested while drawing regular payments. You typically choose:

How often you’re paid (monthly, quarterly, annually)

How much you withdraw (within minimums/limits set under current rules)

Your investment option (often similar to super)

Why people choose it:

More control than a set annuity

Potential tax advantages compared with taking all money out at once

Can align payments with spending needs

Things to watch:

Market falls can reduce your balance and future income

Drawing too much early can increase longevity risk

Option 2: Take a lump sum (one-off or staged)

You can withdraw some or all of your super as a lump sum (subject to your fund’s processes). Some retirees take a lump sum to:

Pay off a mortgage

Build a cash buffer

Renovate or replace a car

Help family (carefully, as gifting can affect Centrelink)

A staged approach (multiple smaller lump sums over time) may help manage tax, budgeting, and investment risk, depending on your situation.

Option 3: Combine a pension and lump sums

This is common in practice. For example, you might:

Move most of your balance into an account-based pension for regular income, and

Keep a small amount in super (accumulation) or withdraw a lump sum for near-term expenses

The “right mix” often comes down to spending needs, Age Pension strategy, your risk tolerance, and estate planning preferences.

How is super taxed when you withdraw it?

Tax depends on your age, the tax components of your super (tax-free vs taxable), and whether you withdraw as an income stream or lump sum, subject to current ATO rules.

Is super tax-free after 60?

Many Australians hear “super is tax-free after 60”. In simple terms, withdrawals from a taxed super fund are often tax-free after age 60, but there are exceptions.

Situations where tax may still apply can include:

Certain taxable components depending on fund type

Untaxed elements (more common in some public sector schemes)

People under 60

Because tax is component-driven, two people with the same balance can have different outcomes.

What about tax if you retire before 60?

If you access super between preservation age and 60, tax may apply to the taxable component. The actual rate and any tax offsets depend on your circumstances and current ATO rules.

If you’re retiring earlier, planning the sequence of withdrawals (and how much you take) can materially affect your after-tax income.

Are account-based pension payments taxed differently to lump sums?

They can be. With an account-based pension, payments may have a tax-free portion and a taxable portion. If you take a lump sum, tax may also depend on the components. Your fund generally provides the breakdown.

Tip: ask your fund for a payment summary / pension certificate and the tax components before you start withdrawals.

What happens to your super investments when you retire?

Retirement doesn’t automatically mean moving to cash. Your super can remain invested whether it’s in accumulation or pension phase.

Key considerations:

Time horizon: retirement can last decades

Sequence risk: big withdrawals during market downturns can do more damage

Cash flow: holding some cash for 1–3 years of spending can reduce forced selling (general concept)

A practical approach many people use is a “bucket” style structure (cash for near-term spending, diversified growth for longer term), but the best setup depends on you.

Does retiring change how Centrelink assesses your super?

If you’re eligible for Centrelink payments (including the Age Pension), super can be assessed under the income and assets tests, subject to current Services Australia rules.

Common themes:

Once you reach Age Pension age, your super in pension phase is usually counted as an asset

Income from an account-based pension is generally assessed under deeming rules (depending on start date and current rules)

Large lump sum withdrawals and gifting can affect entitlements

If Centrelink outcomes matter for your household, consider getting advice before triggering major withdrawals.

What about your super if you keep working?

You don’t have to fully stop work to start planning withdrawals.

Options (subject to current rules) may include:

A transition to retirement (TTR) pension once you reach preservation age

Continuing contributions while drawing an income stream

Delaying access to keep super growing and simplify tax/administration

TTR strategies are often oversold. They can help in the right scenario, but fees, tax, and contribution rules need careful checking.

What happens to your super when you die?

Super doesn’t always form part of your standard Will. It’s typically paid according to your fund’s rules and any valid nomination.

Key actions:

Check if you have a binding death benefit nomination (and whether it has lapsed)

Confirm beneficiaries are eligible dependants under super law

Consider whether your pension has a reversionary beneficiary

Estate planning around super is worth reviewing well before retirement, not after.

FAQs

1. Can I take all my super out at retirement?

Usually, once you meet a condition of release you can withdraw some or all of your balance, subject to your fund’s processes and current ATO rules. Many retirees choose not to withdraw everything to keep money invested and manage tax and longevity risk.

2. Do I pay tax on super withdrawals after 60?

Often, withdrawals from a taxed super fund after 60 are tax-free, but it depends on your fund type and tax components, subject to current ATO rules. If you have untaxed elements or you’re under 60, tax may apply.

3. Is an account-based pension better than a lump sum?

Neither is universally “better”. An account-based pension can provide flexible income while staying invested, while a lump sum can suit debt repayment or major purchases. The best choice depends on cash-flow needs, tax components, investment risk and any Centrelink considerations.

4. How long will my super last once I start withdrawing?

It depends on your balance, spending level, investment returns, fees and how long you live. A sustainable plan usually considers market downturns and builds flexibility into spending rather than assuming steady returns every year.

5. Can I keep my super in the same fund when I retire?

In many cases, yes. Your existing fund may let you start an account-based pension without changing providers, though investment menus and fees may differ between accumulation and pension accounts. Always compare features and costs before switching.

Conclusion

When you retire, your super doesn’t “turn into cash automatically”. You typically decide how to access it, via an account-based pension, lump sums, or a combination, and the tax outcome depends on your age, your super’s components and your fund type, subject to current ATO rules. Add Centrelink and investment risk into the mix, and it’s clear why a retirement income plan matters.

Call to action: build your retirement income plan

Want help turning super into a practical, tax-aware retirement pay cycle? Join a What If Advice retirement workshop to learn the key decisions, the common traps, and the questions to ask your fund before you start drawing down.

General advice disclaimer

This article provides general information only and does not consider your objectives, financial situation or needs. It is not personal financial advice. Consider seeking advice from a licensed financial adviser and check relevant details with the ATO and Services Australia, as rules are subject to change.